With a new look at the 1880s financial reforms in Japan, Steven J. Ericson's Financial Stabilization in Meiji Japan overturns widely held views of the program carried out by Finance Minister Matsukata Masayoshi. As Ericson shows, rather than constituting an orthodox financial-stabilization program—a sort of precursor of the "neoliberal" reforms promoted by the IMF in the 1980s and 1990s—Matsukata's policies differed in significant ways from both classical economic liberalism and neoliberal orthodoxy.

The Matsukata financial reform has become famous largely for the wrong reasons, and Ericson sets the record straight. He shows that Matsukata intended to pursue fiscal retrenchment and budget-balancing when he became finance minister in late 1881. Various exigencies, including foreign military crises and a worsening domestic depression, compelled him instead to increase spending by running deficits and floating public bonds. Though he drastically reduced the money supply, he combined the positive and contractionary policies of his immediate predecessors to pull off a program of "expansionary austerity" paralleling state responses to financial crisis elsewhere in the world both then and now.

Through a new and much-needed recalibration of this pivotal financial reform, Financial Stabilization in Meiji Japan demonstrates that, in several ways, ranging from state-led export promotion to the creation of a government-controlled central bank, Matsukata advanced policies that were more in line with a nationalist, developmentalist approach than with a liberal economic one. Ericson shows that Matsukata Masayoshi was far from a rigid adherent of classical economic liberalism.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Financial Stabilization in Meiji Japan un PDF/ePUB en línea?

Sí, puedes acceder a Financial Stabilization in Meiji Japan de Steven J. Ericson en formato PDF o ePUB, así como a otros libros populares de History y Japanese History. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

FROM “ŌKUMA FINANCE” TO “MATSUKATA FINANCE,” 1873–1881

Beginning in 1878, Japan suffered mounting inflation and currency depreciation triggered by the huge issue of additional inconvertible notes to pay for suppression of the Satsuma Rebellion of 1877, the last and greatest samurai uprising following the Meiji Restoration.1 In response, the Meiji regime took tentative steps toward a program of retrenchment in 1879, Ōkuma Shigenobu’s last full year as finance minister. During that year, total government notes in circulation, which had continually increased since the start of the Meiji period, began a steady decline until their complete replacement by central bank notes two decades later.2 It was under Ōkuma’s successor as finance minister, Sano Tsunetami, however, that the government embarked on austerity in earnest. In late 1880 and early 1881 the Council of State adopted practically all the components of both classical economic liberalism and what in the late twentieth century would become IMF-style neoliberal orthodoxy: fiscal retrenchment, increased taxation, privatization, and currency stabilization. Later in 1881 the government, despite having rejected a proposal made by Ōkuma a year earlier that it raise a large foreign loan to redeem its fiat notes, would approve a new plan he submitted with Itō Hirobumi (1841–1909) to sell domestic bonds abroad and establish a central bank on the British model.

That 1881 plan embodied the critical difference between the Ōkuma and Matsukata approaches to financial policy. Ōkuma sought to engineer a rapid currency reform using the proceeds from overseas bond issuance while applying the savings from austerity to continue the expansionary economic policies he had pursued as finance minister. The adoption of his new foreign-borrowing scheme in the summer of 1881 signaled a softening of official commitment to fiscal retrenchment. Matsukata intended to continue the Sano initiatives with the exception of borrowing abroad and founding a British-style central bank. Yet in practice he would diverge from much of the Sano austerity program in ways that differed from both classical and neoliberal orthodoxy.

Financial Policy in the Early Meiji Period

In the first two decades after the Restoration, Japan experienced a financial roller coaster. The country lurched from a precocious but unsustainable gold standard, which the regime adopted in 1871, to a legal bimetallic monetary system in 1878—but, in practice, no metal standard, as government notes became inconvertible in 1872, as did U.S.-style national bank notes in 1876. Starting in the fall of 1881, Matsukata would put Japan on track toward a functioning, de facto silver standard (even as the country remained officially bimetallic) and ultimately a return to gold convertibility in 1897. Meanwhile, the economy moved from mild deflation in the middle of the 1870s to sharp inflation in the years 1878–1881, followed by an equally intense deflation during the Matsukata reform. Foreign trade also swung from persistent deficits through 1881 to surpluses, with a surge in exports, especially of raw silk, and a decline in imports during the Matsukata deflation. Then came a decade of inflation, as the global price of silver continued to fall, boosting Japanese trade with Western gold-bloc nations and largely insulating silver-standard Japan from the long-term deflationary trend among those nations.

