Political risk was first introduced as a component for assessing risk not directly linked to economic factors following the flow of capital from the US to Europe after the Second World War. However, the concept has rapidly gained relevance since, with both public and private institutions developing complex methodologies designed to evaluate political risk factors and keep pace with the internationalization of trade and investment. Continued global and regional economic and political instability means a plethora of different actors today conduct a diverse range of political risk analyses and assessments. Starting from the epistemological foundations of political risk, this books bridges the gap between theory and practice, exploring operationalization and measurement issues with the support of an empirical case study on the Arab uprisings, discussing the role of expert judgment in political forecasting, and highlighting the main challenges and opportunities political risk analysts face in the wake of the digital revolution.

- 150 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Subtopic

Politics1

Political risk as a social science concept

There is nothing worse than a sharp image of a fuzzy concept.

(A. Adams, quoted by Hoffmann, 2014, p. 84)

1. A fuzzy concept

Even more than portfolio investment, FDI – especially when taking the form of greenfield investment – entails careful consideration of the possible political scenarios pertaining to a given host country: it therefore comes as no surprise that in recent years the analysis and assessment of political risk have become essential tools for executive decision-making for businesses of all sizes.1 Today, a plethora of different actors carry out PRA for investment-related purposes, from consulting firms to export credit agencies, from rating agencies to insurance companies. The diverse nature of the actors performing political risk analysis is mirrored by the diverse meanings attributed to this catchall term. Partly due to its intrinsically interdisciplinary nature, political risk as such has been neglected as a subject for study within the academic framework of political science and international relations, despite the tradition of study into the disparately defined concept of ‘political instability’. When data on political risk is gathered, elaborated and provided to multinational investors in the context of the political insurance industry, comparisons between the different political risk assessment approaches and relative indexes cannot be carried out easily for obvious reasons of competition. This explains the lack of transparency in the field, which raises questions about the logic and practice underpinning existing approaches to PRA. It must be acknowledged that, for instance, despite some interesting contributions in the last few years (see in particular Jensen, 2003, 2008), the relationship between political regimes proper and political risk remains largely unexplored.

Although risk assessment in terms of political environment has always been part of any business venture,2 the acknowledgement of political risk in economic and financial literature only dates back to the 1960s. The conceptual boundaries of political risk have always been hazy, as is corroborated by the fact that since the 1970s, the scholarship on PR has been beset by literature reviews trying to bring this ambiguous concept into focus (see for instance Kobrin, 1978; Fitzpatrick, 1983; Simon, 1984; Friedman & Kim, 1988; Chermack, 1992; Jarvis, 2008). Yet, as a first step in trying to achieve more clarity in this field, it is possible – indeed useful – to analyze the use of the term in its historical evolution. In the 1960s, when financial and economic actors began to develop country risk analysis, the political scenario worldwide was shaped by two complex and intertwining processes: the Cold War, with its inherent ideological contraposition between capitalism and socialism – that is, between free market and planned economies – and the beginning of decolonization. The likelihood of events such as the 1956 Suez crisis or the 1960 Congolese upheaval that could suddenly and drastically change the political as well as the business environment considerably increased. Political risk, however, sometimes also referred to as ‘non-economic risk’,3 was predominantly considered to be a feature of ‘underdeveloped’ or ‘modernizing’ countries (Zink, 1973; Green, 1974; Green & Korth, 1974): as Jodice puts it, first-generation political risk analysts were mostly concerned about investment disputes deriving from so-called ‘economic nationalism’: the trend, typical of developing countries, to confiscate or expropriate foreign property in the name of public interest (Jodice, 1985, p. 9). The 1970s were marked by two events, both – unsurprisingly – with a relevant impact on the business world’s perception of political risk: the 1973 oil-shock and the 1979 Iranian revolution. The occurrence of such grand-scale events highlighted the importance of political risk assessment and management, and the political risk industry began to flourish, with the proliferation of consulting firms as well as of applications for political risk coverage, provided both by public and by private insurers (Simon, 1984). The 1980s saw another shift in the implications of political risk, with a new focus on the problem of debt management by host countries.4 Since the 1990s, however, and particularly after the attacks on the World Trade Center in New York City, terrorism has become a major source of concern for international investors and has emerged as a significant form of political risk (Berry, 2010). The scope and breadth of political risk analysis has also evolved in geopolitical terms from being mostly performed by and in the interest of Western (largely American) MNEs, to becoming a truly global activity. Firms in emerging economies invest in risky markets more than their global counterparts (Satyanand, 2011), and in light of the financial (and political-economic) crisis which began in 2008, developed countries do not look as devoid of risk to foreign investors as they had in the past. Thus, political risk is no longer seen as an exclusive attribute of least developed countries (LDCs). Generally speaking, it can be said that the term political risk has come to designate a component of country risk, the latter being defined as “the ability and willingness of a country to service its financial obligations” (Hoti & McAleer, 2004, p. 1). However, it should also be noted that ‘country risk’ today commonly refers to a wider array of risks, not only financial but also operational in nature: “country risk is of a larger scale, incorporating economic and financial characteristics of the system, along with the political and social, in the same effort to forecast situations in which foreign investors will find problems in specific national environments” (Howell, 2007, p. 7).

