This volume focuses on the aftermath of the euro crisis and whether the reforms have brought about lasting changes to the economic and political structures of the crisis countries or if the changes were short-term and easily abandoned post-bailout and post-recovery.

Starting with an analysis of the state of euro area governance at the onset of the crisis and the ensuing reforms, the book considers structural conditions as well as those specific to the domestic political economy of most of the countries affected by the crisis, including Greece, Ireland, Portugal, Spain, and Italy. It presents up-to-date and incisive analysis of the aftermath of the crisis and suggests how we can situate it within our understanding of different national growth models in Europe.

This book will be of key interest to scholars, students and practitioners interested in the Euro Crisis, Economic and Monetary Union, European Union and European politics and more broadly to Comparative Politics, Political Economy, International Relations, Economics, Finance, Business and Industry.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Michele Chang, Federico Steinberg and Francisco Torres

Introduction

2019 marks the 10th anniversary of the revelation of the Greek debt crisis that snowballed into the euro crisis and threatened the single currency’s very existence. In the course of the euro crisis, a number of euro area countries lost access to market financing and required official assistance: Greece (2010, 2012 and 2015), Ireland (2010), Portugal (2011), Spain (2012) and Cyprus (2013). And while Italy did not receive a bailout, it did face considerable market speculation alongside the other economies in the euro area periphery. Together, those countries were dubbed the GIPSI countries (the crisis in Cyprus came later and no moniker emerged to include it). The speculation against these countries and the existential threat that further spillover posed to the euro area prompted a host of reforms that were enacted over the last decade to improve economic convergence and the resilience of the euro area. Moreover, countries that received bailouts underwent conditionality programs that included major structural reforms.

This volume focuses on the aftermath of the euro crisis and asks whether the reforms have brought about lasting changes to the economic and political structures of the crisis countries or if the changes were short-term and easily abandoned post-bailout and post-recovery. Starting with an analysis of how the crisis led to further constraints on euro area member states, the volume then focuses on how this changed environment, particularly the conditionality programs, disrupted the economic growth models of the GIPSI countries. The case studies analyze in which cases and in which sectors the euro area reforms and the bailout programs were able to promote convergence and alter the domestic political economies of the economies in the euro area periphery. This volume presents an up- to-date analysis of the aftermath of the crisis, how it contributed to lasting change and how various elements of national growth models have either persisted or been altered.

The central argument of the book is that while the crisis had imposed policy constraints on the euro area countries and on the program countries in particular, the national growth models nevertheless persist. Despite the efforts to strengthen euro area governance and impose unprecedented levels of reform on the program countries, it took years for a consensus to emerge on the causes of the crisis (Baldwin and Giavazzi 2015). Even the institutions of the troika found themselves in conflict on how to address the underlying weaknesses of the euro area and the domestic political economy of the crisis countries (see chapter by Lütz et al. in this volume). Nevertheless, substantial convergence has occurred thanks to the euro area reforms made during the crisis and the program that the adjustment countries underwent as a condition of their bailout(s) from the European Financial Stability Facility (EFSF) and the European Stability Mechanism (ESM).

This introduction provides a brief overview of the volume. It presents the main research questions that all of the case studies deal with and the analytical framework that will be utilized to varying degrees by all of the case studies: the varieties of capitalism. The last section summarizes the volume’s case studies, both at the level of the euro area and the country studies.

Analytical framework

The issues confronted in this volume contrast with existing work on the sovereign debt crisis that have considered a wider variety of theories explaining the causes of the crisis itself and the troika programs (Caporaso and Rhodes 2016); or have taken a more sector-specific approach (Johnston 2016; Dølvik and Martin 2017); or works looking at the crisis from a more macro perspective rather than country-level (Caselli, Centeno and Tavares 2016). The theoretically informed chapters draw on the insights from the varieties of capitalism (VOC) literature, specifically in regards to the impact of countries’ respective growth models in leading up to the crisis and its response. They explore the politics in Europe and EU member states to look comprehensively at the European and domestic political consequences of the crisis since countries have exited their respective bailout programs, updating previous work on the causes of the immediate repercussions of the crisis to consider their longer-term impact. Enough time has passed to consider how the reforms imposed by the euro area and the troika have fared during more “normal” times and affected the domestic political economy of the program countries.

The VOC literature is a well-established comparative political economy theory that considers institutional variations across states. In contrast to expectations that globalization would lead to similar policies across countries striving to gain a competitive advantage, VOC points out enduring differences in relationships between government and economic actors. When institutional change does occur, such changes are conditioned by a country’s VOC and “new practices are developed to cope with the problems generated by past practice and integrated into a network of interacting institutions, some of which remain stable as others change” (Hall 2001, p. 76). In other words, “actors seek institutional and functional equivalents to pre-existing forms of coordination” (Hancké, Rhodes and Thatcher 2007, p. 11).

