eBook - ePub

Comparative Regionalisms for Development in the 21st Century

Insights from the Global South

- 294 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Comparative Regionalisms for Development in the 21st Century

Insights from the Global South

About this book

The global 'financial' crisis at the turn of the decade has accelerated changes in the relative standing of major regions. As both the US and Eurozone economies have confronted a series of setbacks and struggles to find their second breath, so Asia, Latin America and even Africa have picked up the slack and have been able to maintain high levels of growth. The resilience of the Global South questions whether we are witnessing an evolution towards a regional rebalancing or even global restructuring. This responding volume has four interrelated topics. It explores the transformation taking place in/with regard to the financing of development in the Global South and the apparition of new players in the field. The emergence of 'New Regionalisms' in the South and the usefulness of these experiences for comparative studies of regional relationship is explicated. It turns its attention to new forms of transnational governance that are emerging and the role that a novelty of actors play in this 'new multilateralism'. Finally, it looks into the implications of this trio of novel directions and players for analyses and policies.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Chapter 1

Competitive Bilateralism or Regionalism: A South African Perspective

The global trading system is characterized by a growing and competing network of bilateral and regional trade agreements. In South Africa, while trade policy has been determined in a multilateral setting, bilateral and regional trade agreements have also been pursued as evidenced by the Southern African Development Community Free Trade Agreement (SADC FTA), the European Union-South Africa Trade, Development and Co-operation Agreement (EU-SA TDCA) and as a member of the Southern African Customs Union (SACU), a party to the SACU European Free Trade Association-Free Trade Agreement (SACU- EFTA FTA) and the SACU Common Market of the South-Preferential Trade Agreement (SACU-MERCOSUR PTA).

However, the verdict is still out on whether South African trade has benefited from preferential access into the United States under the African Growth and Opportunity Act (AGOA). Overlaying these arrangements, there are also ongoing Economic Partnership Agreement (EPA) negotiations with the European community. Policy makers in South Africa, despite multilateral commitments, continue to negotiate preferential deals with other countries. The official March 2011 entry of South Africa to the Brazil, Russia, India and China (BRIC) group illustrates this competitive trend within African regionalism.

Against this background, it is questionable therefore whether these bilateral and regional trade agreements are beneficial to South African trade in general. This chapter aims to investigate whether the two preferential free trade agreements, the SADC FTA and EU-SA TDCA, have had any significant impact on trading patterns and revealed comparative advantages for South Africa. Furthermore, this chapter also attempts to explore the merits for the co-existence of other preferential trade agreements.

Introduction

Discussions about international relations are focusing increasingly on bilateral and regional trade agreements. Since the 1990s, the global trading system is characterized by a growing and competing network of bilateral and regional free trade agreements (FTAs). As of January 10, 2013, the World Trade Organization (WTO) is monitoring some 546 notifications of FTAs with 354 agreements in operation. In just a decade, the number of active FTAs is up by almost 50 per cent (from 180 agreements in 2003). Most WTO members are party to one or more FTAs. Going by present trends, it is expected that the share of trade through bilateral and regional FTAs will continue to rise.

In South Africa, while trade policy has been determined in a multilateral setting, bilateral and regional trade agreements have also been pursued. After a period of phased-in aggressive trade liberalization agreed under the Uruguay Round of the General Agreement on Tariffs and Trade (GATT), bilateral and regional trade agreements began to play a larger role.

In the year 2000, South Africa concluded two major preferential FTAs: a bilateral FTA with the European Union – the European Union-South Africa Trade, Development and Co-operation Agreement (EU-SA TDCA) and a regional-plurilateral FTA with the Southern African Development Community – the Southern African Development Community Free Trade Agreement (SADC FTA). Holden and McMillan (2006) show that the EU-SA FTA stimulated both exports and imports for South Africa, but while South African exports to SADC were stimulated, the results for imports were ambiguous. The AGOA results were far less significant overall, suggesting that preferential access for South African exports into the United States had not been particularly beneficial.

