In The Money Markets Handbook Moorad Choudhry provides, in one comprehensive volume, the description, trading, analysis and calculations of the major markets around the world, providing worked examples and exercises throughout to provide a landmark publication on this important topic. Unique features, including a list of conventions and trading rules in virtually every market in the world, means that this book is relevant to virtually every money market in the world.

Includes an in depth treatment of repo markets, asset and liability management, banking regulatory requirements and other topics that would usually be found only in separate books

Written with clarity in mind, this book is vital reading for anyone with an interest in the global money markets

Features coverage of derivative money market products including futures and swaps, and the latest developments not covered in current texts

Frequently asked questions

How do I cancel my subscription?

Simply head over to the account section in settings and click on “Cancel Subscription” - it’s as simple as that. After you cancel, your membership will stay active for the remainder of the time you’ve paid for. Learn more here.

Can/how do I download books?

At the moment all of our mobile-responsive ePub books are available to download via the app. Most of our PDFs are also available to download and we're working on making the final remaining ones downloadable now. Learn more here.

What is the difference between the pricing plans?

Both plans give you full access to the library and all of Perlego’s features. The only differences are the price and subscription period: With the annual plan you’ll save around 30% compared to 12 months on the monthly plan.

What is Perlego?

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 1000+ topics, we’ve got you covered! Learn more here.

Do you support text-to-speech?

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more here.

Is The Money Markets Handbook an online PDF/ePUB?

Yes, you can access The Money Markets Handbook by Moorad Choudhry in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over one million books available in our catalogue for you to explore.

Part of the global debt capital markets, the money markets are a separate market in their own right. Money market securities are defined as debt instruments with an original maturity of less than one year, although it is common to find that the maturity profile of banks’ money market desks runs out to two years.

Money markets exist in every market economy, which is practically every country in the World. They are often the first element of a developing capital market. In every case they are comprised of securities with maturities of up to twelve months. Money market debt is an important part of the global capital markets, and facilitates the smooth running of the banking industry as well as providing working capital for industrial and commercial corporate institutions. The market provides users with a wide range of opportunities and funding possibilities, and the market is characterised by the diverse range of products that can be traded within it. Money market instruments allow issuers, including financial organisations and corporates, to raise funds for short term periods at relatively low interest rates. These issuers include sovereign governments, who issuer Treasury bills, corporates issuing commercial paper and banks issuing bills and certificates of deposit. At the same time investors are attracted to the market because the instruments are highly liquid and carry relatively low credit risk. The Treasury bill market in any country is that country’s lowest-risk instrument, and consequently carries the lowest yield of any debt instrument. Indeed the first market that develops in any country is usually the Treasury bill market. Investors in the money market include banks, local authorities, corporations, money market investment funds and mutual funds and individuals.

In addition to cash instruments, the money markets also consist of a wide range of exchange-traded and over-the-counter off-balance sheet derivative instruments. These instruments are used mainly to establish future borrowing and lending rates, and to hedge or change existing interest rate exposure. This activity is carried out by both banks, central banks and corporates. The main derivatives are short-term interest rate futures, forward rate agreements, and short-dated interest rate swaps such as overnight-index seaps.

In this chapter we review the cash instruments traded in the money market. In further chapters we review banking asset and liability management, and the market in repurchase agreements. Finally we consider the market in money market derivative instruments including interest-rate futures and forward-rate agreements.

Introduction

The cash instruments traded in money markets include the following:

Time deposits;

Treasury Bills;

Certificates of Deposit;

Commercial Paper;

Bankers Acceptances;

Bills of exchange.

In addition money market desks may also trade repo and take part in stock borrowing and lending activities. These products are covered in a separate chapter.

Treasury bills are used by sovereign governments to raise short-term funds, while certificates of deposit (CDs) are used by banks to raise finance. The other instruments are used by corporates and occasionally banks. Each instrument represents an obligation on the borrower to repay the amount borrowed on the maturity date together with interest if this applies. The instruments above fall into one of two main classes of money market securities: those quoted on a yield basis and those quoted on a discount basis. These two terms are discussed below. A repurchase agreement or “repo” is also a money market instrument and is considered in a separate chapter.

