The global energy scenario has transformed in the past 20 years. Oil demand, earlier driven by the West, is now shifting to the East, more specifically to Asia. New oil supplies from North America have challenged the hegemony of the traditional oil exporters from West Asia and Africa. India, once a marginal player in the world oil market, is now a valued customer providing demand security for oil exporters.

This book systematically examines India's oil and gas trade, which makes it the world's third largest importer of oil after China and the US. It explores the changing patterns of oil demand and supply, and the growing market for natural gas, renewable energy, biofuel, and alternative sources of energy. Further, the volume discusses a range of issues that affect India's position in the global energy econom, y such as

The geographic shifts in energy production and trade; international relations and economic sanctions that affect the oil trade;

India's quest for energy security; and contest with China for oil assets;

Building new partnerships, and investing in stable, oil-rich countries like the US and Canada, while keeping up existing energy relations with Saudi Arabia, the UAE and Kuwait;

Using market mechanisms to ensure energy security.

Topical and comprehensive, this book in The Gateway House Guide to India in the 2020s series will be useful for scholars and researchers of international relations, geopolitics, foreign policy, security and strategic studies, energy studies, West Asia studies, South Asian studies, and international trade. It will also be of interest to policymakers, diplomats, career bureaucrats, and professionals working with think tanks, academia and multilateral agencies, media agencies, and businesses.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que India and the Changing Geopolitics of Oil est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à India and the Changing Geopolitics of Oil par Amit Bhandari en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Politics & International Relations et Geopolitics. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

April 2020 saw an unprecedented event in the world oil market – the price of West Texas Intermediate (WTI), one of the most widely traded benchmarks globally, fell to –$36/barrel as the April contracts neared expiry. Meaning, you had to pay your customer $36/barrel to take your oil away. Prices went negative because of the COVID-19 pandemic – global oil demand tanked by 30% in a matter of weeks while production continued at pre-crisis levels, leading to a glut of oil. Production from operational oil fields cannot be switched on or off like a tap, so fresh oil continued to reach the market. Dumping the oil is an environmental crime and not possible – so traders holding oil purchase contracts ended up paying large amounts to buyers willing to pick up this oil. Eventually, the US ran out of places to store this oil. Supertankers, which can carry up to 2 million barrels of oil, were chartered not to move the oil but to store it.

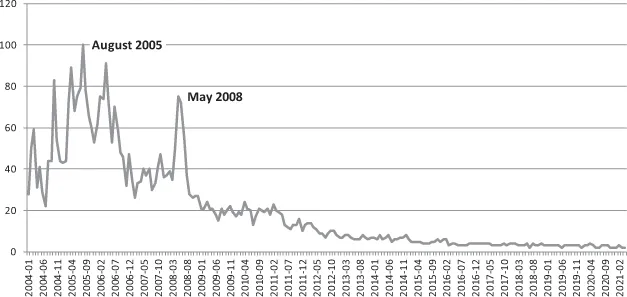

This is a complete about-turn compared with the early 2000s, when fears of peak oil were rife. As per the peak oil theory, the world oil production was set to reach a peak (2006 by some estimates), after which it would enter a terminal decline. The ever-reducing supply would keep pushing up prices, making abundant and affordable oil a thing of the past. Lacking cheap energy, poor countries like India would be forever stuck at lower incomes. Hundreds of books dealing with the subject and its various dimensions have been written. Luckily for us, it didn’t happen. Google Trends shows that interest in peak oil peaked around 2005 and has since abated.

Peak oil was killed by a mix of supply- and demand-driven factors. World oil supply has increased and has become more diversified because of increasing production of unconventional oil, primarily shale-oil in the US and oil-sands of Canada. At the same time, oil demand growth has slowed down – it has actually reversed in most of the high-income European countries and Japan – a mix of ageing population and improving energy efficiency. The increasing use of renewable energy, particularly electric vehicles, has also played a role. As a result, the focus is now on peak-demand – the point at which global oil demand will reach a peak and then start to decline. A lot of the known oil reserves are destined to never leave the ground. The April trade in WTI, precipitated by COVID-19, showed what happens when supply exceeds demand by a big margin.

Figure1.1 Peak Oil – No Longer Peaking

Moreover, COVID-19 itself may become a long-term factor in shaping how energy markets develop. Early projections suggested that the global oil demand for 2020 would shrink by an unprecedented 8.1 million barrels per day1 – almost 8% of all oil consumption. Not all of this will come back even as the world economy recovers. For instance, air travel – which constitutes an important part of oil consumption – may not recover to pre-COVID levels for years, if ever. Some of India’s tech giants – such as TCS2 and Infosys,3 which employ hundreds of thousands of workers – may introduce permanent ‘work from home’ policies, so that only a small fraction of their staff needs to be physically present at the workplace, reducing the need for commutes. Workplaces have become used – for want of better options – to video-conferencing apps, which may also reduce the requirement for business travel in the long run. On the flip side, people may be more reluctant to use public transport and opt for personal vehicles, due to health concerns.

All of these trends have big implications for India, which is the world’s third largest user and importer of oil, with a growing demand.

Saudi Arabia's bet

Peak oil turned out to be a bubble. Is peak-demand going to be the same? Many oil producers, who have the most to lose in such a scenario, are not betting on it. Saudi Arabia, which has, for decades, been the poster boy of a conservative, oil-fuelled monarchy, is trying to change, socially and economically, under the leadership of Crown Prince Muhammad bin Salman (MBS). The Vision 2030, a document first unveiled in 2016, speaks of diversifying the Saudi economy away from oil and converting the Kingdom into an investment powerhouse, Saudi Aramco into a global industrial giant and the Sovereign Wealth Fund (SWF) into the world’s largest wealth fund.

