eBook - ePub

Essentials of Physician Practice Management

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Essentials of Physician Practice Management

About this book

Essentials of Physician Practice Management offers a practical reference for administrators and medical directors and provides a comprehensive text for those preparing for a career in medical administration, practice management, and health plan administration. Essentials of Physician Practice Management is filled with valuable insights into every aspect of medical practice management including operations, financial management, strategic planning, regulation and risk management, human resources, and community relations.

Tools to learn more effectively

Saving Books

Keyword Search

Annotating Text

Listen to it instead

Information

PART ONE

FINANCIAL MANAGEMENT

CHAPTER ONE

BUDGETING FOR PHYSICIAN PRACTICES

Objectives

This chapter will help the reader to

- Understand the purposes and advantages of budgeting.

- Describe the process of budgeting.

- Prepare a budget for a physician practice.

Each year physician practices go through the all-important exercise of planning for the coming year’s activity. As more fully discussed in Chapter Sixteen, this should be a joint activity between practice management and the physician-owners. The budget is the tool that group practice managers use to translate the practice’s goals and objectives for the year into dollars. The budget also serves as a vehicle to communicate financial targets to physician-owners and other stakeholders in the practice.

To the wise practice manager the budget is not just a financial plan. It is also a mechanism for monitoring and managing the activity of the practice on a periodic basis. Some practices compare actual results to the budget on a monthly basis. Others do it more or less frequently. The comparison of actual results to budgeted amounts enables practice management to

- Focus on where the practice is going and what it will take to get there.

- Determine where resources should be allocated.

- Assess the productivity of the practice.

- Foster accountability in department managers.

- Analyze the areas in which variances in volume have occurred.

- Identify rates paid by third-party payers that are either more or less than originally predicted.

- Identify costs of various inputs to the practice, such as labor and supplies, that are either more or less than originally predicted.

- Make the necessary changes on a timely basis to keep the practice healthy.

- Note opportunities for future expansion.

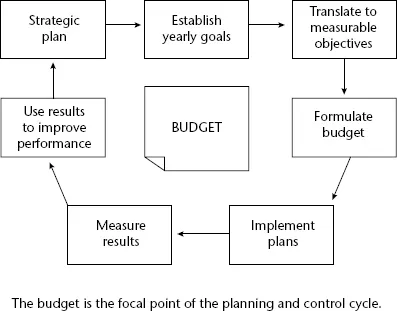

Practice managers can use this information to make timely changes to practice operations. Corrective action is particularly important in times like the present when reimbursement is low in comparison to the resources it takes to adequately deliver services and manage a practice. Thus the budget as a control mechanism takes on additional importance. Figure 1.1 illustrates the relationship between the budget and the planning and control cycle.

FIGURE 1.1. THE BUDGET IN RELATION TO THE PLANNING AND CONTROL CYCLE.

The budget is the focal point of the planning and control cycle.

Variety in Budgeting Methods

There is a great deal of variety in how physician practices budget. Some take budgeting very seriously and use it as a planning tool, whereas others don’t prepare budgets at all. The wise group practice manager will develop a budget in sufficient detail to provide himself, the physician-owners, and other practice stakeholders with information that will be useful in guiding the practice and monitoring results. At the same time, the budget should not be so detailed that it takes an inordinate amount of time to accumulate and analyze the information. The size and complexity of the practice as well as the level of its administrative resources will play a role in determining the appropriate level at which to budget. However, it is better to budget with less detail than not to budget at all. Practice budgets vary in

- Level of stakeholder participation

- Level of detail

- Budgeting method used—incremental or zero-based

Level of Participation

Participation in the budgeting process varies from practice to practice. In some practices budgeting is left to the practice administrator, with little input from the physicians other than how much they intend to work in the coming year. This is unwise. Input from physicians, department heads, and other clinical staff can provide the practice manager with fresh ideas. In addition to making the budget more reliable, such input increases buy-in to the financial plan as well as awareness of what it costs to run a practice. At the same time, where participation is advisable and will most likely produce the best result, the practice manager must also consider the following:

- The budgeting process will take longer and consume resources that the practice might otherwise devote to patient care.

- Estimates of patient volume and of costs of the inputs to deliver patient care may be unrealistic.

- People who take time to provide their input to the budgeting process may be disappointed if their input is overridden by the practice manager.

Level of Detail

As more fully discussed later in this chapter, revenue budgets are constructed using estimates of patient volume at varying levels of reimbursement. Expense budgets are constructed using estimates of labor, supplies, and overhead. How far the practice manager disaggregates those estimates depends on the precision desired. For example, a more precise budget can be created by budgeting patient visits by intensity as well as by payer and contract type.