The three primary models in VOC are the liberal market economy (LME), the coordinated market economy (CME) and the mixed market economy (MME); their characteristics are briefly described in Table 1.1. Within LMEs, an arm’s-length relationship exists between the state and economic actors operating within a competitive environment. The UK and the US are often presented as the typical LME countries, and Ireland also fits this description. Within CMEs exist more extensive relationships between governments and economic actors, contributing to a more collaborative economic environment. Some of the main differences concern wage-bargaining systems that are coordinated in CMEs but not in LMEs, and the types of skills developed by workers that are more general in LMEs and asset-specific in CMEs (Hall and Soskice 2001). Germany, Belgium, Austria and the Netherlands are typical CMEs. The third model of the MME was introduced later to explain more completely economies like France, Spain, Portugal, Italy and Greece that share characteristics of both LMEs and CMEs. Their hybrid nature lacks the functional coherence and institutional complementarities that characterize LMEs and CMEs, leaving the state to compensate for the country’s economic deficiencies through the use of subsidies and protectionism (Molina and Rhodes 2007).

Table 1.1 Varieties of capitalism traits

Liberal market economy

Coordinated market economy

Mixed market economy

Examples

UK, Ireland

Germany, Belgium, Austria, Netherlands

France, Italy, Spain, Portugal, Greece

Growth model

Demand-led

Export-led

Demand-led

Asset specificity

Low

High

Low

Wage coordination

Low

High

Limited

Role of state

Limited

Coordinator

Compensator

VOC research explained not only different institutional and policy preferences but also how they interacted with the top-down pressure from the Europeanization process. In some instances, member states effectively would re-regulate in bottom-up initiatives rooted in VOC models (Menz 2005). The robustness of the respective VOC models not only relate to the aggregate welfare benefits that they provide, they also reinforce underlying political and social relationships (Hall and Thelen 2009).

These insights had important ramifications for EMU. The euro area consisted of very diverse economies at different levels of development and had different growth models. At the onset of EMU, Greece, Ireland, Portugal and Spain still benefited from EU cohesion funds in order for their economies to catch up to those in the euro area core in the north, which might have dampened reform pressures. Nevertheless, it was assumed that the single currency would encourage economic convergence. The fixed exchange rate system that had been in place since 1979 had contributed to converging interest rates and inflation rates as well as exchange rate stability. Capital controls had already been liberalized through the Single Market program, which presumably would intensify market discipline. The Maastricht Treaty’s convergence criteria demanded nominal convergence in long-term interest rates, inflation, debt and deficit levels, and exchange rate stability. Post-euro, adherence to the Stability and Growth Pact (SGP) would ensure continued fiscal probity. The Broad Economic Policy Guidelines and Lisbon Strategy would encourage structural reforms that would include more labor market flexibility and deregulation.

Nevertheless, monetary union did not lead to more convergence. Portugal, for example, was deemed a “big disappointment” after the first decade of EMU because of the “marked deterioration in … the Portuguese economy … with its potential growth rates now pointing to divergence rather than convergence” (Commission 2008, p. 115). EMU did not alter the VOC of the member states, and EMU may have pushed the different VOC to the point of incompatibility by removing their traditional forms of adjustment through exchange rate changes and national central banks targeting convergence in inflation and real exchange rates (Johnston and Regan 2016).

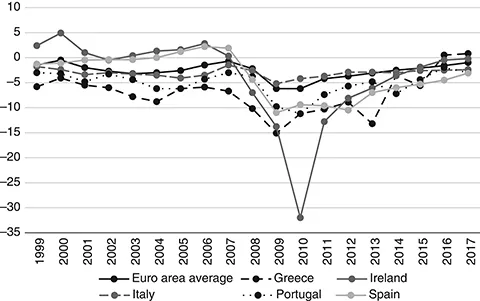

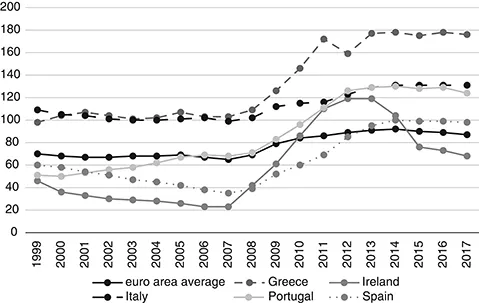

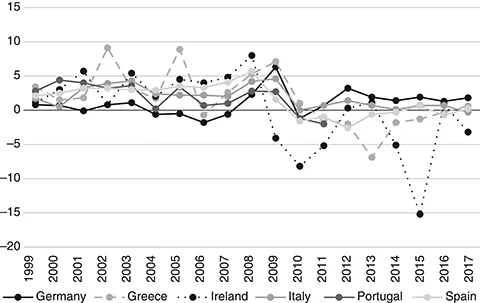

VOC indicated that MMEs would be more likely to engage in behavior that contributed to their vulnerability prior to the crisis despite the EU rules that were in place to promote convergence. Figure 1.1 shows that the deficit to GDP ratios of the MME countries under study exceeded the euro area average once the euro was adopted, though Spanish deficit figures quickly improved. This was on top of the already high debt levels carried by countries like Italy and Greece prior to the crisis, as seen in Figure 1.2. Indeed, Italy was well above the Maastricht Treaty convergence criterion’s debt limit of 60 percent of GDP but was able to enter in the first round of EMU thanks to the flexible application of these criteria.

