This book facilitates a systematic comprehension of internal workings of corporate governance in practice. Facets of this multidisciplinary, constantly evolving field are discussed and interrelationships among them are explained to provide insights on how certain precepts come into play for various roles in governance. This book pragmatically explains and illustrates with a view to integrate. To keep the scope achievable, the emphasis is placed on the U.S.-based companies; where possible, differences in governance around the world are identified.

Three rich sources of knowledge help shape the message of this book: existing paradigms, personal experience in governance, and research on issues and challenges of governance.

Features:

Permits a holistic view of the complex corporate governance landscape.

Discusses and generously illustrates the practice of corporate governance.

Aids understanding of issues and challenges of corporate governance.

Identifies ways to advance the value of one's role in corporate governance.

Teaches how to avoid crucial mistakes that compromise the value of one's contribution in the governance process.

If you are a professional accountant, securities lawyer, economist, financial analyst, auditor, executive, entrepreneur, or an investor, you will find the book helpful in understanding the entire landscape of governance fairly quickly. Those already involved in the governance arena may find the book refreshing, and may use it to coach others. This book can serve as a reference book in any offering of a course at any academic level.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

An overarching purpose of governance is to maintain trust in those who manage others’ interests. The idea of governance applies to any group or entity, not just corporations. Take, for example, the neighborhood homeowners’ association. It directs and controls what happens to the neighborhood in the immediate future and in the long run. The association initiates rules such as how the park inside the neighborhood will be used, where in the neighborhood speed bumps should be installed, and how pets will be handled in the public areas by their owners. In addition, the association enforces covenants that deal with the external look of each house, approves modifications to existing structures, and addresses complaints regarding violation of the covenant by any of the members. The governance structure permits the neighborhood to preserve its esthetics, help maintain the infrastructure such as roads and parks within the neighborhood, help protect the area from criminal activities, and keep the valuation of homes attractive. Many of these benefits would not occur if the houses in an area were not subject to governance by the homeowners’ association. In essence, the association is trusted by the homeowners to do the right thing in their best interests. The cost of membership imposed on each owner is probably worth the discipline imposed on the neighborhood as a whole.

What works for a small organization becomes almost a necessity for a corporation with fiduciary accountability to its investors. At the core of corporate governance is a system that directs and controls the organization. Corporate governance is an evolving discipline that has been around for as long as public limited companies have existed. In recent years, corporate governance is clarified as GRC – governance, risk, and compliance – thus embedding the major governance responsibilities of risk management and compliance with the laws and regulations into its fold. As such, implicit in effective corporate governance is an interplay of several disciplines including accounting, finance, risk management, leadership, law, information technology, communication, and organizational behavior.

The purpose of corporate governance is to direct and control the activities of an organization by establishing structures, rules, and procedures for decision making. There is no set formula to translate this into what it means for a corporation; every case is different. Take, for example, a company that provided IT outsourcing services and due to continued growth, set up a major offshore center for this purpose. The idea was to benefit from access to skills at a very reasonable price. Practically, almost all client services were performed by this center with about ten thousand employees at the overseas center. The board considered the significance of the offshore center and attendant risks and decided that it would meet at the offshore location at least once every year for a longer than an average board meeting. As is evident in the board’s decision, the business model, company’s maturity stage, rate of growth, and changing risks should dictate appropriate governance steps. The governance in action is highly influenced by the complexity of the firm, uncertainty faced by the company, and the need for adaptation in changing environments.

Meaning of Governance

Governance means to regulate internally. The term governor in the field of engineering implies some mechanism that will measure and regulate the key outcomes of the device. An example is the centrifugal governor which regulates the machine’s speed by exerting centrifugal force on rotating weights driven by the machine output shaft. Synonyms for governance include protector, steersman, and pilot. Each term describes some component of governance but, by itself, is not sufficient to express the overall spirit of governance. Collectively, these terms imply the need to govern – to protect, steer in a certain direction, or to pilot its trajectory and control its flight path. In engineering, the device is separately identifiable from the mechanism that regulates the performance of the device. In corporate governance, at least notionally, one may identify the company and its management as the “device” and the board of directors as the “mechanism.” In the future, this idea of physical separation may be defied as, for example, in the case of a driverless car, where the car itself has the artificial intelligence to self-govern its particular journey.

