![]()

Part I

Principles of economics

![]()

1 Introduction

This chapter introduces the main elements of an economic system: its agents, their decision making, and the limited availability of resources. It also argues that the use of models allows the capture of fundamental relationships among those agents in a simplified but meaningful way.

Economics is the study of the way in which economic agents make their decisions regarding the use (allocation) of scarce resources. This definition contains three concepts that must be defined to fully capture the meaning of economics. These include economic agents, scarce resources, and the decision-making mechanism.

Economic agents are the decision makers in the economy. These are individuals, households, enterprises, and the state. They make decisions on the use of the available resources by answering the following questions: (i) what to produce/consume; (ii) how much to produce/consume; (iii) how to produce/consume; and (iv) who produces/consumes.

The resources available in an economy are those goods and services used and transformed in other goods and services allocated among the agents participating in that economy. An economics problem arises only when resources are scarce, so that decisions on how to allocate them need to be taken.

A traditional taxonomy of resources classifies them in three types: land (physical resources of the planet), labor (human resources), and capital (resources created by humans to aid in production: tools, machinery, factories, etc.). Sometimes a fourth element is added under the label of enterprise. It refers to the organization of resources to produce goods and services.

The answers to the questions above depend on the organization of the economy. An economy can be centrally planned. In this case the state owns all the resources and allocates them. At the other extreme we find pure free market economies, where the allocation of resources is determined by the forces operating in the markets for goods and services without any state intervention. Most economies though combine elements of market allocation together with some state intervention. These are called mixed systems.

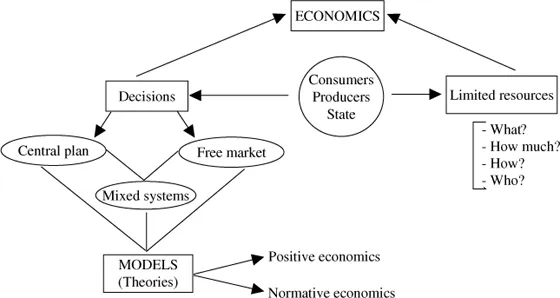

Real economies are far too complex to be studied as such. Therefore, we have to limit ourselves to use economic models (theories). An economic model is a set of assumptions providing a simplified representation of reality capturing the fundamental relationships among economic agents. To illustrate, the relation between an economic model and a real economy can be compared to the relation between a road map and the actual road network. There are two fundamental types of models according to the aim of the study. On the one hand, we find models built to describe the decision-making process and the allocation of resources. The solution to these types of models is called the equilibrium allocation of that economy. This approach avoids economic value judgments and is known as positive economics. Once an equilibrium allocation has been characterized, further questions can be brought forward. These incorporate value judgments about the equity and efficiency properties of the equilibrium allocation, and the particular policy actions that ought to be followed to achieve a desirable goal. This is the realm of normative economics, also known as welfare analysis. Figure 1.1 summarizes this.

Figure 1.1 The meaning of economics.

This first part of the book is thus devoted to presenting the content of economics. Chapters 2 and 3 contain the analysis of consumers and producers. Chapter 4 studies the interaction of consumers and producers in the market. Next, we introduce the state as an actor both intervening in the functioning of the markets in Chapter 5 and also looking at concentration of producers (Chapter 6). Finally, and with the perspective of the health care sector, Chapter 7 is devoted to the study of the (differential) behavior between for-profit and nonprofit organizations.

![]()

2 Demand

In this chapter we address the decision making of a consumer in the market. From the primitive concept of preferences over consumption goods and the budget constraint, we derive the demand system, study its properties, and aggregate the individual demands into the market demand.

In this chapter we will study the behavior of consumers. A consumer is an agent making decisions on consumption. It may be an individual, a household, a community of apartment owners in a building, etc. as long as they share a common objective. The problem of deciding what to consume and how much arises because resources are scarce. This means that the consumer faces restrictions when taking the consumption decision. We summarize these restrictions into a single one described by the income available to the consumer.

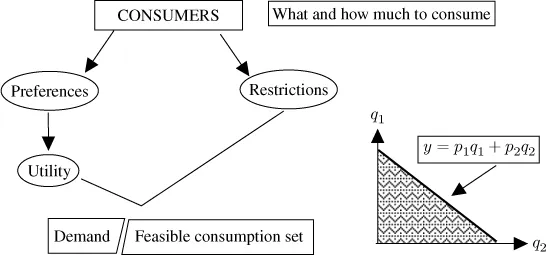

The selection of goods to consume is made among all goods that (potentially) can be found in the economy. This is the so-called consumption set. A particular combination of these goods (i.e. a point in the consumption set) is labeled as a consumption plan. To be able to select, the consumer has to be endowed with a criterion allowing for comparison of all the possible consumption plans. The capacity to compare is described by the preferences. Figure 2.1 illustrates these elements. On the left-hand side we have the set of consumers, each one endowed with preferences and submitted to restrictions. The right-hand side of the figure illustrates an example of an economy with two goods (q1 and q2),1 the consumption set (the space q1 − q2), and the restriction. This is the straight line crossing the consumption set diagonally. It represents how a certain level of income y is spent between two goods that are sold at prices p1 and p2. All points in the shaded area are feasible consumption plans, that is, bundles of goods affordable to the consumer. This is called the feasible consumption set. Formally, it is the subset of the consumption set defined by those affordable consumption plans given the consumer's income and the prices of the commodities. The particular consumption bundle chosen (given the income and prices) defines the demand of the consumer. To complete the description of the elements involved in the decision problem of the consumer it remains to introduce the utility. We will argue below that we do not have the mathematical tools to deal with preferences. Therefore, we “translate” with the tools of calculus the information given by the preferences into an index of satisfaction called utility function analytically tractable.

To summarize, the consumer must identify the consumption plan in the feasible consumption set yielding the highest possible level of satisfaction (i.e. utility). As such optimal consumption plans will be contingent on income and prices, the outcome of this decision-making process will be a function specifying for every level of income and every system of prices the utility maximizing consumption plan. This is the so-called demand function.

Figure 2.1 The consumer problem.

Before proceeding with the detailed analysis of the consumer behavior, some notation should be introduced.

In the economy the set of consumers is denoted by

I. A particular consumer is identified by

i ∈

I. A consumer

i is characterized by a vector

() where

represents consumer

i’s initial income (wealth),

denotes the consumption set, and

denotes the preferences of

i ∈

I on

Xi. A consumption plan is denoted as

qi=

(qi1, qi2)∈

Xi. Let

Xi =

X, ∀

i ∈

I. Finally, we assume that in the economy there are

l goods indexed as

k =1

,2

,..., l.

2.1 The elements of the consumer problem

To guarantee that the problem of the consumer is properly defined, we need to introduce some assumptions regarding its elements. Regarding the consumption set X, we will assume that it is non-empty, closed, and convex. Non-emptiness is required so that the consumer may select a consumption plan. The other assumptions are technical. They are...