![]()

CHAPTER 1

An Introductory View to Banking, Development Banking, and Treasury

We have mentioned that our focus is going to be any treasury activity carried out by a traditional financial institution, a development bank, a corporation, or a government. When discussing the issuance of debt we will indeed draw examples from all four types of entities listed; however, when the objective will be a deeper understanding of several concatenated activities, we shall focus on the former two types of institution: investment banks and development banks. Furthermore, our view will narrow toward development banking not only because it is a special concern of ours but also because, in its simpler type of financial activity, it offers an opportunity to isolate clearly the different functions of a bank. A development institution that uses the tools of investment banking (we shall see in Section 1.6.1 that some do not) offers the simplest type of banking activity, a type made up of instruments upon which traditional investment banks have built increasingly more sophisticated ones; the higher level of sophistication, in our situation, does not translate necessarily to a better understanding.

In this chapter we shall introduce the fundamental activities of a financial institution as lending, borrowing, investing, and asset liability management (ALM); we shall try to present them in this order so as to follow the business line that goes from the client’s need for a loan, through the bank’s need to fund the loan, and then invest the income generated and hedge the potential risks. We shall then conclude with a sketch of the structure of a typical financial institution and a definition of the type of development bank we shall be dealing with.

1.1 A REPRESENTATION OF THE CAPITAL FLOW IN A FINANCIAL INSTITUTION

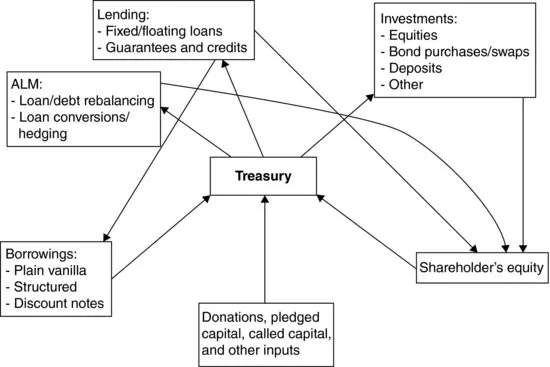

Before offering an introduction to fundamental banking activities, let us focus on a schematic representation of the flow of capital within a financial institution. As we have said before, we shall use a development institution as an example, since it encapsulates at least the fundamental aspects of banking plus a few additional features.

In Figure 1.1 we show the capital inflow and outflow to the treasury of a development institution. In Section 1.6 we describe which type of institutions obtain their funds in which particular way, but here we attempt to describe in a general way how development institutions obtain their funds and what they do with them.

A development institution, like many institutions, has shareholders who have brought a certain initial amount of equity to the institution and own a share of it. The sum of all these contributions constitutes the majority of the institution’s equity. Additionally, and this is peculiar to development organizations, there are donors’ contributions. These contributions can be made either by the shareholders themselves or by other entities; they can actually be given to the institution or they can be pledged, meaning that they remain with the donor until the institution asks for it. These contributions can be offered or, when coming from the shareholders, they can be requested by the collection of shareholders.

An additional inflow of capital, and the main topic of this book, is debt. In Section 1.3 we introduce how borrowing fits within the general activity of an institution and define the varieties of those instruments. Throughout the rest of the book we describe how debt is priced.

The main outflow, and the reason for being a development institution or a commercial bank, is lending. In Section 1.2 we introduce how lending takes place in relation to clients’ needs. Income generated by loans is used to repay the debt; any additional return flows into the institution’s equity.

The role played by the investment unit of a development institution will be introduced at a general level in Section 1.4 and in more detail in Section 6.4.2. Its main mandate is essentially to prevent depreciation in the institution’s equity and to provide emergency liquidity to its lending unit. Investments’ returns flow back into the institution’s equity.

Finally, the institution’s capital is also used for asset liability management, which will be introduced in Section 1.4 at a general level and then in detail in Chapter 7. Its main mandate is to balance debt and income and to hedge high-level exposures. It is an activity that should be more or less return neutral; however, any positive return would flow into the institution’s equity.

Having sketched the general movement of capital within a development institution, we can now begin introducing its main activities in more detail before—in the subsequent chapters—getting into even greater detail by adopting more analytical tools.

1.2 LENDING

A bank is a firm whose core business is dealing with money itself. A bank exists and profits from making money available to others. To make money available is an intentionally vague expression because the ways banks inject liquidity (a favorite journalese expression meaning helping to increase the circulation of money) into the world are multiple and some are more direct than others. The simplest, and the one we shall focus on, is through lending money to whoever needs it (and, of course, qualifies for it).

A loan is the main instrument of lending and the one we shall discuss at length throughout the book. In Section 3.1.1 we give a rigorous definition of it, in Section 3.3.1 we discuss its valuation, and in Chapter 7 we discuss its relationship to debt. Here we are simply going to introduce a loan in the context of a description of the activity of a bank. If we allow for the statement that, irrespective of the sophistication of a banking activity, the business of a bank is lending, we can simply focus on loans, and for that matter the activity of a development bank is sufficient for our discussion. Any additional activity a traditional financial institution, such as an investment bank, carries out can be seen as built on this.

Who are the clients facing a development bank, the entities needing a loan? A typical client of a development institution is a sovereign or private entity most often associated with the developing world; such client would seek the help of a development bank because to do the same in the capital markets would be too expensive or downright impossible. The need for a loan can be associated with a more or less specific development project that the sovereign or corporate entity envisages to carry out. The term development project is vague but we can imagine it including building schools and hospitals, developing infrastructure and power sources, even developing a basic capital market. We can imagine it excluding unnecessarily the strengthening of armed forces or building infrastructures closely linked to the ruler or the ruling party (e.g., a road to the ruler’s estate).

