The funding of innovative projects that are fundamentally ambiguous often leads to situations where decision-making is difficult. However, decision-making can be improved by practices such as syndication and step-by-step funding. The dynamic of this industry requires us to consider the economic and institutional variables that make this system coherent in English-speaking countries, but conversely reduce it to a privileged niche by the leading authorities in Europe and France.

This book proposes two guiding ideas. The first idea presents innovation as a very uncertain process. This modifies the decision-making in the entrepreneurial ecosystem, with intervention upstream in regards to stronger foundations, evaluations and selection of projects. The second idea is that the actors hold onto partial knowledge in a context where their attention span is limited. These cognitive limitations need the formation of networks, and lead to mutual and complementary dependency relations.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

1 Venture Capital, Behavior and Performance of Stakeholders

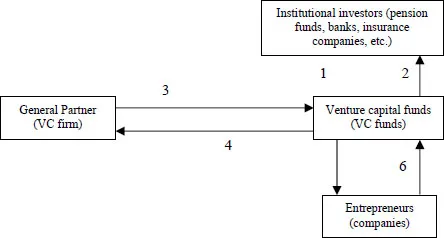

The venture capital industry is structured on the management of assets carried out by third parties. This chapter will focus on the logic guiding the actions of the various different stakeholders to make venture capital an effective mechanism for financing innovation. The social practices that take place are done within three-way relationships between the following players.

Figure 1.1.Simplified diagram of venture capital activity: (1) collection of funds; (2) distribution of returns obtained; (3) low level of contribution; (4) management fees and payments; (5) investments; (6) end of the investment relationships

(source: [RIN 11])

We have identified three main areas of investigation: interactions between financed firms and venture capital (selection, investments, strategies, exits), interactions between venture capital funds and institutional investors (collection of finances, distribution of returns), and finally the organization of venture capital firms and their relationships, including syndication. We adopt the point of view of the works of literature which considers the “General Partner” as a firm and the company as a start-up that receives funding. When we consider the financing chain for innovative start-ups, we may note two characteristics unique to France: first, the relative weakness of long-term funds, and second, the significant participation of the public sector [EKE 16]. For regulatory reasons (prudential ratios), investments by banks and insurance companies in long-term, high risk projects are necessarily limited. The influence of public intervention is given in Table 1.1.

Table 1.1.Distribution of private equity funds raised, by type of investor (in %), 2012–2015: (1) = Germany + Switzerland and Austria; (2) = United Kingdom + Ireland; (3) = Denmark, Finland, Norway, and Sweden; (4) = France + Belgium and Luxembourg

(source: [EKE 16, p. 5] from EVCA)

Germany (1)

United Kingdom (2)

Scandinavian countries (3)

France (4)

Public institutions

22.3

2.9

13.4

22.3

Family offices and individuals

18.8

6.5

6.9

19.1

Insurance companies

8.4

9.6

4.3

16.6

Funds of funds

15.5

18.6

22.1

14.7

Pension funds

21.5

36.3

27.4

11.0

Banks

6.1

2.2

5.6

7.2

Private companies

3.6

1.8

1.5

5.0

Sovereign wealth funds

0.7

15.4

10.5

2.7

Capital markets

0.2

1.6

1.5

0.8

Academic institutions, donations, and foundations

3.1

5.1

6.6

0.8

Total

100

100

100

100

Table 1.1 shows the funds raised by private equity. Despite the similarity of these statistics, venture capital must be considered as distinct from private equity, even if these two financing mechanisms are of a comparable nature (illiquid and medium- to long-term investments). The two do not take the same approach to the problem of fundraising. In particular, with regard to venture capital in Europe, the difficulty of finding the right options for departure explains why this industry consistently underperforms. This would explain why the funds raised on the European venture capital market do not reach the levels of those raised on the private equity market.

With regard to venture capital, a recent article states that:

“France is characterized... by the importance of venture capital financing through public funds, which represent more than a quarter of the amounts raised. This is partly due to the lack of pension funds and university foundations. In fact, the time scale of these investors, which spans a greater period than that of other institutional players (banks, generalist funds, etc.) and their greater capacity to take risks (compared to insurers, for example), makes them important players in other countries. France is also characterized by its smaller specialized funds. As an example, the largest French funds are about 10 times smaller than the largest American funds. This fragmentation poses a particular problem for the most important fundraising events, beyond the start-up phase, which are essential for supporting the growth of successful start-ups and keeping them within the territory” [FRA 17, p. 2].

It should be noted that the target company and the entrepreneur do not occupy the same position in these two configurations. In private equity- and particularly in buyouts – the company already exists, it is established, is often mature, and generally functions as part of the “old economy”. Investors acquire existing companies, improve their business model (the targets are very often underperforming business units) by transferring modern managerial tools and financial techniques to them to increase their value. Poorly managed companies become attractive targets that can be transformed into profitable companies [MEY 06].

By contrast, in venture capital, the company does not exist at the beginning of the process. It is only a concept of a product, process, or service, which will be developed in the “new economy”. The trade-off between seizing on an entrepreneurial opportunity and being employed in a large company, given the entrepreneur’s aversion to risks, often leads to the conclusion that entrepreneurial choice is not very profitable because of the specific risks faced by the start-up that is to be created. The risk of exposure to corporate volatility is much lower in later stages (development or transmission). On the other hand, managers of venture capital and development capital funds are exposed to the same difficulty of diversifying their portfolios.

