The early 21st century has been a period of extreme fear and greed in the world's financial markets. Vast sums of wealth have been lost by some, but also made by others. Faith in the investment industry is now at its lowest-ever ebb, and the crisis remains far from resolution.Fear and Greed aims to prepare investors for the financial challenges and opportunities of the next few years. Having successfully guided his firm's investors through the turmoil since 2007, leading investment manager Nicolas Sarkis draws upon the lessons of history in order to illuminate the way ahead.In particular, Sarkis explores the plight of equities in the developed world since the millennium and considers when they might finally recover, as well as the likely effects of reducing government indebtedness upon markets. He also offers his insights into the outlook for stocks in emerging nations, for gold and for the single European currency.In addition to the prospects for the leading asset classes, Fear and Greed examines some of the biggest issues confronting the financial world as a whole. Sarkis focuses on the behaviour of central banks, regulators, and financial wrongdoers, especially in relation to their contribution to the current crisis.In this lively and engaging book, Sarkis offers a clear vision of the coming years and plenty of inspiration for investors.

- 240 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Chapter 1: A Lost Era in Equities

Following a century to remember, the stock market has suffered more than a period – of longer than a decade – that many investors would rather forget. Equities were the best performing asset class across much of the globe between 1900 and 2000, despite some spectacular upsets along the way. Since the dawn of the new millennium, however, shares in the developed world have delivered decidedly disappointing returns, inferior to those on most of the main rival asset classes.

A holding of worldwide shares worth $1 at the start of the 20th century would have grown to be worth $7,632 by the end of it. By comparison, $1 in worldwide bonds would have turned into just $75, while $1 of cash invested safely would have become only $54. The tables have since turned dramatically, however. In the first decade of the 21st century, a $1 investment in stocks would have grown to just $1.09 by 2010, versus $2.16 for bonds and $1.31 for cash. [1] Equities have significantly underperformed other assets.

Despite stocks’ dismal showing since the dawn of the new millennium, the cult of equity remains largely intact. The cornerstone of this faith is that shares are the best bet when it comes to investing over extended periods of time. Its scriptures come in the form of such compelling research as that of Professor Jeremy Siegel, whose bestselling book Stocks for the Long Run has even been praised as “the buy-and-hold bible.” [2] Unsurprisingly, one of this cult’s most popular messages today is that, after such a lousy run since 2000, the stock market ought soon to resurrect itself.

Rather than obediently joining the flock, there is a strong case for questioning the orthodoxy on equities. While common stocks have indeed been winners over the very long run, there have also been times when they have struggled for a sustained period. Even in the US – the best performing market of all and the one for which the most detailed data exists – there have now been four periods from the early 20th century to the present when stocks have peaked, declined and then taken a generation or more to recover their former heights. I call these periods lost eras.

Fairly little has been said about these lost eras in equities compared to other episodes within stock-market history. After all, spectacular bubbles like the late 1990s tech mania and awesome crashes like that of October 1987 make for much racier reading. As a result, ordinary investors are largely in the dark about the very existence of these lost eras, let alone about their characteristics or what caused them. For obvious reasons, the cult of equity’s high priests – the banks and brokerage houses that dominate the financial industry today – prefer not to dwell excessively on these inconvenient, but very significant, exceptions.

While less sophisticated players may well prefer to kneel and pray that the poor returns on stocks since 2000 will soon somehow be miraculously transformed into a new bull market, serious investors should instead delve into the history books. By understanding what happened during previous periods of equity famine, we will be better prepared to cope with the challenges of the latest one – and position our portfolios accordingly.

So, let’s begin by asking ourselves what exactly is a lost era in the stock market?

Defining a lost era

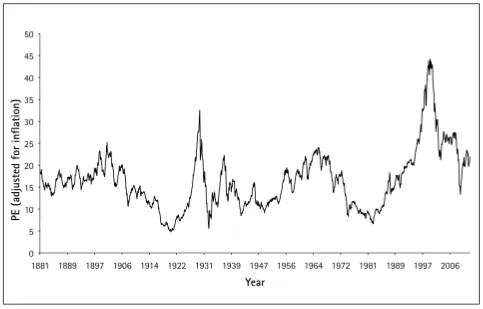

Looking at a chart of the price-to-earnings ratio (PE) of US equities adjusted for inflation over the past 140 years or so (Chart 1.1), these periods are easy enough to spot. Whereas the long-term tendency has evidently been for stocks to rise, there are also clearly some long stretches of time where the market has gone downwards or sideways in a persistent fashion. The beginning of each lost era is the point where the stock market makes a major high that is subsequently not surpassed for many years.

Chart 1.1 – S&P 500 price-to-earnings (PE) ratio after inflation, 1881 to 2012

Source: Robert J. Shiller [3]

The timing of the end of a lost era isn’t always quite as obvious as one might think, though. For two out of the three previous lost eras shown in Chart 1 – those that ended in 1920 and 1982 – the stock market’s absolute low also marked the start of the next long-term uptrend. Following the Wall Street Crash of 1929, however, stocks hit rock-bottom in 1932 but the market essentially then went sideways – albeit with some dramatic swings in each direction – until the next sustained uptrend finally got underway in 1949, some 17 years later. And it wasn’t for another decade still, until 1959, that the S&P finally regained its peak of 30 years earlier.