Not all projects benefit from the same type of loan, and the role of a development institution is to construct the lending instrument around the needs of the client. We now present some of the possible types of loans in the context of the type of project.

- Loan versus credit or guarantee: The first choice facing a development institution offering financial help to a borrower is whether this help should take the form of a loan, a credit, or a guarantee. A loan is an instrument where the repayment of the principal is linked to some market-driven variable; we leave this vague but it means that irrespective of whether the interest rate is fixed or floating (see the following), it is driven by some market considerations. A credit on the other hand is an instrument where the repayment is usually made of a nominal (small) rate. Finally, a guarantee is not an offer of funds but a guarantee to honor a promise made by a borrower that an investor will purchase a bond issued by some country with the understanding that, in case the borrowing country defaults, the development institution wil step in to honor the debt. In general, the wealthier the borrower, the more likely it will be offered a loan rather than the other two instruments. Another general rule is that the size of a credit or a guarantee is usually smaller than the size of a loan.

- Bullet versus amortizing loans: A project that might be more or less capital intensive and it might offer returns in a more or less gradual way. A way for the lending institution to accommodate the needs of the client is to issue a loan with a specific repayment profile.

A loan (we shall see this in more formal detail later) consists of a series of repayments of interest and principal, with the principal, as the name suggests, being the main component of the loan. Should the principal repayment prove to be difficult for the borrower, a solution is made available through a bullet loan in which the borrower throughout the life of the loan repays only the interest1 and the principal is returned only at maturity. Let us imagine that the borrower needs the funds to build up the country’s energy industry; these projects, ranging from dams to oil exploration, usually require a large initial investment, a long time to build, and then must produce a fairly regular source of income. During the build-up period it would be difficult for the borrower to repay the principal, therefore, in this situation, for example, a bullet loan would be ideal.

A lender is, however, hesitant to issue too many bullet loans. This will be treated more formally when dealing with the issue of credit, but it is easy to see how the further into the future we push the repayment of the main part of the loan, the more—particularly when dealing with countries and projects fraught with uncertainty—we place ourselves in a riskier situation. Because of this, the more standard form of loan is an amortizing loan, one where, at each interest paying date, the principal upon which the interest is calculated is partly repaid.

- Fixed-versus floating-rate loans: The interest repayments on a loan are a percentage amount that can be either the same at each repayment date (a fixed-rate loan) or variable, linked to some external parameter (a floating-rate loan). The choice of loan on the part of the borrower and the lender will be mainly driven by considerations linked to the financial markets of the currency in which the loan has been issued. The volatility of interest rates and the expected levels of inflation, all compounded by the length of the loan, will be deciding factors in the choice. Similar to the previous situation in which the choice was about which repayment profile, the choice of fixity in the interest repayments will be a balance between the borrower’s needs and the lender’s ability to deal with financial risk.

Development banks are typically very risk averse and will usually try to convert both costs (from their own borrowing, which we shall see later) and income (from loans repayments) into an easy-to-interpret and manage cash stream. Fixed- and floating-rate loans offer the lender different risk profiles with typically a preference for floating-rate loans.2

- The currency of the loan: An important issue is the currency in which the loan is offered, important also because the currency will decide which interest rate regime will govern the loan (i.e., if the loan is in currency X, it will be X interest rates that both borrower and lender will examine in their decision for a floating- or fixed-rate loan).

The return on the investment the borrowing entity is hoping to obtain will drive, as it did in the previous cases, the choice of currency of the loan. We mentioned the example of oil extraction as a possible project: should the project be successful, the income generated will be in U.S. Dollars (USD) since oil is a global commodity priced in USD. The borrowing country will then be motivated to take a loan in USD. In the case, for example, of the construction of a dam to provide electricity to local customers (who are expected therefore to pay for consumption in local currency) the income generated will be in local currency and therefore the borrowing country would prefer the loan to be in local currency. We can easily see how from the borrower’s point of view it would be desirable to match, currencywise, the income stream with the debt stream.

A similar and therefore symmetrical wish is on the lender’s part. Development banks are usually financed (as we shall see in the following section) in strong currencies3 and therefore would like to match the income they receive with the costs they face. A development bank would rather issue a USD loan than a local currency loan. Furthermore, a local currency loan is more subject to devaluation and/or inflation. An intuitive rule of thumb would be that anyone would rather receive income in a strong currency and pay debt in a weak one. As a consequence of this, local currency loans usually constitute a small, yet far from negligible portion of a loan portfolio.

The needs of a borrower are assessed at the moment of deciding the type and amount of loan. It is considered that the borrower will face certain costs throughout the life of the project, and the loan should be used to cover those costs. These costs, however, could change dramatically—driven by changes in the foreign exchange—after the issuance of the loan and this is because of a third currency other than the strong and the weak mentioned before (e.g., the borrower needs to purchase equipment in a third country). To manage this type of exposure there are also multi-currency loans that are issued, linked not to a single currency but to a basket of usually strong currency.

Here we have presented very briefly the type of choices facing a borrower and a lender when deciding which type of loan is best suited to the financing of a project. We now take on the point of view of the development institution and observe the different types of debt we can use to finance these loans.

1.3 BORROWING

The type of development institutions we are concerned with are those (we discuss them in more detail later) that use the tools of investment banking toward development, that is, they use their superior credit to borrow in the capital markets and then use the funds raised toward lending.

The debt profile of a development institution is one that should at the same time be in tune with its income profile (by income profile we mean the types of loans issued as discussed in the previous section) and capable of maximizing investors' needs. We shall discuss this at great length in the following chapters but, it is almost obvious, a bank should issue debt that can be considered as attractive as possible in the eyes of investors, otherwise not only will it be difficult to place, it will also be unduly onerous to serve.

In a way similar to the one ad...