![]()

Chapter 1

Introduction to Mergers and Acquisitions

Harvey Poniachek

Rutgers Business School

Introduction

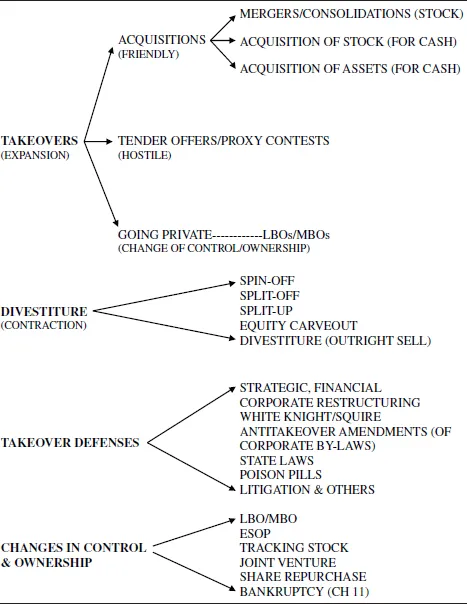

Mergers and acquisitions (M&As) are quite popular in the business world and are often the principle strategy for corporate growth and restructuring. Most major companies have conducted numerous M&As throughout their history. M&As include a variety of activities and types, and could be horizontal transactions between companies with similar products or services, vertical, involving companies with different value-added activities, or conglomerate, involving companies in completely different industries. See Exhibit 1 for the definition of broadly defined M&As.

The parties to a merger are the buyer, usually referred to as the acquirer or bidder, and the seller or target. In a narrowly defined merger or acquisition, one company acquires another and the acquirer is the surviving party and remains in business, whereas the target company ceases to exist. Mergers are motivated by various objectives, including expectations for synergy that could be generated from expansion of sales and revenues, reduced cost, and lower cost of capital. The premise of synergy is that the sum of the parts is more valuable than the parts, or 2 + 2 = 5.

Exhibit 1:M&As: Broadly Defined Activities

M&As change the ownership and control of a public corporation, with senior management of the target firm usually departing after the merger and a new management team takes over. Target’s shares or assets are purchased for various consideration, including cash, stock or a combination of both.

M&A transactions are more complicated and much larger than ordinary capital expenditures. In light of their complexities and magnitude, M&As constitute a most significant corporate financial decision that commonly involves various specialists. M&As are legally intensive and subject to various laws and regulations and subject to various taxation laws and accounting requirements.

In mergers, sellers generally do better than buyers and following an announcement of a bid target shareholders receive an average gain of 25–30%; whereas acquirer’s shares usually decline, but in aggregate the value of the shares increases by some 5%.1

This chapter reviews M&As data, growth through M&A, merger trends and influences, M&A models, performance, and risk.

Growth Through Mergers

The survival and prosperity of corporations over the long term depend on their ability to grow and develop through a process of restructuring and redeployment of resources. Corporate restructuring could be accomplished internally, or organically, by shifting resources from mature and declining business activities to new activities with more attractive growth potential. Alternatively, restructuring could occur externally, or inorganically, through M&As, which have become an essential vehicle for corporate change and a dominant feature of the American economy since the late 19th century.

GE experience in the 1980s and 1990s reflects the significance of pursuing growth strategy via M&As. Under the leadership of Jack Welch, the President and Chairman of GE during 1981–2001, the company made 993 acquisitions at an estimated cost of approximately $165 billion and divested of over 400 businesses valued at an estimated $28 billion. During this period, the company’s revenue has grown to $130 billion in 2000 from $21 billion when Mr. Welch became chairman in 1981. GE experienced 9.9% compounded annual growth rate (CAGR) during 1985–2000, of which 4 percentage points came from acquisitions.2

There are limits to growth through M&As due to a limited pool of available targets, antitrust concerns (GE failed to takeover Honeywell due to EU antitrust concerns), risk, and disadvantages of becoming too big. Jeffrey R. Immelt, Mr. Welch successor as CEO & Chairman of GE, adopted a new policy that has divested of many of the acquisitions made under the prior administration, and embarked on a new strategy.3 It seems that Mr. Immelt implicitly repudiated Mr. Welch’s growth model by moving to dismantle parts of the sprawling GE empire by divesting of NBC Universal and GE Capital, and acquiring some prize companies.

The issue is whether the conglomerate growth model through M&As that Mr. Welch promoted at GE is still viable? Data shows that during the 18-year tenure of Mr. Jeffrey R. Immelt as GE’s chief executive,4 the company’s stock underperformed against the S&P 500 index of the overall stock market performance. For instance, GE shares dropped 25% over the past 10 years, in contrast with a 59% rise for the S&P 500, rival industrial conglomerate Honeywell’s stock has more than doubled, and United Technologies gained 67%. Yet, Mr. Immelt pointed to the increased strength of the company’s industrial businesses, their competitiveness, and large market shares.

