Dispute Resolution in Islamic Finance addresses how best to handle disputes within Islamic finance. It examines how they can be resolved in a less confrontational manner and ensure such disagreements are settled in a just and fair way.

There has been little focus on how disputes within Islamic finance are resolved. As a result, many of these disputes are resolved through litigation, notwithstanding that the various jurisdictions and court systems are generally poorly equipped to handle such matters. This book addresses this gap in our knowledge by focusing on five centres of Islamic finance: the United Kingdom, the United States of America, Malaysia, the Kingdom of Saudi Arabia and the United Arab Emirates. Before exploring these countries in detail, the book considers the issues of the choice of law within Islamic finance as well the prevailing forms of dispute resolution in this form of finance.

The book brings together a group of leading scholars who are all specialists on the subject in the countries they examine. It is a key resource for students and researchers of Islamic finance, and aimed at lawyers, finance professionals, industry practitioners, consultancy firms, and academics.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

1 In search of an effective dispute resolution mechanism in Islamic finance

Adnan Trakic, John Benson and Pervaiz K Ahmed

Introduction

Islamic finance has grown rapidly since the beginning of the new millennium. In 2003 Islamic financial assets were approximately US$200 million; by 2013 these assets had grown to an estimated US$1.8 trillion.1 By the end of 2017 total Islamic assets were valued in excess of US$2 trillion.2 This growth has outperformed conventional finance in this period with much of this growth occurring in the Gulf Cooperation Council (GCC) countries, Iran and Malaysia. In these countries Islamic finance has increased the penetration rate to above 15 per cent of all financial assets.3 Whilst still a minor share of the global financial assets the recent growth has been due to a desire of many people and institutions to have a more ethical form of banking as well as a significant growth in the number of Islamic compliant financial products being offered.

Islamic or Shari’ah compliant products offered by Islamic banks are tailored by Islamic financial institutions (IFIs) to comply with both Shari’ah (Islamic law principles) and laws of the jurisdictions in which they operate. Shari’ah compliance is an important governance layer in IFIs, which not only ensures that products offered are in compliance with Islamic principles but also ensures that all processes and dispute resolution mechanisms adopted by the IFIs are consistent with Shari’ah. Islamic financial transactions are, in many cases, intra-national but increasingly involve parties originating from different countries. In practice, parties in cross-border Islamic financial transactions normally choose English law as the basis to their contractual documents, or the law of another country like Malaysia, instead of Shari’ah.4

As a consequence, when disputes occur and parties choose litigation (resolution of disputes through the courts), the courts of those countries are more likely to treat the Islamic finance transaction as a conventional contract and apply domestic conventional law thereby neglecting the Shari’ah underlying nature of the transaction.5 An examination of English and Malaysian cases involving Islamic finance matters shows that the courts are not well-equipped to adjudicate Shari’ah aspects of the Islamic finance contracts.

This deficiency in litigation has led to debate about whether litigation through the court system or some form of alternative dispute resolution (ADRs) mechanism should be the preferred process for dispute settlement in Islamic finance.6 A number of studies have shown that Islamic financial institutions have generally favoured litigation over ADRs when attempting to resolve disputes.7 In recent years, however, there has been a move in Islamic finance towards the use of alternative dispute resolution mechanisms, especially arbitration. It has been claimed that arbitration and mediation, which have a strong basis in Islamic jurisprudence, have an advantage over litigation as they promote settlement of disputes speedily and discreetly.8 Some proponents of arbitrations have gone further and suggested that arbitration clauses should be made mandatory in Islamic finance agreements.9

This recent trend raises an important question: are there viable alternatives that can be used to resolve disputes in Islamic finance whilst maintaining the fundamental basis of Shari’ah both in principle and contract? This volume addresses this weakness in the literature and key research gap by exploring alternative dispute resolution mechanisms that could serve to resolve disputes in Islamic finance in a more appropriate way.

Alternative dispute resolution mechanisms

As with all forms of contractual agreements disputes between the parties will, from time to time, occur. There are a number of mechanisms that can be used to resolve such disputes which lead to the question: can products offered by the IFIs withstand the test of time and remain Shari’ah compliant even after the disputes have been resolved? If the contracting parties have chosen an appropriate Shari’ah compliant dispute resolution mechanism, an Islamic finance product is likely to remain Shari’ah compliant. Therefore, it is important to have an effective and appropriate dispute resolution mechanism in Islamic finance, which not only upholds the intentions of the parties as evidenced by their agreement but also recognizes and enforces the Shari’ah underlying nature of the Islamic finance transaction.