It is not possible to change the economic base of the country without also changing the society. Thus, social liberalism goes hand in hand with economic liberalism. In 2019, Saudi Arabia cut down gender segregation in public places, finally allowed women to drive cars and permitted music concerts – hitherto banned. On the economic front, the Kingdom is promoting a new finance hub – the King Abdullah Economic City as well as other cities being set up for entertainment and tourism. One of the biggest projects is a city called Neom, on the northern Red Sea coast of the Kingdom, which will function as a smart city and a tourism hub.

To fund these new investments/diversifications, the Kingdom announced it will be listing its prime asset – Saudi Aramco, the national oil company. First talked about in 2016, the IPO was projected to raise $100 billion for the Kingdom, enabling new investments.4 The IPO was temporarily shelved and then scaled down by almost 70% – eventually to a still massive $25.4 billion for 1.5% shares in the company.5 Post IPO, Aramco has become the most valuable company in the world – worth $1.7 trillion at its IPO price and touching $2 trillion as well in the weeks following the IPO.

One of the reasons for the Aramco IPO was to create a kitty for future investments, many of them to be made via the SWF of the Kingdom. This SWF has made large investments in Uber and Tesla, two of the best-known start-ups globally,6 and with business models that can dramatically alter the global energy demand scenario, and Saudi Arabia’s fortunes. Saudi Arabia is clearly trying to hedge its bets against a future where oil may no longer be central to the fortunes of the world economy. Saudi Arabia’s caution is warranted – major trends are under way that may reshape the global energy scenario.

Oil demand: from West to Asia

The two most closely followed numbers in the oil world are the prices of Brent and WTI. Brent is the name for the light, sweet crude produced from a North-Sea oil field owned by Royal Dutch Shell. Over time, it has become the most closely followed benchmark for pricing of oil contracts, much like how Libor is used to set interest rates in financial contracts. Other oils are priced at a certain discount (or premium, as the case may be) to the prevailing price of Brent crude. Production from the Brent field first began in 1976 – the field is currently being decommissioned.7 WTI is an even older benchmark, with price records going back to over 70 years. Like Brent, WTI is also a light, sweet crude. Unlike Brent, it doesn’t come from a single field but is a blend of oils from several fields.

The two most important historical oil benchmarks are both Western crude oils, simply because for most of the recorded oil age, the West has been the largest consumer of oil. In 1973, the year of the first oil-shock, seven of the top eight oil consumers were either the US or its allies. India didn’t even figure in the top ten users of oil. Countries such as Sweden and Belgium – which have populations less than half of India’s major metros such as Mumbai and Delhi – consumed more oil than all of India at that time.

And how things have changed! India is now the third largest user of oil, and its oil consumption has gone up more than tenfold – consuming as much oil as Germany, France and the UK combined! China’s oil consumption has increased in a similar manner – it is now the second largest consumer of oil after the US. Over the same period, Western countries such as Japan, Germany and France have seen their oil consumption decline – a mix of improved energy efficiency, ageing populations and greater use of renewable energy. Because of this shift, China had displaced the US as the world’s largest oil importer. India comes in at the third place. Thus, the oil trade, which was earlier from the Middle East to the West, is now shifting to the East.

Table1.1 Major Oil Consumers: Then and Now

1973

2018

USA

17,318

20,456

USSR

5,981

3,228 (Russian Federation)

Japan

5,265

3,854

Germany

3,249

2,321

France

2,499

1,607

UK

2,228

1,618

Italy

1,983

1,253

Canada

1,682

2,447

China

1,058

13,525

India

474

5,516

World

55,658

99,843

Figures in 000 barrels/day.

Source: BP Statistical Review of World Energy.

Oil (and energy) demand of Asian countries, such as India, is going to increase further, while consumption in Europe (and West, in general) is going to decline due to the following two factors:

Higher growth: Because of its lower base (income), the Indian economy will grow much faster than the world average for many years to come. In 2019, the IMF projected India’s 2020–2024 GDP growth at over 7%, despite a slowd...

Table des matières

Cover

Half Title

Series Page

Title Page

Copyright Page

Table of Contents

List of figures

List of tables

1 Flux in the energy world

2 India's quest for energy security

3 Flashpoints and chokepoints

4 Using market mechanisms for energy security

5 Meeting India's energy challenge

Index

Normes de citation pour India and the Changing Geopolitics of Oil

APA 6 Citation

Bhandari, A. (2021). India and the Changing Geopolitics of Oil (1st ed.). Taylor and Francis. Retrieved from https://www.perlego.com/book/2995521/india-and-the-changing-geopolitics-of-oil-pdf (Original work published 2021)

Chicago Citation

Bhandari, Amit. (2021) 2021. India and the Changing Geopolitics of Oil. 1st ed. Taylor and Francis. https://www.perlego.com/book/2995521/india-and-the-changing-geopolitics-of-oil-pdf.

Harvard Citation

Bhandari, A. (2021) India and the Changing Geopolitics of Oil. 1st edn. Taylor and Francis. Available at: https://www.perlego.com/book/2995521/india-and-the-changing-geopolitics-of-oil-pdf (Accessed: 15 October 2022).

MLA 7 Citation

Bhandari, Amit. India and the Changing Geopolitics of Oil. 1st ed. Taylor and Francis, 2021. Web. 15 Oct. 2022.