Merger Trends and Main Influences

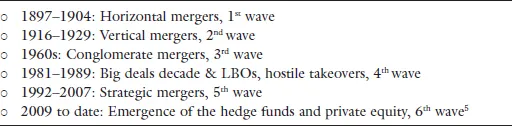

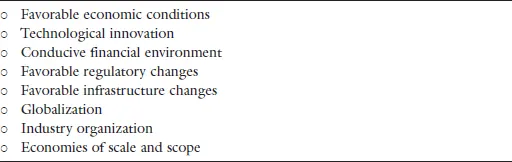

We observe a variety of mergers waves in the past century and a quarter, see Exhibit 2. The mergers since the late 1800s were driven primarily by favorable economic and financial conditions, deregulations, technological innovations, shifts in the competitiveness of companies, globalization, and reasonable valuations, see Exhibit 3. The financial crisis and recession during 12/2007–6/2009 caused a sharp decline in M&As activities, but a solid rebound has occurred thereafter. Going forward, the 2016’s M&A trend is expected to continue as companies seek innovative and transformative transactions to complement organic growth to enhanced scale and synergistic strategic fits.

Exhibit 2:Historic Merger Waves

Source: Patrick A. Caughan, Mergers, Acquisitions, and Corporate Restructuring, 5th Ed., Wiley, 2011, Ch 2; Weston, J. Fred et al., Takeovers, Restructuring and Corporate Governance, 4th Ed., Prentice Hall, 2004, p. 7 and Ch 7.

Exhibit 3:Merger Waves’ Main Influences

Source: Harvey Poniachek.

M&As encompass a wide spectrum of transaction types that afford firms the ability to adjust relatively fast to new challenges and opportunities and maintain or achieve competitive advantage. Broadly defined M&A activities include expansion through M&As; joint ventures; contraction through divestitures or sell-offs; various changes in corporate control and ownership, including going private and leverage buy-outs; and rearrangements through recapitalization and bankruptcy reorganization. Exhibit 3 defines the scope of M&A activities.

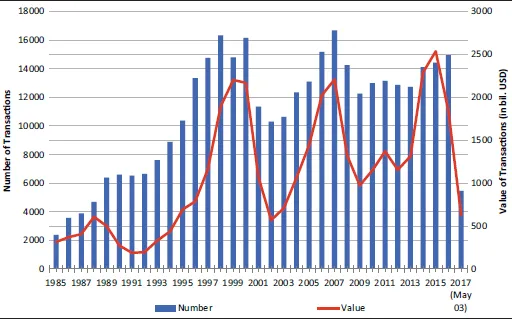

M&A Data

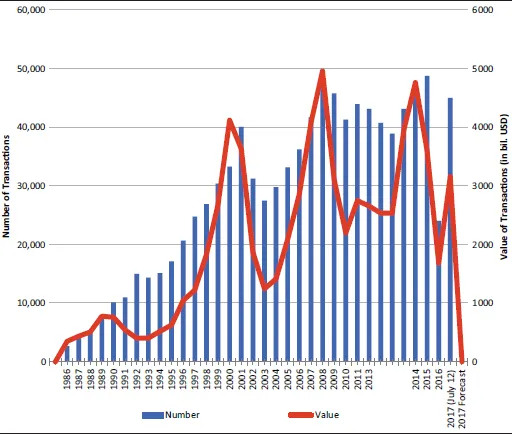

The year 2015 marked the busiest ever for mergers and acquisitions, whereby US companies announced more than $2.1 trillion in transactions, and global M&A volume topped $4.7 trillion in aggregate.6 A Deloitte survey of nearly 2,300 executives and managers from US corporations and private equity firms showed that 87% of the respondents expected their M&A deal activity to sustain or exceed the 2015’s record. Similar results were also reported by Dealogic7 and EY. See Exhibits 4 and 5 for global and North American M&As.

Exhibit 4:M&As Worldwide

Source: https://imaa-institute.org/mergers-and-acquisitions-statistics/.

Exhibit 5:M&As North America

Source: https://imaa-institute.org/mergers-and-acquisitions-statistics/.

Several factors are driving the optimism, including excess cash, high stock prices, and interest rates at historically low levels. While low interest rates and easy access to funds have allowed many acquirers to orchestrate deals, continued economic uncertainty, particularly in Europe and in several markets across Asia, are expected to be a key concern. Despite global economic concerns, 75% of corporate respondents are still searching for a slightly larger share of cross-border deals, while 84% of private equity are seeking acquisitions in foreign markets.

Going forward, more divestitures are planned, with 52% of the corporate respondents stating that their company plans to pursue divestitures to shed noncore assets in the year ahead to help focus their business, and in some sectors to raise capital. The industries that are expected to generate the most M&A activity in the years to come are technology, oil and gas, financial services, and healthcare.

Private equity respondents expressed concern about deals that did not meet expectations over the last 2 years, with 56% of those surveyed saying more than half of deals had not...