Figure 1.1 Deficit to GDP levels of Greece, Ireland, Italy, Portugal and Spain and the euro area (17) average.

Source: Eurostat.

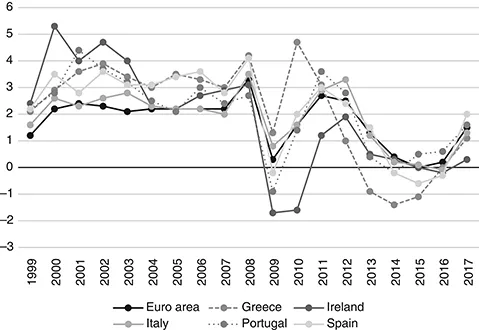

Figure 1.2 Debt to GDP ratio of Greece, Ireland, Italy, Portugal and Spain and the euro area average, 1999–2017.

Source: Eurostat.

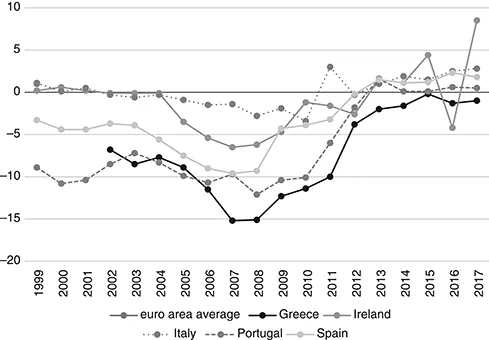

While CMEs were more likely to follow an export-led growth model that generated current account surpluses, LMEs and MMEs tended to generate current account deficits, as seen in Figure 1.3. While Portugal and Spain began EMU with current account deficits, Ireland’s small surplus turned into a deficit midway through the first decade of EMU and remained in deficit until well into the crisis.

Figure 1.3 Current account balance as a percentage of GDP.

Source: Eurostat.

While the run-up to monetary union and its first decade did lead to the liberalization of all euro area economies, MME governments concurrently had ramped up their social spending to compensate domestic actors who otherwise would have suffered as a result of EMU (Hassel 2014). MMEs lost competitiveness as labor costs surged without corresponding gains in productivity, and they could no longer restore competitiveness via devaluation. Figure 1.4 shows the wage discipline in Germany that even had negative changes prior to the crisis, whereas the LME and MME countries under study were significantly higher during this period.

Figure 1.4 Annual percentage change in nominal unit labor costs, 1999–2017.

Source: Eurostat.

Prior to the crisis, ECB interest rates were too high for the northern economies experiencing a slump and too low for some of the southern economies in a real estate boom. Figure 1.5 shows the inflation rates for the countries under study versus that of the euro area; while the latter mainly followed the 2 percent goal of the euro area, this masked the stronger inflation in the MME and especially LME countries under study compared to the euro area average, some significantly so.

Figure 1.5 Annual inflation rate (measured by rate of change of HICP) for euro area 18, Greece, Ireland, Italy, Portugal and Spain, 1999–2017.

Source: Eurostat.

The historically low interest rates for the MMES combined with the explosion of the finance industry made credit abundant. It thereby created a “fragile and perverse complementarity in financial markets” (Fuller 2018, p. 175), as capital from the north drove demand-led growth in the periphery and promoted the export of goods and capital in the north. Large imbalances arose in the euro area as competitiveness diverged, though the access to this cheap credit during the first decade of EMU allowed MMEs to easily finance their debt (Scharpf 2011): “The euro allowed Germany to pursue real exchange rate depreciation through the exertion wage restraint and facilitated the recycling of its export surpluses, thereby creating incentives for unbalanced consumption-led growth in the MMEs and LME” (Vermeiren 2013, p. 731). Although Ireland and Spain have different VOC models, both grew rapidly as a result of rea...

Table of contents

Cover

Half Title

Series Page

Title Page

Copyright Page

Table of Contents

List of figures

List of tables

List of boxes

Notes on contributors

Preface by Paul De Grauwe

Acknowledgments

List of abbreviations

1 After the bailout: 10 years of the euro area crisis

PART I The European dimension of the crisis

PART II Country studies

PART III National growth models and the political economy of adjustment

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Political Economy of Adjustment Throughout and Beyond the Eurozone Crisis by Michele Chang, Federico Steinberg, Francisco Torres, Michele Chang,Federico Steinberg,Francisco Torres in PDF and/or ePUB format, as well as other popular books in Politics & International Relations & Politics. We have over 1.5 million books available in our catalogue for you to explore.