Measured from each stock-market peak to the time of the beginning of the next major uptrend, America’s three lost eras of the 20th century lasted some 14, 20 and 14 years respectively. From the peak of the previous uptrend to the absolute lows, the S&P 500 shed more than 60 per cent of its value after inflation in each of these three periods. Looking back even further to America’s two episodes of the early 19th century, stocks lost half and three-quarters of their real value. Interestingly, the three episodes in the 20th century were noticeably longer than the two lost eras of the 19th century, when the losses suffered were of a similarly major degree, but which nonetheless came to an end after seven years each time. We shall consider a possible reason for this later on. Of course, it is not all one-way traffic during a lost era. Stocks can rally mightily in these periods. Following the horrendous meltdown on Wall Street of 1929-32, to give just one example, the S&P soared by 132 per cent between 1935 and 1937. It then subsequently gave up more than 60 per cent of its value over the next five years. In Japan, where the Nikkei 225 stock index peaked in 1989 and remains depressed more than 20 years later, there have also been five occasions during that period where stocks have gained more than 50 per cent, only then to resume their long-term downtrend. These episodes merely serve to lure investors back into equities but end up leaving them disappointed – not to mention poorer – before very long.

Whereas lost eras have been the exception rather than the rule for the US, they have been far more ubiquitous in many other countries. French equities were trapped in a secular downtrend for more than half of the period between 1854 and 2000. [4] Adjusting for inflation, French stocks also declined in five decades of the 20th century. By way of comparison, British stocks declined in only two decades of the same period. [5]

Why lost eras occur

While awareness of the existence of lost eras is crucial for investors, it is only the first step. A much bigger challenge is explaining why these periods of equity famine actually occur in the first place. Today’s lost era in the West began in 2000, with the bursting of the technology bubble. One possibility, therefore, is that previous lost eras were also at least partly the result of bubbles having burst.

Bubbles

The mania for technology, media and telecom stocks that began in the late 1990s was a clear example of a bubble even before it burst – at least to the more far-sighted among investors. The NASDAQ 100 index – home to many firms from the hot industries of the day – soared by an incredible 1,092 per cent from the start of 1995 to its peak five years later. Such perpendicular gains are themselves often a warning sign that things are getting out of control.

Of course, spectacular stock-price increases can sometimes be justified – particularly if corporate earnings are growing at a similar pace or are projected to do so with good reason. But it is hard to argue that this was the case for the late 1990s. Not only did the US stock market as a whole reach its most extreme ever level of valuation in terms of earnings, but many of the favourite hi-tech companies of the day did not have any earnings – or even revenues, in certain cases.

To justify this orgy of speculation, enthusiasts claimed that the game had fundamentally changed. New technologies – such as the internet – were supposedly going to improve the economy’s potential to grow forever. Turning received wisdom on its head, equities were even argued to be less risky than government bonds, rather than more so. And conventional cash-flow based techniques were abandoned and even ridiculed as being outmoded.

Aside from the vertical increases in stock prices and the fanciful arguments that the old rules no longer applied, other prominent bubble characteristics were clearly in evidence in the late 1990s. Edward Chancellor – a leading authority on financial-market manias – has listed other generic features of a bubble, including rampant credit growth, corruption and blind faith in the authorities’ ability to prevent a sticky ending. [6] These traits were clearly evident in the 1990s tech bubble.

The other great lost era for equities of the present age also began with the implosion of a spectacular bubble. Japan’s Nikkei 225 index shot up by 469 per cent between the summer of 1982 and the end of 1989. This boom too was fuelled by a cocktail of inappropriately low interest rates, generous – and often irresponsible – lending by banks, and a widespread sense of confidence in the superiority of the Japanese ways of business and finance.

All of these elements were also present in spades during the decade known as the roaring 1920s. Easy credit stoked debt-fuelled speculation in Florida real estate, while Wall Street got carried away with such exciting modern technologies as mass-market versions of radio and the motor car. Excessive confidence in the investment outlook was best encapsulated by the contemporary economist Irving Fisher, who infamously remarked that “stocks have reached what looks like a permanently high plateau.” The Great Crash of 1929 got underway just three days later, wiping out much of the professor’s own fortune.

A big problem with the theory that lost eras result from bubbles bursting is that the 20th century’s other two lost eras in the US were not preceded by manias of the same sort. The 1960s did see something of a boom in the stocks of certain growth companies, in particular, as well as the initial proliferation of mutual funds. But the US stock market as a whole did not experience runaway price growth.

The S&P 500 index went up 84 per cent from the start of the decade to its peak in 1968. And while there was a big influx of novice investors into equities thanks to the arrival of mutual funds, the enthusiasm never came close to that of the late 1990s, where newcomers were so enthusiastic yet uninformed that they sometimes bought into a particular stock mistakenly, merely because its name or ticker was similar to that of a technology stock.

Likewise, even though there was certainly some evidence of exuberance in the stock market around the very start of the 20th century – when stocks rose 163 per cent between August 1896 and September 1906 [7] – this hardly compares to the NASDAQ’s meteoric ascent in the late 1990s, or to the six-fold increase in the US market during the roaring 1920s. The market finally came decisively unstuck when it emerged that the chairman of a leading financial institution of the day had been using the firm’s assets in an attempt to manipulate the copper market.

S...

Table of contents

- Cover

- Publishing details

- Acknowledgements

- About the Author

- Introduction

- Chapter 1: A Lost Era in Equities

- Chapter 2: Will Deleveraging Drag us Down?

- Chapter 3: Gold’s Glittering Path

- Chapter 4: Beyond Hype: a Balanced Look at Emerging Markets

- Chapter 5: Dread, Denial and Default

- Chapter 6: The Future of the Euro

- Chapter 7: Fear and Loathing on Wall Street

- Chapter 8: When Rules and Regulators Fail

- Chapter 9: The Moral Hazard of Money

- Chapter 10: Central Banks: Leave, Improve or Abolish?

- Conclusion

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Fear and Greed by Nicolas Sarkis in PDF and/or ePUB format, as well as other popular books in Business & Stocks. We have over 1.5 million books available in our catalogue for you to explore.