Introduction to Accounting

Pru Marriott,J R Edwards,Howard J Mellett

- 560 Seiten

- English

- ePUB (handyfreundlich)

- Über iOS und Android verfügbar

Introduction to Accounting

Pru Marriott,J R Edwards,Howard J Mellett

Über dieses Buch

The fully revised and updated Third Edition of this textbook provides an accessible introduction to accounting for students coming to the subject for the first time. It embraces the basic techniques and underlying theoretical concepts in accounting and shows how these are applied in various circumstances.

This New Edition incorporates major changes which improve and update the previous edition. It can be easily used by students working on their own, as well as in a classroom environment.

It provides:

- Fully illustrated & worked examples

- Student Activities

- End of chapter questions, many of which have been taken from major accounting examination bodies.

-The solutions to all activities are given at the end of each chapter, and answers to the end of chapter questions are also supplied.

Introduction to Accounting is an essential textbook for undergraduate accounting students. It is designed to meet the needs of both the non-specialist and those intending to specialise in accounting at undergraduate and also postgraduate levels. The Solutions Manual will be available via the SAGE website.

Häufig gestellte Fragen

Information

| 1 | The framework of accounting |

- explain the accounting and decision-making process;

- identify the main entities involved in the supply of accounting information;

- distinguish between financial accounting and management accounting;

- identify the external users of accounting information; and

- outline the nature and content of the principal accounting statements.

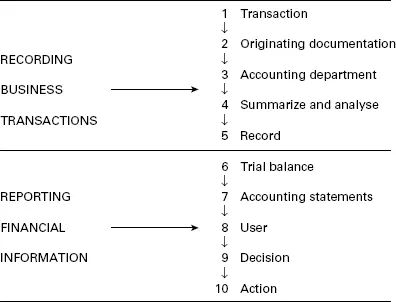

THE ACCOUNTING PROCESS

SUPPLIERS OF ACCOUNTING INFORMATION

| 1 | Sole traders.These are businesses that have a single owner who also takes all the major managerial decisions. Operations are usually on a small scale, and typical examples are an electrician, the local newsagent and hairdresser. The main reason why accounts are prepared for the sole trader is to help establish the amount of income tax due to the Inland Revenue. He or she makes little use of accounting statements for business decisions. Instead these decisions are based on knowledge obtained as a result of direct contact with all aspects of business activity. |

| 2 | Partnerships.These exist where two or more individuals join together to undertake some form of business activity. The partners share between them ownership of the business and the obligation to manage its operations. Professional people, such as accountants, solicitors and doctors, commonly organize their business activities in the form of partnerships. Accounting statements are required as a basis for allocating profits between the partners and, again, for agreeing tax liabilities with the Inland Revenue. |

| 3 | Clubs and societies.There are, in Britain, many thousands of clubs and societies organized for recreational, educational, religious, charitable and other purposes. Members invariably pay an annual subscription and management powers are delegated to a committee elected by the members. The final accounts prepared for (usually large) societies, formed by registering with the Registrar of Friendly Societies, are often controlled by statute. For the local club or society, the form of the accounts is either laid down in the internal rules and regulations or decided at the whim of the treasurer. Conventional accounting procedures are sometimes ignored in a small organization. Reasons for this are lack of expertise, the meagre quantity of assets belonging to the organization and the fact that the accounts are of interest only to the members. |

| 4 | Limited companies.A limited company is formed by registering, under the Companies Act, with the Registrar of Companies and complying with certain formalities. The company may be private, indicated by the letters Ltd at the end of its name, or public, in which case the designatory letters are plc. The main significance of the distinction is that only the latter can make an issue of shares to the general public. In the case of public companies there is the further distinction between quoted companies, whose shares are traded on the stock exchange, and unquoted companies. In general, public companies are larger than private companies and quoted companies larger than unquoted. The directors of all limited companies are under a legal obligation to prepare and publish accounts, at least once in every year, which comply with the requirements of the Companies Act. (It should be noted that there are also in existence a small number of unlimited companies – for example, this method of incorporation is sometimes used by professional firms who are not allowed to have limited liability but want the tax advantages of being a company.) A limited company may, alternatively, be formed by means of either a private Act of Parliament or a royal charter. These are called statutory and chartered companies, respectively. The form of their accounts may be regulated by the charter or statute. In addition, it is normal practice to comply with the general requirements of the Companies Act. |

FINANCIAL ACCOUNTING AND MANAGEMENT ACCOUNTING COMPARED

Inhaltsverzeichnis

- Cover Page

- Title Page

- Copyright

- Dedication

- Contents

- Series editor’s preface

- Preface

- 1 The Framework of Accounting

- 2 The Balance Sheet

- 3 Profit Calculated As The Increase in Capital

- 4 The Preparation of Accounts from Cash or Incomplete Records

- 5 The Double Entry System I: The Initial Recording of Transactions

- 6 The Double Entry System II: Ledger Accounts and the Trial Balance

- 7 The Double Entry System III: Periodic Accounting Reports

- 8 Asset Valuation, Profit Measurement and The Underlying Accounting Concepts

- 9 Partnerships

- 10 Company Accounts

- 11 Interpretation of Accounts: The Cash Flow Statement

- 12 Interpretation of Accounts: Ratio Analysis

- 13 Decision–Making

- 14 Standard Costing and Budgetary Control

- Appendix: Solutions to questions

- Index