Written in a fun and accessible manner, The Fund Spy offers Kinnel's unique insight as a 14-year Morningstar fund analyst. He speaks plainly about the conflicts that can go against investors' interests, explaining how to avoid traps and push out the slick sales pitches facing today's investors. He also offers several "10 lists," which provide quick answers to investors' most common questions (e.g., the Top 10 Funds to Recommend to Relatives, the 10 Best Contrarian Managers, the 10 Most Overrated Managers).

eBook - ePub

Fund Spy

Morningstar's Inside Secrets to Selecting Mutual Funds that Outperform

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Author Russel Kinnel walks readers through the handful of key factors they need to pick winning funds. Armed with the quantitative data and qualitative research, they will gain the confidence to pick great funds for the long-term. This book will be accompanied by a web-based tool created by Morningstar, which will enable readers to evaluate their own funds using Kinnel's criteria.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

1

The Remarkable Gap Between Winners and Losers

THIS BOOK IS ALL ABOUT picking winning funds, so let’s take a look at what you’ll win if you select good funds.

Too often, people assume that one fund is as good as the next. Or they put in the effort to pick their stock funds but buy their bond funds from whichever fund company is most convenient. But that’s leaving a lot of money on the table.

As the immortal Spinal Tap lead singer David St. Hubbins said, “It’s such a fine line between stupid, and clever.” Put a little time into your fund selection, and you’ll be on the right side of the St. Hubbins line.

It’s amazing to me how people will spend way more time researching fun expenditures, like cars and plasma TVs, than they will on developing an investment plan and selecting their investments. Sure, it isn’t as fun, but it’s your retirement, your house, and your kids’ college education!

Let’s look at why it’s worth a little effort. It’s not too hard to pick funds that will do a little better than average, and it takes only a little more work to upgrade from there so that you’ve meaningfully improved your chances of returns that are well above average while reducing your chances of lousy performance. Of course, there’s no foolproof method of predicting the top-performing fund over the next 10 years, but there are dependable methods to select funds that should earn strong returns while limiting cellar-dwellers.

The Forest for the Trees

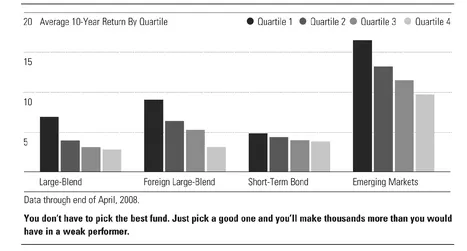

Sometimes short-term returns, such as those for a six-month period, can be all bunched together. From that perspective, funds in a particular category might all look alike. If you step back and look at the effects of long-term compounding, however, the differences get dramatic. You can see the gaps in Figure 1.1, where even among low-returning bond funds the gap is quite wide.

Figure 1.1 The Enormous Gap Between Winning and Losing Funds

Source: Morningstar

Let’s consider the returns of large-blend funds returns over the past 10 years. The large-blend category, which is home to a passel of S&P 500 Index funds, might seem like a bunch of bland benchmark-huggers. But consider the differences in average 10-year annualized returns for each quartile through April 2008: Funds in the top quartile gained 7.02 percent per year over the 10-year period; funds in the second quartile rose 4.06 percent per year; the third, 3.23 percent; and the fourth, 2.9 percent. That’s a huge gap from the top quartile to the second and down to the fourth. In honor of St. Hubbins, let’s call the gap between the top and bottom quartiles the stupid penalty. In the case of large-blend funds, it’s more than 400 basis points. Put in dollar terms, $100,000 invested 10 years ago in the typical top-quartile large-blend fund grew to $197,000 today, versus $149,000 for the second quartile and $133,000 for the worst—making a stupid penalty of $64,000!