Overlaying these arrangements, there are also ongoing Economic Partnership Agreement (EPA) negotiations with the European community. Policy makers in South Africa, despite multilateral commitments, continue to negotiate preferential deals with emerging trading partners. The official March 2011 entry of South Africa to the BRIC group illustrates this competitive trend within African regionalism.

It is our view, therefore, that South Africa’s increasing engagement in the world economy and liberalization of trade creates competitive pressures and a potential shift in the country’s comparative advantage in the international market. Also, with the EU-SA TDCA 12-year implementation horizon soon coming to an end, and taking into account the inclusion of South Africa into the SADC EPA negotiations, our analysis will make a contribution to the debate. The chapter therefore focuses on identifying whether South African trade has been affected in recent years by the granting of preferential access under these agreements. In addition, in a south-south developing mandate, given that a preferential trade agreement framework was signed by the Ministers of Trade in South Africa and Brazil in 2000, this chapter also attempts to explore the merits of the co-existence of a potential FTA with Brazil.

Our chapter proceeds as follows: In the next section, we provide some of the stylized facts concerning South Africa’s trading export and import patterns. Thereafter, we discuss our methodology and data. Specifically, this study uses a modified version of the Balassa (1965) index to identify South Africa’s most competitive commodities relative to the EU and SADC, in terms of the ‘revealed’ comparative advantage and also determine to what extent the most competitive commodities witnessed a shift in their trade competitiveness. Additionally, of added value, this study investigates the revealed competitiveness of South Africa relative to Brazil, an increasingly important emerging trading partner; and also identifies the major products that have export potential for South African producers. The last section concludes.

South Africa’s Patterns of Trade: Stylized Facts

Over the last decade, when looking at South Africa’s pattern of international trade, four major relevant themes are apparent: a significant increase in the country’s openness, the dominance of manufacturing, a geographical diversification in its trade and an unbalanced bilateral and regional trading.

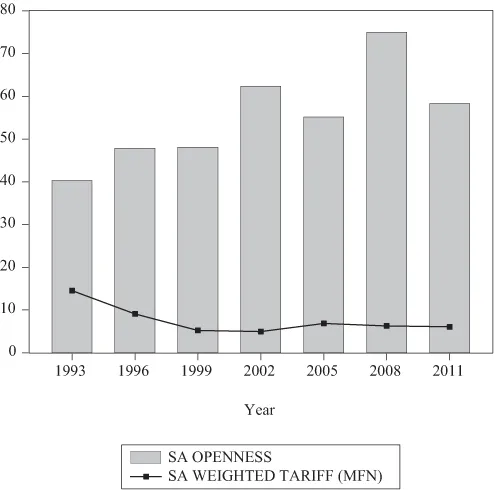

South Africa’s trade has been considerably liberalized since the early 1990s (Jonsson and Subramanian 2001). South Africa is an open economy. As illustrated in Figure 1.1 below, the ratio of trade relative to GDP has increased significantly from 40 per cent in 1993 to 58 per cent in 2011. Also, South Africa’s average most favoured nation (MFN) applied tariff rate is of interest, and as shown in Figure 1.1 has dropped considerably from 14.5 per cent in 1993 to 6 per cent in 2011 in line with that of an average upper-middle-income economy.

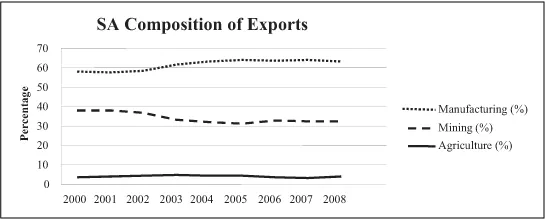

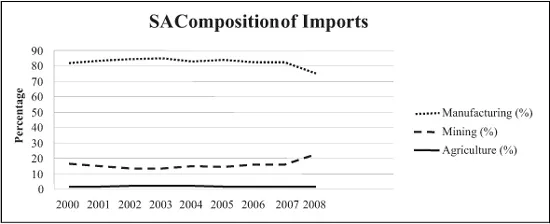

To provide more insight into this increased openness, Figures 1.2 and 1.3 show the country’s composition of trade. Manufacturing is by far the main driver in exports from and imports into South Africa.

