America’s landscape is undergoing a profound transformation as demand grows for a different kind of American Dream--smaller homes on smaller lots, multifamily options, and walkable neighborhoods. This trend presents a tremendous opportunity to reinvent our urban and suburban areas. But in a time of fiscal austerity, how do we finance redevelopment needs? In Foundations of Real Estate Development Finance: A Guide for Public-Private Partnerships, urban scholar Arthur C. Nelson argues that efficient redevelopment depends on the ability to leverage resources through partnerships. Public-private partnerships are increasingly important in reducing the complexity and lowering the risk of redevelopment projects. Although planners are an integral part of creating these partnerships, their training does generally not include real-estate financing, which presents challenges and imbalances in public-private partnership.

This is the first primer on financing urban redevelopment written for practicing planners and public administrators. In easy-to-understand language, it will inform readers of the natural cycle of urban development, explain how to overcome barriers to efficient redevelopment, what it takes for the private sector to justify its redevelopment investments, and the role of public and nonprofit sectors to leverage private sector redevelopment where the market does not generate sufficient rates of return.

This is a must read for practicing planners and planning students, economic development officials, public administrators, and others who need to understand how to leverage public and non-profit resources to leverage private funds for redevelopment.

eBook - ePub

Foundations of Real Estate Development Financing

A Guide to Public-Private Partnerships

- 200 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Foundations of Real Estate Development Financing

A Guide to Public-Private Partnerships

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Topic

ArchitectureSubtopic

Architecture GeneralChapter 1

The Cycle of Development, Optimal Redevelopment, Redevelopment Goals and Benefits, and Barriers to Redevelopment

Before I review the foundations of real estate development finance and the role of public-private partnerships in redeveloping the United States, I need to show where P3s fit in the development/redevelopment cycle. I start by describing the cycle of urban development and what I call “efficient redevelopment.” This is followed by a review of impediments to efficient development, and I conclude with the role of P3s to facilitate efficient redevelopment.

The Cycle of Development

That urban areas transform themselves over time is certain. Miles Colean (1953) calls this the “cycle of development.” Larry S. Bourne (1967) provides a succinct review of the process, which comprises an initial period of construction followed by a period of increasing value and function, then a period of increasing maintenance costs and deterioration, perhaps leading to idling or abandonment, and then a period of redevelopment as the old structures are replaced.

Consider the normal life of a building. It is built initially to serve an investment horizon and becomes obsolete either because of economic factors (where the building is more expensive to maintain than justified by revenue streams) or functionality (where markets have changed, leaving the building unsuitable for its initial use) or both. As the structure loses value through a process called depreciation, the land on which it sits will normally gain value, especially if the urban area is growing.

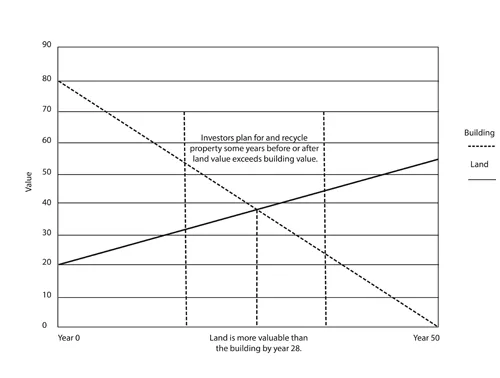

Figure 1.1 illustrates this appreciation in land and depreciation in the structure assuming a new building is built with a fifty-year useful life, which is common for one- and two-floor office buildings. When its doors open, the building accounts for 80 percent of the property value and the land for the remaining 20 percent; this is a typical building-to-land relationship for commercial buildings. The building depreciates over a fifty-year period, or 1.6 percent annually, and becomes worthless (except for any scrap value) in the fiftieth year. Land, on the other hand, gains value at about the rate of growth of the urban area, compounded. If the population or employment growth rate is 2 percent annually, the land value increases at this rate (net of inflation). By the twenty-eighth year, the land is worth more than the building. Some years before and after this happens, the investors reassess their investment and, ideally, renew the site by replacing the initial structure with one consistent with the highest and best use over a new investment horizon.