Top 10 Best Things About Mutual Funds

1. Diversification is better than you get on your own.

2. There is greater transparency than any other managed account.

3. They bring great management to individual investors.

4. Low-cost funds are the best deal in investing.

5. They enable you to invest outside your area of expertise.

6. They are easy to compare.

7. Audited portfolios make theft nearly impossible.

8. You can get in or out every day at net asset value.

9. Some have track records that are decades long.

10. You can invest automatically without paying commissions.

The gap remains dramatic in other categories. For the foreign-large-blend group, the top quartile returned 9.16 percent, compared with 6.49 percent, 5.38 percent, and 3.24 percent for the three other quartiles, respectively. For the intermediate-bond fund category, returns were 6.02 percent, 5.25 percent, 4.85 percent, and 4.07 percent. That’s a big gap for high-quality bond funds. Then, I checked two categories at the extreme ends of the risk spectrum and found not much changed in the gaps. For short-term bond funds, the breakdown was 4.93 percent, 4.47 percent, 4.10 percent, and 3.91 percent. It’s amazing to think that you can do 100 basis points better per year in a category where yields and returns are so tightly bunched. For the diversified-emerging-markets-stock category, returns were 16.62 percent, 13.31 percent, 11.58 percent, and 9.84 percent.

One of the most striking aspects of the study is that it even works across categories. Except for the emerging-markets-stock fund category, you could take the top quartile of one of the four other categories and beat the bottom quartile of other groups. For example, you’d have been better off in a top-quartile short-term-bond fund than a bottom-quartile or even second-best-quartile large-blend fund. The top quartile of intermediate-bond funds beat the bottom-half returns for the foreign-large-blend group.

Improve Your Chances of Success

In short, you’ll make it much easier to beat your investment goals if you can select outperformers. This book will show you how to do that. No, you won’t bat 1.000, but you should be able to be on the right side of the St. Hubbins line most of the time.

Don’t settle for high-cost, poorly run funds simply because they fell into your portfolio or someone is touting them. Take the time to research and buy funds that will work for the long haul. Three months or even a year from now, you may not see a difference, but you will see a dramatic difference in 10 and 20 years, when the power of compounding has grown your portfolio.

The returns we just reviewed include only funds that were good enough to survive in the first place. It’s tough to take into account those funds that were around for only part of the time period. Suffice it to say that if we could factor those in, the gap would be even greater. The crummiest funds are the ones generally killed off, so the bottom-quartile figures would be even worse if extinct funds could be included.

Welcome to Lake Wobegon

Lest you think that finding better funds is a daunting task, consider this: The average fund investor actually does better than the average fund, despite making key errors. Yes, that sounds like Lake Wobegon where everyone is above average, but it’s just a matter of two different averages. It does seem hard to believe, considering that many fund investors are lousy timers. They buy hot sectors after they have gone up a lot, and they panic and sell poor-performing sectors just before they rally. Yet they actually compensate for their bad timing by picking above-average funds.

In 2006, I used asset-weighting to find out how the typical investor did. That means I weighted fund returns based on asset size at the end of each month. When you do that, you see that investors typically fare worse than the actual stated returns for a fund because of lousy timing of purchases and sales. In fact, I first wrote about this in a Morningstar FundInvestor commentary titled “Mind the Gap” published in 2005. Financial pundits ate this up with a spoon because it made fund companies and fund investors look bad, and justifiably so.

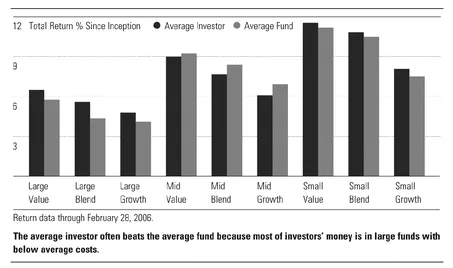

But in a 2006 study, I took the extra step of asset-weighting those investor returns so that I could see how the average investor did overall. It turns out that collectively, fund investors actually did better than the average category performance because they chose better-than-average funds (see Figure 1.2). Interestingly, none of the pundits picked up this follow-up story. In fact, the earlier study is still cited far more than the latter because financial writers like the elitist sound of it. Fund companies and fund investors are idiots—end of story. The follow-up study shows that the average investor isn’t quite that much of a dolt, but that won’t sell newspapers or really high-priced hedge funds.