From a geographical standpoint, South Africa’s trade remains concentrated with relatively high-income traditional partners in the north, but this concentration of trade is decreasing and there seems to be a reallocation of trade moving towards key emerging markets in the south, as shown in Figures 1.4 and 1.5.

Additionally, a noteworthy point is that while Germany has consistently been South Africa’s major individual trading partner, since 2009, China has become the country’s most important individual trading partner when total trade between the two countries amounted to about US$ 15 billion. In 2011, South Africa’s total bilateral trade with China has reached almost US $30 billion, with an SA deficit of about US $2.5 billion.

Regarding South Africa’s regional trade, the European Union as a bloc remains South Africa’s most important regional trading partner as evidenced in Figures 1.6 and 1.7.

Figure 1.1 Trade Openness: 1993-2011

Source: Authors’ calculations based on UNCTAD (2012) database

Figure 1.2 Exports Composition: 2000-2008

Source: Authors’ calculations based on DTI (2010) data

Figure 1.3 Imports Composition: 2000-2008

Source: Authors’ calculations based on DTI (2010) data

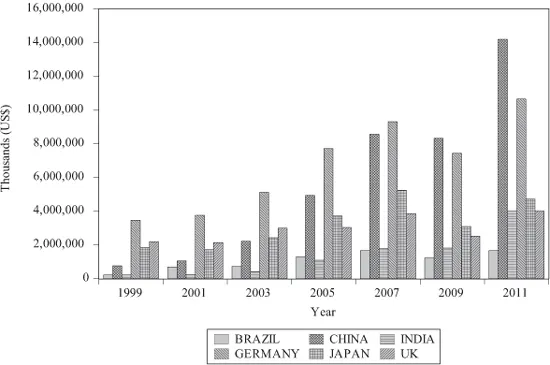

Figure 1.4 Key Trading Import Partners: 1999-2011 (US$)

Source: Authors’ compilations based on UNCTAD (2012) data

Figures 1.6 and 1.7 also show that the country has slowly developed a more integrated trade with the African, Caribbean and Pacific States. According to our estimates based on UNCTAD (2012) data, South Africa’s trade with Africa is focused on the SADC re...

Table of contents

- Cover Page

- Title Page

- Copyright Page

- Contents

- List of Figures and Tables

- Notes on Contributors

- Foreword

- Acknowledgements

- List of Abbreviations

- Introduction: Comparative Regionalisms for Development in the 21st Century: Insights from the Global South

- 1 Competitive Bilateralism or Regionalism: A South African Perspective

- 2 Understanding Regional Integration Policies in Africa

- 3 UNASUR in the Context of a Changing Regional Environment: Prospects and Challenges

- 4 Constraints to Regional Integration in Central Africa

- 5 Development in the Caribbeans After a Half-century of Independence: Insights from Regional and Transnational Perspectives

- 6 Regional Integration in the Pacific

- 7 Regional Aid for Trade in Africa: Time to Walk the Talk

- 8 Food Security in ECOWAS

- 9 Impact of Regional Integration on Human Rights Protection in Africa

- 10 The Role of Regional Parliaments in Enhancing Democracy in the South

- 11 Regional Economic Integration in Africa: Impediments to Progress?

- 12 Regional Formations and Global Governance

- Conclusion: New Regionalisms: Beyond NETRIS

- Appendix

- List of Websites

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Comparative Regionalisms for Development in the 21st Century by Timothy M. Shaw, Emmanuel Fanta in PDF and/or ePUB format, as well as other popular books in Economics & Political Economy. We have over 1.5 million books available in our catalogue for you to explore.