Figure 1.1. Optimal timing of redevelopment for a fifty-year structure assuming land value appreciates 2 percent annually, compounded, net of inflation. (In the public domain; created by Arthur C. Nelson and redrawn by Allison Spain)

For the most part, nonresidential space is not durable. Overall, the United States has about 100 billion square feet of enclosed space used for such nonresidential purposes as retail, offices, institutions, and so forth. About 70 percent of all nonresidential space is housed in buildings of one or two floors. In any given year, about 2.5 billion square feet of nonresidential space becomes idled or is replaced—2.5 percent annually.

In contrast, residential structures are quite durable. The United States has about 130 million residential units, but only 500,000 residential units—about 0.5 percent—become vacant or are replaced each year. I have estimated that the typical residential unit lasts about 170 years (Nelson 2004, 2013a). Pitkin and Myers (2008) estimate that units last 200 to 500 years. Whatever the length, planners and public officials need to understand that residential development is very durable, not because the structures themselves are built to last a long time, but because occupants will maintain the unit through repairs and rehabilitation for decades or even centuries. Most nonresidential development, in contrast, is not durable and needs to be replaced about every 20 to 40 years.

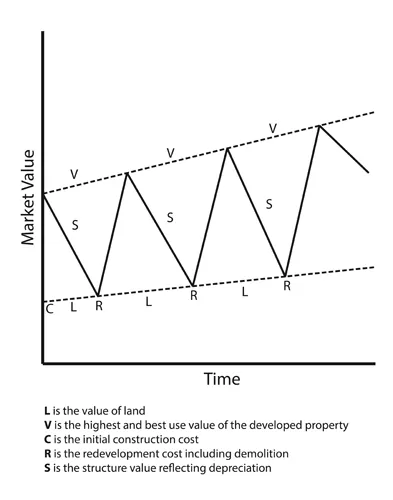

Urbanized land thus goes through a series of changes over decades and centuries. The first building on a site, for instance, might be a neighborhood grocery store. As the building ages, it becomes more expensive to maintain, so profit (revenue net of costs) goes down. In the meantime, the land value goes up. The “opportunity” cost of keeping the land in its current use goes up as profit in the current use goes down. At some point, the landowner incurs the cost of demolition and rebuilding to increase profits by going to the “highest and best” use of the land. Maybe the new structure is a low-rise retail store. In a few more decades, the next highest and best use might be a midrise office building. In theory, redevelopment of the built environment would be seamless, leading to ever higher and better uses over time, as illustrated in figure 1.2. In practice, this is rarely the case, for reasons I outline next.

Figure 1.2. The cycle of urban redevelopment. (In the public domain; created by Arthur C. Nelson and redrawn by Allison Spain)

Optimal Redevelopment

The first buildings to be constructed in an area are often small and built of material that is easy to dismantle. At some point, buildings become of such size and durability that they may be difficult to replace, especially if market conditions do not warrant the expense of both dismantling and rebuilding the site. The result can be what Bourne (1967) calls a “constrained” process of redevelopment. This could lead to blight as the structure becomes idled or vacant and its presence discourages reinvestment in the area, thereby delaying redevelopment beyond that which is “optimal.”

In a classic paper theorizing the optimal timing of redevelopment, Donald Shoup (1970, 43) demonstrated that the optimal time for redevelopment of urban land depends on four factors:

The optimal date for development or redevelopment of urban land depends on (1) the discount rate applying in the real...

Table of contents

- Cover

- Contents

- Foreword

- Preface

- Acknowledgments

- Introduction: The Future of America Is Redevelopment, and the Future of Redevelopment Is Public-Private Partnerships

- Chapter 1: The Cycle of Development, Optimal Redevelopment, Redevelopment Goals and Benefits, and Barriers to Redevelopment

- Chapter 2: Implementation of Redevelopment Plans and the Role of Public-Private Partnerships

- Chapter 3: Real Estate Finance and Development Basics

- Chapter 4: Survey of Public-Private Partnership Tools and the Role of Public Patient Equity to Leverage Private Real Estate Development

- Conclusion: America’s Progress Depends on Redevelopment through Public-Private Partnerships

- Appendix A: Workbook User Guide

- Appendix B: Simplified Depreciation Periods for Land Uses

- Notes

- References

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Foundations of Real Estate Development Financing by Arthur C. Nelson,Arthur C. Nelson in PDF and/or ePUB format, as well as other popular books in Architecture & Architecture General. We have over 1.5 million books available in our catalogue for you to explore.