Figure 1.2 The Average Investor versus the Average Fund

Why does the average investor beat the average fund? The main reason is costs. Big funds generally have lower costs because the funds pass along some economies of scale to fundholders. (Don’t worry—they keep plenty for themselves.) In fact, the difference between the average fund investor’s performance and the average fund’s performance is almost exactly the same as the difference between the asset-weighted expense ratio and the average expense ratio.

Fund investors and their advisors find their way to bigger, lower-cost funds for a wide range of reasons. Some seek out lower costs; others like to consolidate their accounts, and the big fund companies (which tend to have cheaper funds) make that easy. Others go through brokerages, which favor certain big fund companies, and some just buy them because they’re in their 401(k). In addition, there’s a self-reinforcing aspect to this, as lower-cost funds tend to outperform, thereby attracting assets, and that, in turn, lowers the expense ratio further.

FAQs

Q. When you say better than average, what group are you averaging?

A. I’m referring to the average return of a fund category. Categories are our way of classifying funds. Comparing returns within a category enables you to assess a fund’s performance. The categories are also helpful in building a diversified portfolio. We base the categories on three years’ worth of portfolio data. For example, we group domestic stock funds by our Style Box with categories such as small value and mid-growth.

Q. What is the Morningstar Style Box™?

A. The Style Box is a nine-box grid we use to analyze funds; the categories are based on them. We’ve found that funds with similar market cap, value, and growth characteristics tend to behave in similar fashion and invest in similar holdings. It’s divided by market cap vertically (small, mid, and large) and value/growth horizontally (value, blend, and growth). We use five value characteristics and five growth characteristics to determine where a fund plots on the y axis.

Conclusion

So, if the typical investor can easily find his way to an above-average fund, imagine what you can do when you intelligently target the key factors that drive fund performance. Only a few investors are using all of the tools I’m going to share with you in this book. Some are brand new, and others are tried and true.

Armed with the right strategy, you can do better than the average fund and the average investor. With better information, you can avoid the timing mistakes that so many investors make, and you’ll be well on your way to reaching your goals.

2

Does Your Manager Eat His Own Cooking?

IF I ASKED you if the managers of your mutual funds invested in their funds, your first reaction might be, “Of course they do.” It turns out that most don’t.

Some managers really do mean it when they say they consider fundholders partners, while others don’t. Until recently, everyone could talk big, but then the SEC started requiring managers to actually disclose their investments.

The good news is that hundreds of managers have more than $1 million of their own money in the funds. The bad news is that thousands don’t have a dime in their funds. Apparently, those fund ads and slick brokers’ pitches didn’t even convince the folks running the fund to invest.

Let’s take a look at the gory deta...

Table of contents

- Title Page

- Copyright Page

- Dedication

- Foreword

- Preface

- Acknowledgements

- Chapter 1 - The Remarkable Gap Between Winners and Losers

- Chapter 2 - Does Your Manager Eat His Own Cooking?

- Chapter 3 - New Trading Cost Estimates Shed Light on a Big Mystery

- Chapter 4 - The Power of Expense Ratios Is Greater Than You Think

- Chapter 5 - How to Use Total Returns Wisely

- Chapter 6 - Understanding Mutual Fund Strategies and Fundamental Risk

- Chapter 7 - How to Find Good Managers and Avoid the Dodgy Ones

- Chapter 8 - The Inside Scoop on No-Load Fund Companies

- Chapter 9 - The Inside Scoop on Broker-Sold Fund Companies

- Chapter 10 - Twenty Great Funds That Passed My Test

- Appendix A - The Best of Eleven Years of Fund Spies

- Appendix B - Vital Statistics on the 20 Funds That Passed Our Test

- Glossary

- About the Author

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Fund Spy by Russel Kinnel in PDF and/or ePUB format, as well as other popular books in Personal Development & Personal Finance. We have over 1.5 million books available in our catalogue for you to explore.