Physicians provide services in several settings. Office visits, surgical procedures, and other types of diagnostic and therapeutic services can be provided in physicians’ offices, hospitals, skilled nursing facilities, hospices, outpatient dialysis facilities, clinical laboratories, and ambulatory surgical centers. Physician practices frequently use relative value units (RVUs) to express intensity of service. The resource-based relative value scale (RBRVS) was enacted into law as part of the Omnibus Budget Reconciliation Act of 1989. The fee schedule, phased in over a four-year period (1992 to 1996), reimburses physicians for their services based on three distinct components:

- Work (physician effort and skill)

- Practice expenses (rent, supplies, staff effort)

- Malpractice expenses

The objective of the RBRVS is to compensate physicians based on both the work involved and the resources used in patient care. There are codes for 7,000 distinct services, ranging from basic services such as injections to complex bundles of procedures associated with particular surgeries. These more complex bundles include the surgery and preoperative and postoperative visits. Each HCPCS (Healthcare Common Procedure Coding System) procedure code has a relative value (the basic value is 1). These values are adjusted for geographic factors to produce the reimbursement level. Although this payment system was created for services to Medicare patients, the methodology can be used to predict the level of effort involved in serving other patients as well.

In 2001, the American Medical Association performed a survey to determine whether non-Medicare payers used the RBRVS relative rankings in their payment systems. Respondents to the survey included Blue Cross Blue Shield organizations, health maintenance organizations, point-of-service plans, preferred provider organizations, Medicaid agencies, and workers’ compensation plans. Of the 226 entities surveyed, 74 percent used the RBRVS in at least one of their product lines.1 The American Academy of Pediatrics has adapted the RBRVS relative rankings for services to pediatric populations.2

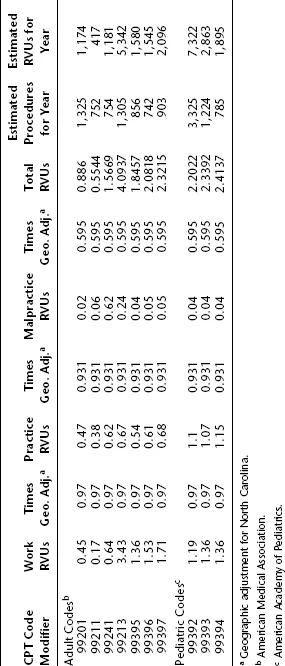

If a practice manager is budgeting using a high level of detail, she might compile a list of the Current Procedural Terminology (CPT) codes most frequently used by the practice and estimate the number of times each would occur during the year. Table 1.1 presents an example of such a list, in which estimated RVUs for each of the three reimbursement components are multiplied by the geographic adjustment to estimate the total RVUs. However, if that level of detail is not desired, the practice manager can determine the procedures most commonly performed and categorize them according to the average time it takes to perform each one, as illustrated in Table 1.2, using the following scale:

TABLE 1.1. RBRVS ILLUSTRATION.

TABLE 1.2. CPT CODES CATEGORIZED BY LEVEL OF EFFORT.

| CPT Code | Work Level RVU (1,2,3) | Minutes |

| 99201 | 1 | 15 |

| 99211 | 1 | 15 |

| 99241 | 1 | 15 |

| 99213 | 3 | 45 |

| 99395 | 1 | 15 |

| 99396 | 2 | 30 |

| 99397 | 2 | 30 |

| 99392 | 2 | 30 |

| 99393 | 2 | 30 |

| 99394 | 2 | 30 |

| Work Level RVUs | Time | |

| 0–2 | = | 15 minutes |

| 2.01–3.5 | = | 30 minutes |

| >3.5 | = | 45 minutes |

Level of detail also comes into play when estimating the reimbursement to be received for a particular service. Depending on size and geographic location, a practice may have dozens of reimbursement levels for the same service. If a high level of precision is desired, the group practice manager will estimate by payer and by contract. Depending on the number of payers and of contracts per payer, this level of detail may be overwhelming. Practice managers may wish to use only a few p...

Table of contents

- Cover

- Contents

- Title

- Copyright

- List of Figures and Tables

- Acknowledgments

- Preface

- Part One: Financial Management

- Part Two: Regulatory Environment and Risk Management

- Part Three: Human Resource Management

- Part Four: Strategic Considerations: Planning, Marketing, and Management

- Part Five: Information Management

- The Editors

- The Contributors

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Essentials of Physician Practice Management by Blair A. Keagy, Marci S. Thomas, Blair A. Keagy,Marci S. Thomas in PDF and/or ePUB format, as well as other popular books in Medicine & Public Health, Administration & Care. We have over one million books available in our catalogue for you to explore.