As long as the owner and the business are essentially the same (that is, the owner directly controls the business), there is no need for a separate force to regulate the business. However, once the owner is separated from the management of the business, the owner – who now has very little control over the firm – becomes concerned about how well the business is doing. A corporation as a separate legal entity does just this; it separates the owners – providers of equity – from the management of company operations and strategy.

Corporations may be public companies or private companies. In private companies the owners are likely to be somewhat hands-on in the management of the business. As a result, there may not be as severe a need to govern as there would be for a company whose voting shares are publicly traded and owned by many, often numerous, investors. Foreign public companies that participate in the U.S. financial markets are, for all practical purposes, treated the same as public companies. The shares of foreign companies are usually listed in the U.S. financial markets as American Depository Receipts (ADRs), a negotiable certificate issued by a U.S. depository bank representing a specified number of shares, perhaps even a fraction of a share.

The separation of shareholders from management is accompanied by a vast amount of equity invested by the shareholders; their financial well-being is tied to how well their company is doing. After all, they are the ones who put at risk their investment in the owner equity of the company; although the management may be managing the company, they are at the risk of losing their investment if the company does not do well. At the same time, as a group, they wield considerable influence as providers of capital they invest in the company.

Shareholders and Management

If you look at who has invested in the voting shares of a company, you might find individual investors, banks and other financial institutions, retirement funds, charities, mutual funds, hedge funds, and exchange traded funds (ETFs). Such dispersed ownership may be appropriate for raising equity, but it certainly does not lend itself to owners having an intention or interest in direct management of the company. Today’s complex businesses working in a dynamic environment require the expertise of dedicated professional management.

By design, shareholders agree to not get involved in the management of the company. And the managers agree to do the best they can to achieve the goals of the company directed primarily toward increasing shareholder equity in the business. So, the relationship is mutual: shareholders benefit when the company prospers, and management is rewarded as they lead the company to do well. What could go wrong in this relationship? Perhaps management fails to deliver or expends a disproportionate amount of resources to do so. It could be that management chooses alternatives that are more (or less) risky according to the owners, or that are not what the owners would pick. Thus, there is a built-in tension between the two.

An additional factor contributing to the complexity of the relationship between the shareholders and management is the issue of information asymmetry between the two. Management runs the show and, therefore, has all the data and information they need; on the other hand, the shareholders do not have access to information unless, and only to the extent, required by regulatory measures. While full access to all company data is neither desired nor expected by the shareholders, they do expect that information necessary for the governance of management will be available to them in a timely manner and in appropriate detail.

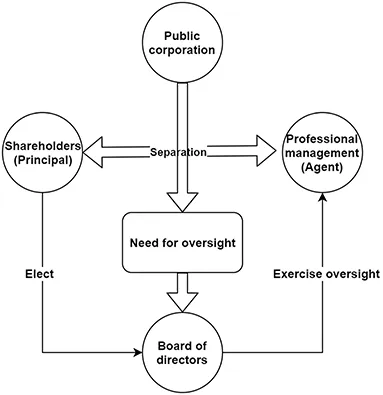

Finally, even with the arrangement of having professional management conduct the affairs of the company to grow value for the shareholders, the dispersed group is too large and practically unable to manage directly their agent, the top brass in the company. To solve this problem, shareholders elect a group of representatives as directors to form the board of directors. The board in turn provides oversight on management in the interest of the shareholders. Conceptually, another layer of principal-agent is added: management (agent) reports to the board (principal) who is an agent of the shareholders (principal). Thus, the burden of governing the company falls on the few organized as the board of directors of the company. Figure 1.1 provides an overview of the agency in corporate governance.

Figure 1.1 Agency in corporate governance.

Agency Problem

The idea of an owner having an agent manage the affairs of the owner-entity is not new; it has surfaced in various contexts. An apartment complex can hire a fulltime resident manager to manage the complex, a city can outsource the running of its mass transit system to another entity, and a shopping mall can hire services of a security firm to ensure that the mall is secure and people visiting or working in the mall shops are safe. The owner is called the principal and the manager, the agent. The principal-agent relationship is articulated in the widely known agency theory.

Within the context of the agency theory lies the agency problem or agency dilemma. Take, for example, a medical doctor’s clinic that has acquired a new diagnostic machine. The machine is expensive, and the clinic would like to generate as much cash flow from it as possible in a relatively short period of time. The doctor may desire to recommend more of his patients for the diagnostics available through this machine, although in some cases there may be little need for the diagnosis. The patient trusts the doctor as his agent, but the outcome for the patient turns out to be more expensive and less fruitful!

