![]()

CHAPTER 1

The Only Constant

It is not necessary to change. Survival is not mandatory.

—W. Edwards Deming

My first car was a used ’49 Chevy. We could pull it into the garage and change the plugs, set the timing, clean the carburetor and be on our way. Back then, it was relatively easy to understand engines and how to keep them running smoothly. Today, if someone asked me to explain the first thing about what’s happening under the hood of my car, I wouldn’t have a clue.

There’s a parallel between that Chevy and my first excursion into the world of investing. When I became a stockbroker in the late sixties, my choices were pretty simple: common stocks, preferreds, a few warrants, limited over-the-counter options, U.S. government treasuries, municipals and corporate bonds, and cash. While there were mutual funds, they were extremely limited and many brokerage firms discouraged brokers from selling them to customers.

The financial markets have moved from simple to complex at a rate of change that is impossible to fully grasp. This accelerating complexity has been multiplied by the Internet explosion, global expansion, and myriad other factors, leaving individual traders and investors bewildered and grasping at narrow fragments of the larger picture, or subscribing to the beliefs of supposed experts who promise clarity and shelter from the information maelstrom. It’s no wonder that the current financial atmosphere is one of continual change and uncertainty.

In his landmark book, The Structure of Scientific Revolutions (Chicago: University of Chicago Press, 1962), Thomas S. Kuhn examines the way change realigns the “received beliefs” of any given community; because a community’s participants define themselves according to the ideas they share, they often take great pains to defend those ideas. In fact, it’s not uncommon for this defensive posture to result in the active suppression of new theories that undermine reigning assumptions. Therefore research, Kuhn writes, is not about discovering new truths, but rather “a strenuous and devoted attempt” to force new data into accepted conceptual boxes.

In short, change threatens the very terms with which we identify who we are (and how we invest our money).

But history has proved that in all things stasis never lasts—eventually an anomaly arises that is so compelling it cannot be ignored or dismissed as a “radical theory.” Inevitably, the anomaly unseats the norm, resulting in a paradigm shift in shared assumptions. These shifts, as Kuhn describes them, are nothing short of revolutionary.

Paradigm shifts force a community to reconstruct its foundation of belief. Facts are reevaluated. Data are examined through new lenses and, despite vehement resistance by those who refuse to let go of outdated ideas, the old paradigm is overthrown. A new community is established, and the “radical theories” are accepted as the new normative establishment.

The cycle of change begins again.

How important is change? Think about the many powerful institutions and intrepid individuals that once lead the fray and who are now long gone; those who recognize change early can take advantage of change, those who can’t overturn their past beliefs get left behind. That pattern repeats itself endlessly in all human endeavors.

In

The Tipping Point: How Little Things Can Make a Big Difference (Boston: Little, Brown, 2000), Malcolm Gladwell defined the way people react to change by classifying them on a spectrum:

innovators : early adopters : early majority : late majority : laggards

We are going to show you how to use market-generated information to identify and adapt to change before your competitors—once the majority recognizes that change is occurring, all assymetric opportunity is lost. This book challenges you to be an innovator, to overturn (change) many of the assumptions that now guide your perception of economic and market conditions. You may be faced with information that runs counter to the prevailing beliefs of those whom you have trusted for guidance. Daniel Kahneman said it best: “Resistance is the initial fate of all new paradigms. Often this resistance is strongest among the institutions responsible for teaching and upholding the status quo.”

To begin, we address change in the financial markets from the broadest perspective, which is from the point of view of investors who operate in the longest timeframe. But it is important to note that this same process occurs for traders/investors of all timeframes—those who capitalize on five-minute price swings, day traders who make several daily decisions, short-term traders who hold positions for several days, intermediate-term traders who track bracket extremes, as well traders who hold their positions for several months or even years.

What we are addressing, across all timeframes, is how change occurs.

We believe that the financial markets—and therefore all participants, businesses, and industries dependent on the markets—are at the vortex of a truly significant change. Over the coming years, investors, traders, portfolio managers, financial advisors, pension consultants, and even academics will all have to pick their spot on the spectrum of change ... and win or lose because of it.

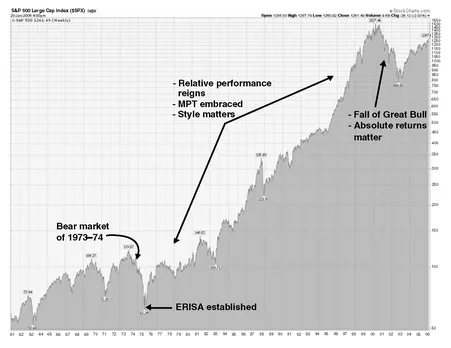

There is no single key driver behind the change we’re experiencing. Rather, a series of developments—some connected and some not—over the past 30 years have created the evolution that is now underway. The balance of this chapter introduces these events and their implications on the financial markets and those who operate within them (traders, portfolio managers, advisors, etc.). To help you visualize the following discussion, Figure 1.1 illustrates several key developments of recent market history in the context of the U.S. equity market.

FIGURE 1.1 Events shaping market and investor behavior: S&P 500, 1965 to 2004.

Source: Chart courtesy of StockCharts.com.