There is at present an on-going debate as to whether litigation or alternative dispute resolution mechanisms, such as arbitration or mediation, is more effective in the settlement of Islamic finance disputes. A variety of ADRs are available, although the most common are conciliation, mediation and arbitration. Conciliation involves an impartial third party directing negotiations to assist the parties to reach a mutually acceptable agreement. Mediation is a similar dispute settling method to conciliation (often used interchangeably) and involves an impartial and independent third party facilitating dialogue to assist the parties to reach a mutually acceptable agreement. Both these approaches are less adversarial than litigation or arbitration and have a clear focus on the actual outcomes. Mediation is different to conciliation in that whilst it has a similar aim its focus is on process and encouraging the parties to articulate their own interests, priorities, needs and wishes to each other.

Arbitration is a more formal process than conciliation or mediation and aims to settle the dispute through the parties presenting their case to an independent, qualified third party (or a panel). The arbitrator can be chosen by the parties. This ADR has many variants, such a final-offer arbitration, and involves the arbitrator or panel of arbitrators handing down a decision (often referred to as an award), which can be binding or non-binding. The dispute is considered settled with the final decision, although in some cases, depending on the particular system or prior agreement between the parties, a decision can be appealed. Arbitration decisions usually remain private and conciliation or mediation can serve as a useful prelude to arbitration.

In contrast to these mechanisms, litigation is a contested proceeding where a party files a lawsuit against another party. It can be costly, usually slower and often with the power balance between the parties unequal. The general aim of litigation is to declare a winner rather than to resolve the disputes or address what is perceived as an inequity. Litigation does however, allow for full discovery, gaining and/or enforcing interlocutory measures against a party, legal enforcement of the decision, and a formal appeals process. Litigation also leads to a public body of consistent decisions that can be used as precedence in future similar disputes.

Key objectives and research approach

The book has four major objectives that underpin the analysis of the questions and the countries explored. First, to increase the awareness of dispute resolution mechanisms and infrastructure available for effective resolution of Islamic finance disputes. Second, to enable proponents and opponents of litigation and ADRs in Islamic finance to present their arguments in an appropriate manner. Third, to enable the participants from industry, the judiciary, and academia to learn from the presented views. Fourth, to suggest to the related bodies and government agencies reform of the existing laws and policies, where considered necessary.

These objectives lead to the following questions:

• What are the appropriate ways to settle disputes in Islamic finance and do such approaches vary depending on context and issue?

• What basis in Islamic law exists to support the various dispute settling processes and what are the arguments against the adoption of such processes?

• How ready are Islamic financial institutions to reconsider the ways they currently use to resolve disputes?

• Is there a strong argument, based on Islamic law, for the reform of existing laws and policies governing the way disputes can be, or should be, settled?

Further questions that the book will address are provided in the discussion of the case study countries in the following section.

The case study jurisdictions

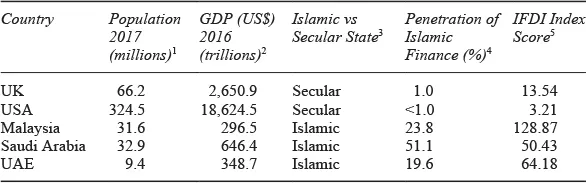

To answer these questions the monograph will focus on five countries specifically chosen to provide a contrast in context and in the significance of Islamic finance. The first two countries, the United Kingdom (UK) and the United States of America (US), are large, industrialized economies. They are both secular societies and have a legal framework that represents such secularity. Islamic finance is not a major financial actor at the present time in either of these countries. They have been included, however, due to the large number of international Islamic financial transactions taking place in both jurisdictions and that many financial contracts have a clause relating to settlement under the prevailing secular laws of these countries. The last three countries, Malaysia, Saudi Arabia and the United Arab Emirates (UAE), are smaller and developing economies, although they have some of the largest Islamic financial providers. All three are Islamic countries10 that subscribe to Islamic law and have strong Islamic banking institutions as can be seen by their top five rating on the Islamic Finance development Index. This is particularly the case with Malaysia which is arguably the most advanced jurisdiction in Islamic finance. Details are presented in Table 1.1.

