Macroeconomics has always played host to contesting schools of thought, but recent events have exacerbated those differences. To fully understand the subject, students need to be aware of these controversies. Rethinking Macroeconomics: A History of Economic Thought Perspective introduces students to the key schools of thought, equipping them with the knowledge needed for a true understanding of today's economy.

The text guides the reader through multiple approaches to macroeconomic analysis before presenting the data for several critical economic episodes, all in order to explore which analytical method provides the best explanation for each event. It covers key background information on topics such as the basics of supply and demand, macroeconomic data, international trade and the balance of payments, the creation of the money supply, and the global financial crisis. This anticipated second edition contains new chapters on Modern Monetary Theory, the Japanese economy, the European Union, and the COVID-19 crisis, bringing the story up to date and broadening the international coverage.

Offering the context that is missing from existing introductory textbooks, this work encourages students to think critically about received economic wisdom. This is the ideal complement to any introductory macroeconomics textbook and is ideally suited for undergraduate students who have completed a principles of economics course.

The book is fully supported with additional online resources, which include lecture slides and an instructor manual.

Frequently asked questions

How do I cancel my subscription?

Simply head over to the account section in settings and click on “Cancel Subscription” - it’s as simple as that. After you cancel, your membership will stay active for the remainder of the time you’ve paid for. Learn more here.

Can/how do I download books?

At the moment all of our mobile-responsive ePub books are available to download via the app. Most of our PDFs are also available to download and we're working on making the final remaining ones downloadable now. Learn more here.

What is the difference between the pricing plans?

Both plans give you full access to the library and all of Perlego’s features. The only differences are the price and subscription period: With the annual plan you’ll save around 30% compared to 12 months on the monthly plan.

What is Perlego?

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 1000+ topics, we’ve got you covered! Learn more here.

Do you support text-to-speech?

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more here.

Is Rethinking Macroeconomics an online PDF/ePUB?

Yes, you can access Rethinking Macroeconomics by John F. McDonald in PDF and/or ePUB format, as well as other popular books in Economics & Economic History. We have over one million books available in our catalogue for you to explore.

How can economics be defined? The standard definition begins with the notion that a society has limited resources that can be used for different purposes. Economics studies the choices for the use of those resources made by individuals, firms, governments, and society as a whole. Furthermore, economics focuses on the incentives that influence and reconcile those choices.

The part of economics that studies the choices made by individual people and businesses is called microeconomics. Those choices are added up to be the study of markets. The choices made by governments in the use of resources and in the regulation of markets are also the purview of microeconomics. Furthermore, economists contend that those choices are rational. Choices are made in response to incentives – monetary and otherwise. Microeconomics looks at the economy from the “bottom up.”

Macroeconomics is the study of the behavior of the economy as a whole. The idea is to understand the determinants of aggregate economic activity – the total output of goods and services and its main components, unemployment, inflation, and other indicators of aggregate economic activity. Macroeconomics is concerned with identifying policies that will improve the performance of the aggregate economy, such as reducing the volatility of the economy and keeping unemployment and inflation low. The subject is of obvious importance. Macroeconomics looks at the economy from the “top down.”

At this time (2021), the field of macroeconomics continues to undergo quite a lot of rethinking. Several schools of thought are, or least their adherents think they are, in contention to provide the best model for future thinking and policy action. In fact, contending schools of thought have been in the pot for decades, but the financial crisis and deep recession that started in 2007 and 2008 have brought the pot to a boil. What is an educated person to think, and do? The editorial pages and the semi-popular books on economics present the views of various economists and other experts, and the voracious reader can come away very confused. The person who reads only the authors who represent one particular school of thought does not come away confused but, I would submit, does not come away educated.

The purposes of this book are to introduce you to the field of economics in general, and then to explore these contending schools of thought in the context of those facts that Secretary Schulz mentioned. At the same time, we shall be mindful that details are confusing, and that emphasis is needed to get at the real meaning of things. The schools of thought – Keynesian, Monetarist, and others – are described first. Then macroeconomic data for several time periods for the United States and a few other nations are presented. The last step is to assess the ability of each of the schools of thought to provide a reasonable explanation for what happened in each of those time periods. It may be that one school of thought is not “best” for all of the selected time periods. Indeed, real-world experience produced a rethinking of macroeconomics in the 1920s, the 1930s, the 1970s, the 1980s, and in the past few years. The various schools of thought were born out of the seeming failure of the prevailing macroeconomic theory. The educated person deserves to know what’s what and who’s who of all of this.

The most important example of this rethinking was conducted by J. M. Keynes in the General Theory of Employment, Interest, and Money (1936). The General Theory was written during the depths of the Great Depression of the early 1930s, and it can be regarded as the founding document for the field of macroeconomics. It is a product of its time, to be sure. Indeed, Keynes believed that useful economics is a product of its time. His purpose was to develop a theory that explained the obvious facts that the capitalist economies of the day were not generating anything close to full employment, and that this state of affairs had existed for several years. The economic theory of the time, which Keynes called the postulates of classical economics and dismissed in a few pages, was not capable of providing an explanation of these overwhelming facts.

Progress in economic analysis and policy making (and in other scientific fields as well) proceeds by

being confronted with facts that cannot be explained by the existing theories,

devising new theoretical explanations (or modifying the existing theories) so as to account for the new facts,

working out the implications of the new theory,

conducting tests of the new theory, and

using the new theory to make economic policy in those situations with the conditions contemplated in the new theory.