THE CREATION OF ERISA

The first serious change in the modern financial services business took place in the early seventies, partly as a result of the U.S. bear market that culminated in October 1974. Leading to the trend’s nadir, equity valuation had decreased by approximately 40 percent (see Figure 1.1), the bond market had dropped an equivalent amount, and there was an estimated 35 percent decline in purchasing power. It should come as no surprise that innovation flourished under these extreme conditions; change demands the surrender of security, and in 1974 the very notion of security was cast in doubt.

Not surprisingly, new government regulations designed to protect employees’ hard-earned retirement funds followed closely on the heels of this cataclysmic plunge. Enter ERISA (Employee Retirement Income Security Act), enacted in 1974 and designed to protect employee pensions. While performance measurement had got under way in the 1960s, ERISA increased focus on return relative to risk, which jumpstarted a new era of corporate accountability.

While this new accountability was clearly needed, ERISA was concerned more with the process by which pension-investment decisions were made, rather than with the investments themselves, which had the effect of ushering in an industry that focused on asset allocation, manager selection, and performance evaluation. Pension funds began to exercise more prudence when selecting money managers, hiring consultants to assist them in meeting their fiduciary responsibilities. The pension-consulting industry-began to boom.

On the surface, ERISA had many positives—it improved diversification and disclosure and promoted standards that enabled investors to better understand and compare investment performance. However, lurking below the surface was a negative that would take years to fully reveal itself: many of the processes implemented as a result of ERISA served to stifle innovation and creativity in the investment management business.

THE RISE AND FALL OF RELATIVE PERFORMANCE

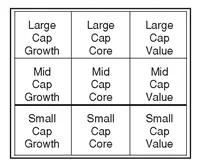

The push toward improved diversification and process transparency resulted in managers developing extremely specific approaches to investing (see Figure 1.2). In turn, consultants needed improved ways to judge how individual managers were performing relative to the market, and relative to each other. Consultants initially used broad markets indices to gauge performance. However, as more and more specialty managers began to appear, benchmarks began to evolve and, as with all change, these evolutions became increasingly complex. Specialized market indexes were employed to gauge performance. Categories were formed so that managers could be compared against their peers. Consultants pigeonholed asset managers into distinct styles so they could more easily monitor their activity and fire them (or not hire them) if they didn’t fit neatly into preconceived categories. Over time, this forced many money managers to become highly specialized, focusing on individual styles like growth or value, which in turn were further broken down into large-cap, mid-cap, and small-cap strategies, as well as a host of other variations.

FIGURE 1.2 Typical U.S. equity styles.

Throughout the Great Bull market that began in 1982 and ran for almost 20 years, managers that attempted to be creative and innovative sometimes found that their ability to raise assets diminished—even if they had stellar track records—because they no longer fit within a convenient category.

The perceived institutional need to compare performance to peers and market benchmarks resulted in most of the focus being on relative performance , rather than absolute performance. (In short, “relative return” has to do with how an asset class performs relative to a benchmark, such as the S&P 500. “Absolute return” speaks to the absolute gain or loss an asset or portfolio posts over a certain period.) The relativistic approach to evaluating performance proved to be a boon for asset managers, in that they could now focus on constructing portfolios that had only to equal or perform marginally better than market benchmarks—regardless of whether performance was positive or negative.

Relativism provided a windfall for asset managers, in that it often masked poor absolute performance; an asset manager with a negative return could still win the Boeing pension fund simply by outperforming peers and benchmarks! As long as performance was measured on a relative basis, the money management industry continued to raise significant assets (upon which fees could be charged). While this wasn’t so detrimental during the rising markets of the time, the relative-performance crutch did little to prepare managers to compete in the less certain markets that followed the end of the great bull market in 2000.

The tide would soon turn: Once it was clear that the market was no longer going up, clients would begin to demand that their managers do more than simply match the market.

THE FALL OF THE GREAT BULL

Coupled with an extended bull market, the enactment of ERISA had the effect of codifying modern portfolio theory (MPT) in the eyes of the majority of investors and investment managers. (In a nutshell, MPT emphasizes that risk is an inherent part of higher reward, and that investors can construct portfolios in order to optimize risk for expected returns.) For fiduciaries, the concept of controlled risk through diverse asset allocation is certainly appealing. When markets are “behaving” (as they were for nearly two bullish decades) the return, risk, and correlation assumptions used to generate asset allocation analyses tend to sync relatively well with market activity; a trend is predictable as long as it continues. In this environment, modern portfolio theory became the comfortable thread that held the financial markets’ complex patchwork quilt together. Within this model, asset managers that performed well on a relative basis within a single, easily identifiable style could consistently raise assets. Once they stepped away from their advertised style, however, their opportunities became limited. An unfortunate result of this phenomenon was that this narrow, restrictive environment tended to limit the growth of asset managers’ skill base. It’s difficult to understand how talented, competitive individuals allowed themselves to remain locked into one specific management style for so long, especially when that style had clearly fallen out of favor. I saw managers literally go out of business rather than change their investment approach.

As the great bull began to show signs of strain and the equity markets began to behave with far less certainty (no longer trending up). It became apparent that the relativistic, MPT-driven business model embraced by traditional asset managers—one in which money was managed on a relative basis, track records were marketed based on relative performance, and performance was measured in relative terms—was plagued by significant weaknesses.

Alexander M. Ineichen of Union Bank of Switzerland (UBS) estimated that total global equity peaked at a little over $31 trillion at the top of the bull market, falling to approximately $18 trillion at the 2002 low—a decline of approximately 42 percent. As during the 1974 period, the investment community reluctantly began to embr...