The agency problem vividly illustrates that conflicts of interest may exist in an agency. Where conflict of interest emerges, the behavior of management – the agent – may not be aligned to the best interests of the shareholders – the principal. To manage their risk, owners would want to control senior management to generate management behavior congruent with shareholder interests. For this, the shareholders may deploy control mechanisms such as the following:

Regularly scheduled meetings between shareholders and management, for example, quarterly conference calls.

Publicly available media coverage of the company and the industry to which it belongs.

Pay-for-performance: an instrumentality designed in the compensation plans for the top executives wherein the shareholder interests are aligned with management incentives.

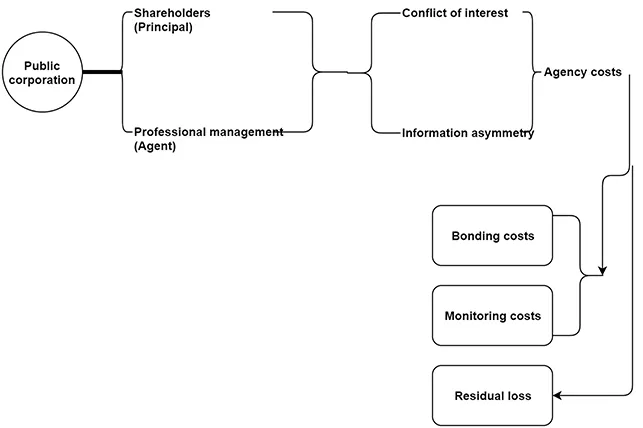

Agency Costs

Agency costs are a result of the possible deviation of agent behavior from the principal’s expectations. Where such deviations are anticipated, the principal may develop measures to control such behavior; this, in turn, will result in agency costs. Unexpected deviations, while they cannot be controlled, will still result in some losses or other consequences, which are also a part of agency costs. The aggregate agency costs are normally classified as follows:

Bonding costs: Costs of preplanned mechanisms agreed between the shareholders and management. These include proactive initiatives that will stabilize and align shareholder expectations with management’s behavior. A performance-based compensation plan for top executives is an example of bonding costs.

Monitoring costs: Costs incurred to observe and control management’s behavior and to verify the results of the company financial performance through an independent audit. While excessive monitoring intrudes on management’s freedom to steer the enterprise, too little monitoring could cause behavior contrary to shareholder expectations. As a result, moderation in monitoring activities is a desirable attribute.

Residual loss: Residual losses arise from conflicts of interest which cannot be controlled due to lack of alignment between shareholder and management interests. Consequently, management misbehavior causes additional costs or losses to the shareholders.

Figure 1.2 provides an overview of the origin of agency costs.

Figure 1.2 An overview of the agency costs.

Other Theories

While the agency theory has gained a great deal of attention in the corporate governance field, competing theories have been proposed. These include transaction cost theory, resource dependency theory, and stewardship theory.

Transaction Cost Theory (TCT) provides insights into why organizations are structured in certain ways and how they cope with uncertainty. If assets to be deployed by the firm are too specific (that is, have limited alternative uses in the outside market), chances are, the firm would prefer to own or control such assets. This reduces the amount of uncertainty. If the environmental uncertainty stems from the supply-side of inputs, it is likely that the firm would consider vertical integration of its operations by acquiring the sources of supply. For example, an oil refinery would also own crude oil producing facilities. The understanding of the organization structure, how it is staged to cope with uncertainty, and how it is changing over time in response to changing uncertainty is important from the perspective of risk management and resource allocation within the firm. Strategic decisions, such as make-or-buy, can be contextualized and assessed effectively using insights from the TCT.

An organization is essentially a collection of resources, tangible and intangible. The mix of resources owned or controlled by the organization results in the strength or power to the organization. This potentially powerful mix of assets is leveraged in dealing with the external factors, such as the customers, suppliers, and competitors. Management in this per...

Table of contents

Cover

Half Title

Series Page

Title Page

Copyright Page

Dedication

Table of Contents

About the Author

Foreword

Preface

PART I Cornerstones

PART II Governance Roles and Structure

PART III Governance in Action

PART IV Other Topics

APPENDIX A: LIST OF ACRONYMS

APPENDIX B: LIST OF WEB-BASED RESOURCES

INDEX

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Corporate Governance by Vasant Raval in PDF and/or ePUB format, as well as other popular books in Betriebswirtschaft & Wirtschaftsprüfung. We have over 1.5 million books available in our catalogue for you to explore.