The highest accolades in economics often are conferred on those who devise the new theory that turns out to be successful. Keynes provided the new theory but devoted very little space in the General Theory to empirical testing or policy recommendations. Indeed, the lack of details pertaining to economic policy is striking and perhaps is surprising, given that much macroeconomic policy now has been based on Keynesian principles for decades. But Keynes’s purpose in his book was to develop a new theory that could explain, to the satisfaction of his fellow economists, the overwhelming facts of the depression in the private economy. Here is a famous quote attributed to Keynes: “When the facts change, I change my mind. What do you do sir?” Unfortunately, there is no evidence that he ever said this, but it sounds like something he would have said.

As I neared the completion of the first version of this book, a new book by the economist Dani Rodrik (2015) arrived. The title of the book, Economics Rules, means that economics as a discipline operates with certain rules. The rules include (2015, p. 213):

Economics is a collection of models; cherish their diversity.

It’s a model, not the model.

Make your model simple enough to isolate specific causes and how they work, but not so simple that it leaves out key interactions among causes.

Unrealistic assumptions are OK; unrealistic critical assumptions are not OK.

To map a model to the real world, you need explicit empirical diagnostics, which is more craft than science.

A summary of Rodrik’s view is that economics expands horizontally by adding more models that can be used to understand particular situations. There is no one model that explains all situations. Models that fail in certain situations are not discarded but rather saved and still used to understand other situations to which they do apply. This book is written in this spirit. Macroeconomics consists of a collection of models that keeps expanding because the world and the questions we ask keep changing.

This chapter introduces you to the background information and tools that you need to read the rest of the book.

The big questions

The big questions that must be answered in any economy are:

what goods and services to produce,

how to produce those goods and services, and

for whom shall the goods and services be produced?

Any economy is somehow organized to allocate its scarce resources to produce goods and services for people.

How can we judge how well the society has accomplished these basic tasks? One method is to determine the efficiency with which the resources have been used. Could more have been produced with the given resources? Could more of one good have been produced without a reduction in the production of anything else? Or would an increase in the output of one good have required a reduction in the output of another good? If the answer to the first two questions is “yes,” then the society has not been as efficient as possible.

A second method for judging the outcome of an economy is the fairness with which the goods and services are distributed to the people (the “for whom” question). If the society has, in principle, enough resources to provide for the basic needs of all, does it? Beyond that, does the society generate a highly unequal distribution of goods and services even if the basic needs of all are met? Does such an unequal outcome meet with the approval of most people? The issue of distribution has been argued by economists, philosophers, and everyone else since the beginning of civilization. The economist falls back on a simple rule that mirrors the rule for production efficiency. If the well-being of one person can be improved without reducing the well-being of any other person, then make the change indicated, especially if that one person is poor compared to the majority of society.

In a nutshell, the economic way of thinking, always in an economist’s head, is the understanding that a choice is a tradeoff – something must be given up to get something else. An efficient economy, as defined earlier, is one in which this rule applies. In order to have more of one good, you must give up the opportunity to have the same amount of some other good. What must be given up is called the opportunity cost. More of one good requires giving up the opportunity to have some of the other good. Note that opportunity cost occurs at the “margin” – one more of this means less of that. So how are those choices made? As noted, economists believe that choices are made in response to incentives. Rational choice involves reckoning the opportunity cost of an action in comparison to its benefits. For example, a person goes shopping for food. The price of steak is $9.00 a pound. The decision to buy the pound of steak means that, ultimately, the person has $9.00 less to spend on other items. That is what a price means, after all. Is a pound of steak worth the price to the shopper? Only that person can answer the question, of course.

How does production occur? How are the “what” and “how” questions answered? An economy uses what are called the basic “factors of production” to produce goods and services. Those factors are:

land

labor (both quantity and quality)

capital (plants, office buildings, machinery, etc.)

technology

entrepreneurship (the capacity to recognize what goods and services to produce and the ability to organize the inputs to get the job done)

The quality of labor is otherwise known as “human” capital – knowledge, experience, and expertise. College students are considered by economists to be investing in human capital (at least some of the time). But experience on the job also counts as valuable human capital.

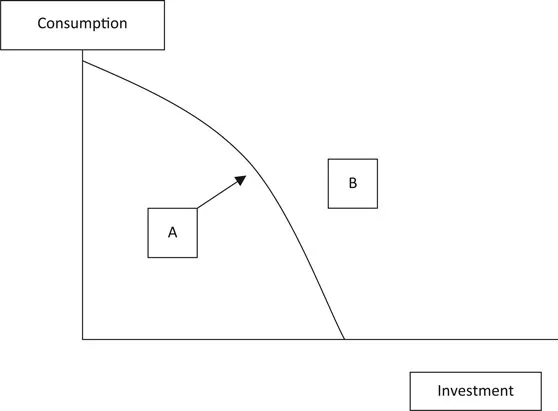

Basic concepts I: production possibilities

A simple diagram captures the “what” and “how” questions. Consider Figure 1.1. On the vertical axis we measure units of an all-purpose consumption good, and the horizontal axis is used to chart units of investment goods. Investment goods are things such as plants, equipment, and houses that are used to produce consumption goods in the future. The diagram depicts consumption and investment, because these are basic concepts in macroeconomics. In essence, Figure 1.1 is showing the options available for the production of goods and services for use now versus the capacity to produce goods and services later – the now-versus-later choice. The curve is called the production possibilities curve.

FIGURE 1.1 Production Possibilities

The diagram is drawn for given supplies of the basic factors of production – land, labor, capital, technology, and entrepreneurship. Any point on the curve shows the maximum amount of consumption goods that can be produced given the indicated amount of investment goods – hence...