From childhood through to adulthood, retirement and finally death, The Economic Psychology of Everyday Life uniquely explores the economic problems all individuals have to solve across the course of their lives.

Webley, Burgoyne, Lea and Young begin by introducing the concept of economic behaviour and its study. They then examine the main economic issues faced at each life stage, including:

* the impact of advertising on children

* buying a first house and setting up home

* changing family roles and gender-linked inequality

* redundancy and unemployment

* coping on a pension * obituaries, wills and inheritance.

Finally they draw together the commonalties of economic problems across the lifespan, discuss generational and cultural changes in economic behaviour, and examine the significance of other, non-economic constraints, upon individuals.

The Economic Psychology of Everyday Life provides a much-needed comprehensive and accessible guide to economic psychology which will be of great interest to researchers and students.

eBook - ePub

The Economic Psychology of Everyday Life

- 224 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The Economic Psychology of Everyday Life

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Subtopic

History & Theory in PsychologyIndex

Psychology1

An Introduction to Economic Psychology

What is Economic Behaviour?

We all think we know what economic behaviour is—it is about buying a computer, thinking about investment options, looking at a saving advert and wondering whether we ought to put some money by, choosing a holiday, and evading one’s taxes. But do we really? The behaviours in the opening sentence all seem economic but how about this list: deciding to have children, stealing a car, making a Christmas present, washing one’s clothes. Or walking to work (as opposed to going by car), visiting a friend who lives nearby (as opposed to one who lives further away), giving a friend a lift. By some formal definitions all of these behaviours (and indeed virtually all behaviour) can be seen as economic (Webley and Lea, 1993b). The central concept usually deployed here is scarcity: as Robbins (1932, p. 16) wrote ‘Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses’. Economists do not need to confine themselves to those domains we traditionally think of as ‘economic’ (markets, pricing, labour supply) and the intellectual imperialists such as Becker (1976, 1991) have striven hard to extend the scope of economics to explain, among other things, criminal and family behaviour. An alternative view sees economic behaviour simply as those areas that are generally seen as economic (buying, work, saving, etc.), usually as these are activities that go through the market (see Webley and Lea, 1993). But none of these definitions (nor others) take us very far: the pragmatic approach used here is to focus on those problems facing individuals at different points in their life that are best understood (or at least illuminated) from an economic psychology perspective. Thus we do deal with saving but don’t deal with mate choice (although one could).

Approaches to Economic Behaviour

It is possible to regard the study of economic behaviour as just another branch of applied social psychology, where at worst one simply applies standard social psychological theories to economic phenomena (e.g. applying attribution theory to understand people’s explanations for poverty) and at best one develops theories that have more general application (Langer’s, 1975, 1983, ideas of illusion of control and mindlessness might be an example of this). We do not take this view. Our belief is that economic behaviour is best understood by a truly interdisciplinary approach that draws on both economics and psychology (and related disciplines). This is not an easy option: economics and psychology have, in the past, had an uneasy relationship, as the conventions of inference and theory construction are very different. Economists have often shown ‘aggressive uncuriosity’ (Rabin, 1998) towards psychological research and psychologists have often been dismissive of a science based on what seem to them to be absurdly unrealistic assumptions. Nonetheless we believe that a truly interdisciplinary approach will bear fruit in the long term and benefit both parent disciplines. Here we outline some of the alternative perspectives that have been brought to bear in the two disciplines.

Optimality—the economist’s approach

To simplify greatly, economists (or strictly speaking neo-classical economists) begin with the assumption that people are self-interested utility-maximisers—they are selfish and rational. So, faced with an interesting question, say the effect of the introduction of fees on applications for university places, the first step would be to construct a model of the behaviour in question. This would consider the quantifiable benefits of university education (the lifetime increase in earnings as a result of having a degree), the risks (the probability of ending up without a degree), and the costs (for example, of renting student accommodation, of forgone earnings). The model would make a number of simplifying assumptions, for example that universities come in only two types (high- or low-status) or that the choice is between a university in one’s home town or in a distant city. The model would be of the behaviour of units in the system: in our example this could be individuals or households, in other cases it could be firms, regulators or the government. The model is then developed, but always on the assumption that the economic units (of whatever kind) are behaving in their own interests and in the most optimal way. It is important to bear in mind that such models do not usually predict the behaviour of individuals (a particular individual may be altruistic, badly informed or make poor judgements): what they do is to predict average behaviour, or what will happen, all other things being equal. So our model might predict that fees would reduce the number of mature applicants for university places (as the impact on their lifetime earnings of having a degree is less and the cost of taking up a place is higher) or might predict that fees would not reduce the overall number of applications but that students would become more likely to be home-based.