The UK’s and US’s laws and courts tend to be the most popular choice among the parties in international Islamic transactions. The Islamic finance cases decided in both jurisdictions lead to the conclusion that the courts are not prepared or well equipped to recognize and enforce Shari’ah aspects of an Islamic finance agreement. As a result, the courts, through the adjudication process, inadvertently transform an Islamic finance transaction into a conventional one. The situation seems to be different in arbitration. Arbitration legislations in both countries are accommodative of Shari’ah principles involved in Islamic finance transactions. This monograph will investigate the above claims and will address the question as to whether the above jurisdictions are appropriate forums for the settlement of Islamic finance disputes.

Table 1.1 Selected data for case study countries

Sources: 1 United Nations, ‘World Population Prospects (2017 Revision), 2017’ https://esa.un.org/unpd/wpp/publications/Files/WPP2017_KeyFindings.pdf accessed 16 June 2018. 2 World Bank, World Bank National Accounts data and OECD National Accounts data files, 2016 https://data.worldbank.org/indicator/NY.GDP.MKTP.CD accessed 16 June 2018. 3 A secular state is a country whose laws and institutions are not connected to any particular spiritual or religious doctrine (for further details see the Oxford Dictionary). 4 Islamic Financial Services Board, ‘Islamic Financial Services Industry Stability Report 2017’, Islamic Financial Services Board, Kuala Lumpur, pp. 8–9. 5 ICD-Thomson Reuters, ‘Islamic Finance Development Report 2017, Thomson Reuters and Islamic Corporation for the Development of the Private Sector, available at https://islamicbankers.files.wordpress.com/2017/12/icd-thomson-reuters-islamic-finance-development-report-2017.pdf accessed 17 June 2018. This index covers five criteria: Quantitative development, knowledge, governance, corporate social responsibility, awareness. Malaysia is currently ranked number 1, whilst Saudi Arabia and UAE are in the top five globally.

Malaysia has, arguably, the most advanced laws on Islamic finance anywhere in the world. Malaysian courts are experienced in dealing with Islamic finance cases. The Malaysian dispute resolution mechanism for Islamic finance cases is unique in the sense that the courts are obliged to refer Shari’ah aspects of the agreement to the Shari’ah Advisory Council of either the Central Bank or the Securities Commission for ascertainment and ruling.11 The legislative provisions allowing for this, however, have been under attack recently. The Federal Court decision, in 2017, in Semenyih Jaya Sdn Bhd v Pentadbir Tanah Daerah Hulu Langat emphasized that the judicial power of the court can only reside in the judiciary and provision of a federal law which usurp the judicial power of the court are unconstitutional. This monograph will assess the suitability and effectiveness of the Malaysian dispute resolution mechanism for Islamic finance. It will also investigate the constitutionality of the impugned legislative provisions in the light of the recent Federal Court decision. Malaysia is home to the Asian International Arbitration Centre (AIAC),12 which has recently passed AIAC i-Arbitration Rules 2017, which is the first of its kind anywhere in the world. The monograph will thus ...

Table of contents

Cover

Half Title

Series Page

Title Page

Copyright Page

Table of Contents

List of tables

Notes on contributors

Preface

1 In search of an effective dispute resolution mechanism in Islamic finance

2 Choice of law in Islamic finance

3 Prevailing dispute resolution mechanisms in Islamic finance

4 Islamic dispute resolution in the United Kingdom

5 Settlement of Islamic finance disputes in the United States of America

6 Settlement of Islamic finance disputes in Malaysia

7 Settlement of Islamic finance disputes in the Kingdom of Saudi Arabia

8 Settlement of Islamic finance disputes in the United Arab Emirates

9 Dispute resolution in Islamic finance: the way forward

List of statutes and regulations

List of cases

Bibliography

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Dispute Resolution in Islamic Finance by Adnan Trakic, John Benson, Pervaiz K Ahmed, Adnan Trakic,John Benson,Pervaiz K Ahmed in PDF and/or ePUB format, as well as other popular books in Business & Islamic Banking & Finance. We have over 1.5 million books available in our catalogue for you to explore.