The calculation of interest in the money markets often differs from the calculation of accrued interest in the corresponding bond market. Generally the day-count convention in the money market is the exact number of days that the instrument is held over the number of days in the year. In the UK sterling market the year base is 365 days, so the interest calculation for sterling money market instruments is given by (1.1):

(1.1)

However the majority of currencies including the US dollar and the euro calculate interest on a 360-day base so the denominator in (1.1) would be changed accordingly. The process by which an interest rate quoted on one basis is converted to one quoted on the other basis is shown in Appendix 1.1. Those markets that calculate interest based on a 365-day year are also listed at Appendix 1.1.

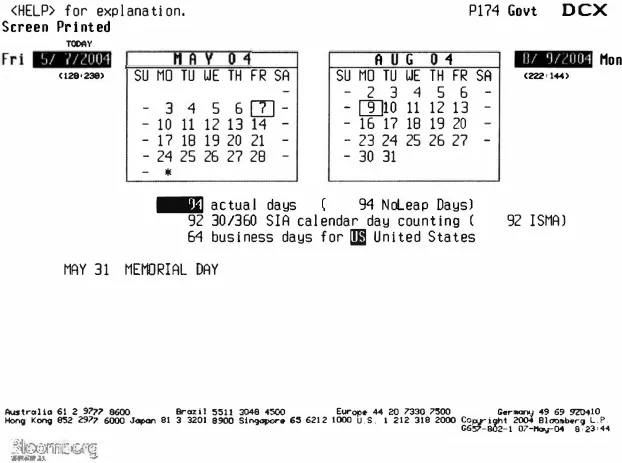

Dealers will want to know the interest day-base for a currency before dealing in it as FX or money markets. Bloomberg users can use screen DCX to look up the number of days of an interest period. For instance, Figure 1.1 shows screen DCX for the US dollar market, for a loan taken out value 7 May 2004 for a straight three-month period. Ordinarily this would mature on 7 August 2004, however from Figure 1.1 we see that this is not a good day so the loan will actually mature on 9 August 2004. Also from Figure 1.1 we see that this period is actually 94 days, and 92 days under the 30/360 day convention (a bond market accrued interest convention). The number of business days is 64, we also see that there is a public holiday on the 31 May.

Figure 1.1 Bloomberg screen DCX used for US dollar market, three-month loan taken out 7 May 2004

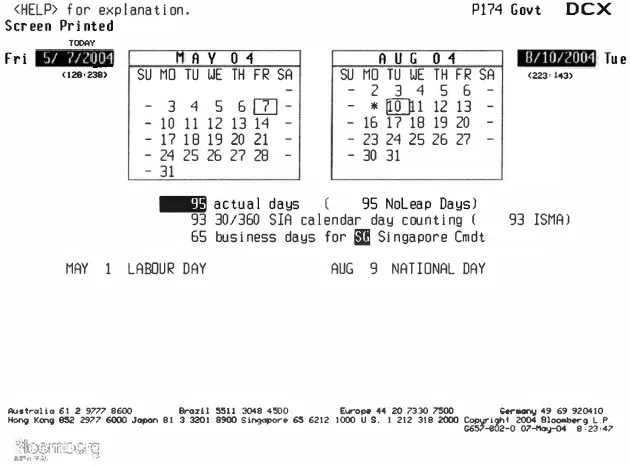

For the same loan taken out in Singapore dollars, look at Figure 1.2. This shows that the same loan taken out for value on 7 May will actually mature on 10 August, because 9 August 2004 is a public holiday in that market.

Figure 1.2 Bloomberg screen DCX for Singapore dollar market, three-month loan taken out 7 May 2004

Settlement of money market instruments can be for value today (generally only when traded in before mid-day), tomorrow or two days forward, known as spot.

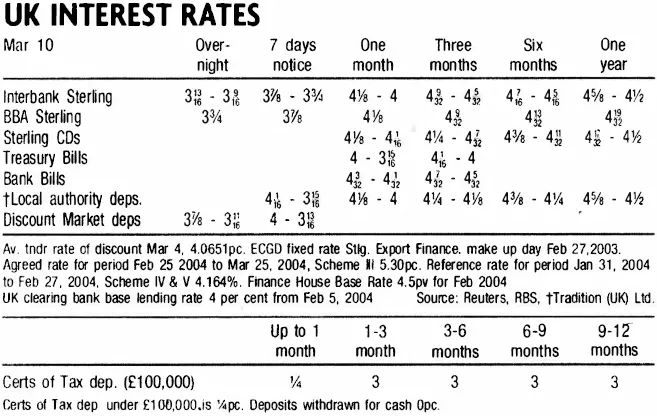

Figure 1.3 London sterling money market rates. Extract from Financial Times, 11 March 2004.