Social psychologists often dispute the claim that people are rational and make optimal decisions (they also argue against the assumption of self-interest, but less forcefully). They point to the extensive experimental evidence on decision-making (see, for example, Gilovich, 1991; Plous, 1993), which clearly shows that people often act contrary to rationality assumptions. Psychologists are frequently dismissive of economics as a consequence. We believe that this is misguided on two grounds. First, as we pointed out above, economics does not usually try to predict the behaviour of individuals (any more than a physicist tries to predict the flight pattern of a particular falling autumn leaf). It tries to produce predictions that work well on the average. So the fact that individuals can be shown to act irrationally does not matter as long as aggregate predictions do work well (this is the pragmatic defence of the rationality assumption advanced by Friedman, 1953). We are not so sure this condition is met (indeed, unlike models of weather systems, there is little evidence that models of the economy are getting any better, Wren-Lewis, 1996) but the argument itself is a reasonable one. Second, and much more importantly, it has been convincingly argued by Rachlin (1980) that any behaviour that is consistent can be described as rational. This may require some redefinitions and extensions to the basic theory (for instance, taking into account the costs and benefits of searching for information or the costs of remembering previous decisions) but does not alter the fact that it is fairly pointless trying to ‘disprove’ rationality (for an extended discussion of this issue see Lea, 1994).

Extension of the optimality approach to the whole lifetime

As we said above, economists try to model behaviours on the assumption that people are trying to maximise utility. This means that when dealing with behaviours such as saving, house-buying and career choice, costs and benefits need to be considered over the very long term. Life-cycle models in economics basically assert that people maximise their utility over their lifetime. A typical model of labour supply, for example, would involve an individual maximising utility (which would be a function of hours worked and leisure); a typical model of saving would involve an individual smoothing consumption and integrating income and consumption streams in order to maximise utility. The following quotation is a very clear example of this approach: ‘An individual maximizes a lifetime utility function whose arguments are an aggregate consumption good, annual hours of leisure during work weeks and annual hours of leisure during nonwork weeks subject to a lifetime wealth constraint’ (Reilly, 1994, p. 463). This may seem very unrealistic as it seems to imply that people have very long time horizons. Put in concrete terms it suggests that one of the factors entering into the decision to take a particular job at age 21 will be the quality of the pension deal on offer. But, again, psychologists’ criticisms of these life-cycle approaches are often misplaced. First of all, these are models of what people do and not how they think: it is possible to behave rationally (to act in the optimum way) without having worked out the likely consequences of different choices (that is, to have engaged in rational thought). Second, life-cycle models in economics are now very complex and sophisticated and take into account different time horizons and time preferences; we shall make some use of those in Chapter 5.

The household life-cycle

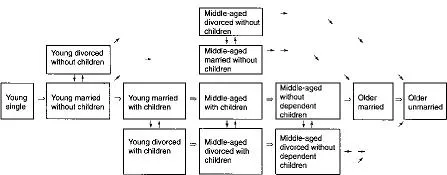

The idea of the household life-cycle (at first called the ‘family life-cycle’) was introduced into the study of consumer behaviour by Wells and Gubar in 1966. This approach basically relates spending and other economic behaviour to transitions in the family situation. These might be, for example, the birth of the family’s first child, the departure of the last child from the household or the death of a spouse. The original model excluded non-traditional households (e.g. people who stayed single or parents who never married) and so a number of researchers have suggested modifications to the original scheme. Here we present the Murphy and Staples (1979) version and its associated diagram (Figure 1.1), which is probably the most widely used. This maintains the idea of progression through stages but recognises that there are alternative routes through the life path.