Moreover, the financial flows do not have the same purpose. Venture capital represents an institutional and organizational innovation that makes it possible to organize young innovative companies and professionalize their management, so that – in the case of the most efficient among them – they can make it into the technology stock market (going public). Following the logic of private equity, opportunities for profit can be found when the funds become owners of mature companies in which operators identify opportunities to create value, by optimizing their business portfolio and restructuring the scope of these companies. To this end, companies are often removed from the stock market, their shares become the property of one (or more) funds and, since they are no longer listed, they cannot be bought on the stock exchange by the public: they “go private”, hence the term private equity. A new model known as the “not publicly traded” model has emerged and developed rapidly in recent years, which contradicts the underlying logic of capitalism.

We will focus on three aspects. First, we will specify the framework for analyzing the relationships between venture capitalists and entrepreneurs. Then, we will analyze the real behavior of these two categories of actors. Finally, we will highlight the contributions made by venture capitalists to the performance of innovative companies.

1.1. The analytical framework

Academic literature essentially uses two approaches: the agency theory and the resource dependency approach.

1.1.1. The contractual model and agency problems

Over the lifespan of the company, a financing gap is created when potentially profitable investment opportunities cannot be taken advantage of due to a lack of internal financing. Additional external capital might then be provided by shareholders, banks, venture capitalists, companies, etc. In the first stage of development, when the company does not yet exist and its business model is not defined, funds may be provided by the entrepreneurs themselves, their families, and/or their friends. In addition to this, they may receive public support (competitions, honorary loans) or support provided by incubators (see Box 1.1) or accelerators1 [EKE 16]. The authors of the cited work distinguish the incubation phase from the seed phase (with funds usually provided by business angels, but also from public authorities or specialized funds) and the start-up phase, in which venture capitalists are very active2.

Box 1.1.The EuraTechnologies incubator (source: [NUN 17, p. 18])

“EuraTechnologies [is] an ecosystem where major digital firms and start-ups coexist... The path to creating a company is filled with challenges: deciphering the administrative process, convincing investors, building an address book of potential clients... To address these challenges, the incubator gives guidance and advising. It brings in lawyers, accountants, tax experts, managers... An army of experienced professionals, whose job it is to show newcomers the ropes before letting them take the wheel. Alongside the multitude of small businesses, digital giants such as IBM and Capgemini have created their own operations to ‘directly access project leaders’, says Massimo Magnifico [Chief Operating Officer of EuraTechnologies]. The presence of large laboratories, such as those of the Institut national de la recherche consacré au numérique (Inria) or the Commissariat à l'énergie atomique (CEA), continue to contribute to the richness of the site... The owners of a technology talk to companies who will ‘potentally [find it] a practical application...’”

The literature has often focused on the opacity of the information involving start-ups, particularly those that are technology-intensive [CAR 02]. In addition to the fact that coverage by the media only very rarely works in favor of young companies (except at international trade fairs), an innovative idea that can lead to a new product, process, or service is a strategic asset that the company must protect in order to receive future returns. In this sense, restricting information is a rational strategy for controlling intangible assets. Moreover, since these are innovation-based companies whose concept is based on R&D expenditures, their situation can be compared to what has become known as the “lemons market” and modeled by Akerlof in 1970. When projects involve long-term R&D investments, funders have more difficulty distinguishing between worthy projects and ones that are less so. The existence of such problems of information imbalances gives rise to three types of difficulties: adverse selection, moral hazards, and opportunism.

In its extreme version, adverse selection means that the market for R&D projects can disappear if the information imbalance is too severe. Indeed, if the cost of disclosing information to the market is very high, the quality of the signal surrounding the potential project is reduced [HAL 10]. The ambiguity is very strong in this case. According to Hall, this mechanism can be attenuated in two ways. First, if R&D expenditure is an observable signal that can be audited externally, and second, if the innovator is a serial entrepreneur whose reputation has been built through previously founded and successful start-ups.

Moral hazards occur when the entrepreneur – and venture capitalist do not share the same objective, with the former preferring to invest in activities that are rewarding for themselves, but not necessarily for the company. Regardless of this difference, the entrepreneur may have excessive confidence in a project and overestimate it, while the probability of success will only gradually become apparent over time. In this context, the entrepreneurs and the venture capitalists will disagree on the time commitment and the number of rounds of funding required. Venture capitalists face the dilemma of either having to wait too long to cancel a project or having to cancel it too quickly. However, it is possible to accelerate or slow down the project’s financing rate, depending on the progress that has been made and the expectations formed at each stage. There is also nothing from preventing the venture capitalists from including a termination rule in the contract (based on certain criteria), thus eliminating the possibility for opportunistic behavior by a contractor seeking to extend the duration ...

Table of contents

Cover

Table of Contents

Acknowledgments

Introduction

1 Venture Capital, Behavior and Performance of Stakeholders

2 The Sectoral Dynamics of Venture Capital

3 The Three Structures for Interpreting Venture Capital: The Market, Industry and Institutions

Conclusion

References

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Venture Capital and the Financing of Innovation by Bernard Guilhon,Sandra Montchaud in PDF and/or ePUB format, as well as other popular books in Business & Corporate Finance. We have over 1.5 million books available in our catalogue for you to explore.