In 1871, a decade before the Matsukata reform, the Meiji government began working to establish a gold-backed monetary system on the recommendation of Vice-Minister of Finance Itō Hirobumi, who was then studying financial systems in the United States. Itō presciently observed in a letter to his colleagues in Tokyo that the “trend of opinion in Western lands” was in favor of the gold standard.3 He thus predicted that countries in the West with silver or bimetallic standards would follow Britain’s lead and go for gold, as in fact many did after Germany officially adopted that standard in 1873. Also, in 1871 the Meiji state established the yen as the official monetary unit and began the process of replacing more than sixteen hundred varieties of pre-1868 domain notes (hansatsu) with its own yen notes.4 Furthermore, in 1872 the government accepted Itō’s proposal to organize a decentralized U.S.-style system of “national banks” chartered by the state to issue notes exchangeable for gold from the banks’ reserves. The banks would deliver 60 percent of their capital stock in the form of government notes to the Ministry of Finance and could issue up to that amount in their own notes but had to keep the remaining 40 percent of their capital as a reserve in gold coins, resulting in an “extraordinarily high” ratio of specie reserve compared to the experience of most Western banks.5

The government itself minted not only gold coins but also silver ones for foreign-trade purposes because the Western powers insisted on the use of silver—East Asia’s de facto trade standard—in the treaty ports. Consequently, despite being legally on gold for most of the 1870s, Japan in practice had a bimetallic currency system—silver for international transactions and gold for internal ones—until the government made the bimetallic system official in 1878 when it decreed silver coins to be legal tender domestically as well.

In 1886, after the Matsukata deflation, Japan would go on a de facto silver standard with both government notes and newly issued Bank of Japan notes fully convertible to silver. In 1897 the country would return to gold after the government had successfully negotiated a phased revision of the unequal treaties and secured an enormous indemnity in specie from China following Japan’s victory in the Sino-Japanese War of 1894–1895. Japan would thus follow the precedent Germany had set after the Franco-Prussian War a generation earlier of using war reparations to leverage its adoption of the gold standard.6

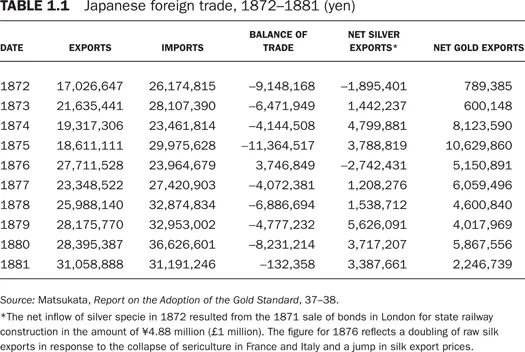

In the 1870s, however, the Meiji government was unable to maintain the gold side of its de facto and, from 1878, legal bimetallic currency system. With the price of silver entering a long-term decline, as other countries followed Germany in going on the gold standard, foreign merchants in the treaty ports began exchanging silver for gold coins, which the exchange rate the regime established in 1871 undervalued. Thus, as Mark Metzler notes, “Japan, like other bimetallic countries, experienced an outflow of gold and was pushed onto a de facto silver standard”7 (though the nation would not have an operational silver standard until 1886, by which time Matsukata had sufficiently contracted the bloated money supply and built up the Treasury’s specie reserve). In the early to middle 1870s, the gold flight compounded the country’s lack of specie needed to back the official, pre-1878 gold standard. From 1872 to 1877 Japan hemorrhaged on average over ¥5 million in gold coins a year. The gold outflow persisted in the first three years under the legal bimetallic system at an average annual rate of nearly ¥5 million (see table 1.1).