The traditional family (with seven stages of adulthood) is represented by the middle row, from young single through to older unmarried (widow or widower). There are routes off this representing the major departures from the traditional family: those who do not have children and those whose marriages end in divorce (though Murphy and Staples exclude those who remain single all their lives). This model is more descriptive than theoretical though there is an implicit claim that life stage will be a strong predictor of economic behaviour over and above age and income. The model may give us some handle on changes in economic behaviour during adulthood.

For example, Wilkes (1995) investigated household spending patterns using a very large sample (over 7,000) of respondents to the US Consumer Expenditure survey. Even with this sample some categories had to be collapsed (a serious problem in much earlier research): it was not possible, for instance, to distinguish middle aged divorced families who had never had children from those who currently do not have dependent children. Wilkes shows that including stage of household lifecycle improves the ability to predict expenditure on different product classes over and above what can be achieved using income, age, education and family size: in other words the concept of the household life-cycle does add something. His results reveal three distinct spending patterns. The first is for spending to rise with the shift to married status, then drop with the arrival of children, rise again as families mature and then drop off during the last stages of the life-cycle (the pattern is a sine wave with two maxima). This pattern is found for, among other products and services, eating out, and buying of cars, furniture and clothing. A second, but less frequent, pattern is found for home improvement products, insurance and medical services, which is one of generally increasing expenditure across the life-cycle. And finally, spending on two products (alcohol and stereo equipment) shows a general decline across the life-cycle, which is interpreted by Wilkes as a shift from a self-indulgent perspective to a more sober family-oriented approach to expenditure.

FIGURE 1.1 The modernised household life-cycle model (after Murphy and Staples, 1979)

Although Wilkes is generally positive about the usefulness of the household life-cycle approach, Nyhus (1998) is rather more critical. She points out that twenty years ago Arndt (1979) described the family life-cycle model as ‘one of the most over-quoted and under-researched concepts’ and that this remains a fair description of the current state of affairs. There have been few empirical tests of the model and it seems to add little (in terms of predictive power) to a more straightforward economic life-cycle approach (see for example, Nyhus, 1998; Wagner and Hanna, 1983). Since it is more complex than the latter and has less theoretical grounding, this should give us pause for thought. Nonetheless, from our perspective, it at least provides a framework for thinking about economic choices across the life-cycle.

Developmental psychology

Economists have until fairly recently ignored children (with some honourable exceptions—for example, Harbaugh and Krause, 1999) and have disregarded the value of a developmental approach to understanding behaviour. Broadly speaking, there are two main kinds of theory—one that looks for the origins of economic behaviour in childhood (e.g. Freud, 1908), the other that plots the development of children’s understanding of the economic world (generally through the use of Piagetian stage models, e.g. Berti and Bombi, 1988). Each presents only a partial picture: ‘origin’ theories underestimate the importance of adult experiences and, in particular, the impact of economic constraints and opportunities, whilst Piagetian stage theories overemphasise the significance of adjusting to the adult economic world and minimise the importance of the child’s own behaviour. Both have tended to regard particular ways of thinking and behaving as natural and inevitable, as opposed to being the result of historical and cultural processes.

We can see this if we look at the way each approach deals with money. Freud (and some later psycho-analysts such as Ferenczi, 1926) essentially saw both adults’ approach to money (what one could call styles of economic behaviour, such as stinginess or being a spendthrift) and money stuff itself as a consequence of anal eroticism. The assumption is that all children experience pleasure in eliminating faeces and enjoy playing with these first products. Children then move on to play with mud, and stones, and eventually coins and paper money. Depending on the nature of the toilet training a child experiences, he or she may become miserly (an ‘anal retentive’), if training is early and rigid, or a spendthrift (‘anal expulsive’). Now, money itself has, historically, come in a wide variety of forms. Some of these may be interpretable in psycho-analytical terms (the huge stone millstones on Yap thus imply a monumental anality) but others (cattle, woodpecker scalps) are rather harder to fit into this framework. And whilst it is true that being miserly may be partly a matter of character and disposition it can also be a reaction to particular economic circumstances. This has led more recent psycho-analytic writers (e.g. Bornemann, 1976) to doubt that the nature of money is derived from the anal character. We actually know very little about how consistent people are in their styles of economic behaviour (an issue to which we will return in Chapter 5).

The neo-Piagetian approach to money gives us rather different insights. It tells us nothing about money per se but reveals how children come to understand its use. The literature suggests that children pass through a series of stages in attaining an adult understanding of money, though the number of stages described ranges from a low of three to a high of nine. For instance, Strauss (1952) described nine categories through which children progress in their understanding of monetary meaning. These ranged from stage one (where children realised that money can somehow buy certain things) through stage four (a recognition that the shopkeeper must be paid by the customers for goods bought in order for him or her to earn money) to stage nine (where children fully understood the notion of profit). Berti and Bombi (1988), by contrast, describe four stages in children’s developing understanding of payment for work. At the first stage (4–5 years) children had no idea of the origin of money, whilst at the second, children saw the origin of money as independent from work. At stage three, children think that change given by shopkeepers is the origin of money and finally at stage four (7–8 years) children associate money with work. What is striking about this study is that it treats money as something clearly defined that children have to come to understand to function as effective economic agents. Money is seen as unproblematic (which it is not) and children’s informal behaviour is ignored. We will discuss these issues in more detail in Chapter 3.

We will conclude this section by briefly describing a different kind of developmental theory, the Eriksonian psycho-social approach. Although, to our knowledge, this has not been applied to economic issues other than the issue of treasured possessions, it does resonate with the approach we will take of focusing on the main economic problems facing people at different stages of their lives. Erikson (1963, 1982) proposed that there were eight stages of psycho-social development each of which has a prototypical developmental task and distinctive psycho-social crises that can ensue. For example, in the first stage (oral-sensory), the child has to solve the problem of establishing basic trust; in the fifth (puberty), the adolescent must resolve the problem of identity versus role-confusion; and in the sixth (young adulthood), the adult must deal with the conflict between intimacy and isolation. Erikson (1982) also identifies the core pathologies of each stage. These pathologies are not passive limitations of individuals but are active (misguided) strategies that protect them from unwanted associations. Thus the core pathology of early adolescence is isolation, whilst of early adulthood it is exclusivity. Erikson’s model is like a staircase: at each stage the achievements of the previous stage provide the resources with which to deal with the problems and challenges of the next.

Newman and Newman (1991) make extensive use of Erikson’s approach and believe that a relatively small number of tasks (quite a few of which are economic in character) dominate a person’s efforts. For instance, one of the main ways in which identity is expressed in Western society is one’s occupation, so it is not surprising that career choice is crucial in helping resolve the central question of adolescence, ‘who am I?’ Economic decisions are also important at later stages: work and lifestyle (in early adulthood) and the management of a career or household in middle adulthood.

Erikson’s approach suffers from all the normal problems of stage theories and its concepts are sometimes abstruse and difficult to operationalise. But it is valuable in identifying the main problems that people have to resolve as they progress through life, and insightful in characterising some of the stages and their associated pathologies.

Expressive/communicative

Social scientists who have focused on the social context of economic behaviour have given us a rather different perspective. Perhaps the first to do so was Veblen (1899), who introduced the idea of conspicuous consumption, the notion that rich people buy expensive goods just because they are expensive in order to signal their wealth and class. This suggests that we should try to understand the goods people buy and exchange as a system of communication, which is the approach taken by Douglas and Isherwood (1996). As they say, ‘The most general objective of the consumer can only be to construct an intelligent universe with the goods he chooses’ (Douglas an...

Table of contents

- Cover Page

- Title Page

- Copyright Page

- Preface

- Acknowledgements

- 1: An Introduction to Economic Psychology

- 2: The Early Years—The Economic Problems of Childhood

- 3: Becoming an Economic Adult

- 4: Economic Behaviour In the Family

- 5: Economic Behaviour In Maturity

- 6: The Golden Years? Economic Behaviour In Retirement

- 7: Afterword

- References

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Economic Psychology of Everyday Life by Paul Webley,Carole Burgoyne,Stephen Lea,Brian Young in PDF and/or ePUB format, as well as other popular books in Psychology & History & Theory in Psychology. We have over 1.5 million books available in our catalogue for you to explore.