Shortage of specie, together with the onerous reserve requirement, also impeded the founding of national banks, only four of which had opened for business by 1876. In the first week of August of that year, the government announced both a revision of the national bank regulations and the compulsory commutation of samurai stipends into interest-bearing public bonds. Under the banking revision, the regime dropped the convertibility requirement for national banks, allowing them to issues notes for up to 80 percent of their capital in the form of public bonds deposited at the Treasury and to hold the rest of their capital as a reserve in unbacked government notes. The government hoped these changes would not only invigorate the national banking system but also provide a safe investment for members of the former ruling class, who would receive a staggering ¥174 million in commutation bonds.8 The remedy had the desired effect: 21 new national banks opened in 1877. But the government’s decision the next year to make the bonds transferable opened the floodgates: as a Western observer declared in 1882, national banks “have sprung up like mushrooms” until their number had reached 153 by 1880, at which point the Ministry of Finance stopped issuing new licenses.9

The national banks have generally received a bad reputation as a failed experiment in decentralized banking, for they ended up exacerbating inflation by issuing inconvertible notes worth more than ¥32 million after 1876. For example, according to Fujimura Tōru, the doyen among postwar Matsukata experts, with the abandonment of convertibility, the national banks “lost the proper function of banks and became troublesome (yakkaina) entities”; they “looked good but in fact had become usurious entities unable to make any contribution to the expansion of production.”10

Ishii Kanji, however, presents a contrary view. He points out that the banks’ newly issued notes “circulated smoothly” at first, supplying the funding needs of “various developing industries”; in his view, “the history of the national banks should not be treated as an unnecessary mistake.”11 To redeem unbacked government notes, the regime had to improve public finances by slashing its enormous outlay on ex-samurai stipends. The 1876 revision of the national bank regulations proved “indispensable” to the accomplishment of that task. Paying those stipends had accounted for as much as a third of government expenditures until 1876; the commutation, however, reduced the cost of supporting the former samurai by half. Adopting the national banking system may have been a detour on the road to establishing a central bank, which even Itō Hirobumi, the champion of that decentralized system, admitted in the early 1870s might be the eventual outcome, but, as Ishii suggests, changing the system to permit the use of commutation bonds as the basis for note issuance was “an effective strategy” for government leaders “to take feudal privileges away from their colleagues as peacefully as possible.” (Granted, that strategy failed to avert the most serious samurai rebellion from breaking out in 1877!) Ishii cogently concludes that creating a standard, centralized currency system was “not only an economic issue but a highly political one.”12

The issuance of unbacked national bank notes certainly helped stoke the fires of inflation, but the government compounded the problem by printing fiat paper on an even greater scale to help pay for its extensive nation-building efforts, ranging from the creation of a Western-style military to the initi...

Índice

Acknowledgments

Introduction

1. From “Ōkuma Finance” to “Matsukata Finance,” 1873–1881

2. Orthodox Finance and “The Dictates of Practical Expediency”

3. Austerity and Expansion

4. Spending in a Time of “Retrenchment”

5. Founding a Central Bank

6. “Poor Peasant, Poor Country”?

Conclusion

Notes

Works Cited

Index

Estilos de citas para Financial Stabilization in Meiji Japan

APA 6 Citation

Ericson, S. (2020). Financial Stabilization in Meiji Japan ([edition unavailable]). Cornell University Press. Retrieved from https://www.perlego.com/book/950759/financial-stabilization-in-meiji-japan-the-impact-of-the-matsukata-reform-pdf (Original work published 2020)

Chicago Citation

Ericson, Steven. (2020) 2020. Financial Stabilization in Meiji Japan. [Edition unavailable]. Cornell University Press. https://www.perlego.com/book/950759/financial-stabilization-in-meiji-japan-the-impact-of-the-matsukata-reform-pdf.

Harvard Citation

Ericson, S. (2020) Financial Stabilization in Meiji Japan. [edition unavailable]. Cornell University Press. Available at: https://www.perlego.com/book/950759/financial-stabilization-in-meiji-japan-the-impact-of-the-matsukata-reform-pdf (Accessed: 14 October 2022).

MLA 7 Citation

Ericson, Steven. Financial Stabilization in Meiji Japan. [edition unavailable]. Cornell University Press, 2020. Web. 14 Oct. 2022.