2. Definitions

2.1 A review

In an attempt to classify the alternative technical meanings that have been attached to political risk over time, the following definitions can be identified: (1) political risk as non-economic risk (Ciarrapico, 1992; Mayer, 1985); (2) political risk as unwanted government interference with business operations (Eiteman & Stonehill, 1973; Aliber, 1975; Henisz & Zelner, 2010); (3) political risk as the probability of disruption of the operations of MNEs by political forces or events (Root, 1972; Brewers, 1981; Jodice, 1984; MIGA, 2010); (4) political risk as discontinuities in the business environment deriving from political change and which have the potential to affect the profits or the objectives of a firm (Robock, 1971; Thunell, 1977; Micallef, 1982); (5) political risk substantially equated to political instability and radical political change in the host country (Green, 1974; Thunell, 1977).5

The first definition is typical of an initial phase in which firms and banks began to address the problem of assessing risks that could not be classified as mere business risks or be evaluated by simply looking at the economic fundamentals of a country. The second definition is quite restrictive and, as noted by Kobrin (1979), has relevant normative implications because it assumes that government intervention is necessarily harmful – in other words, that host government restrictions on FDI involve economic inefficiency. This is not always true, and in PRA the objectives of companies and host governments – which may diverge as well as coincide – should be analyzed accordingly, in order not to be misled by preconception. It could be added that, in light of the debacle of the ‘Washington consensus’, and also considering the financial and economic crisis beginning in 2008 – which exposed the implicit risks in the under-regulation of markets – the concept of laissez-faire government has lost much of its appeal to business theory and practice.

The third definition is perhaps the most precise from the semantic point of view, because it rightly considers political risk not simply in terms of events but rather in terms of the likelihood of events (harmful to an MNE’s operations). If the aspect of probability calculation is overlooked, by conceptualizing political risk in terms of mere ‘events’ which can have an impact on a firm,6 one might end up behaving like the proverbial fool who, when a finger is being pointed at the moon, only looks at the finger. Political risk calculation is an intrinsically forward-looking task (on this point, see Chapter 2), and political risk may well be structurally high, and be perceived as such by a firm, even in the current absence of possibly harmful events.

The fourth category of definitions is broader, since it focuses on the business environment rather than on the individual firm. The influential definition provided by Robock (1971) deserves a closer look:

Political risk in international business exists (1) when discontinuities occur in the business environment, (2) when they are difficult to anticipate, (3) when they result from political change. To constitute a risk these changes in the business environment must have a potential for significantly affecting the profit or other goals of a particular enterprise

(p. 7)

The idea of an existing, observable discontinuity in the business environment is quite common in definitions of political risk. Once again, it is important to underscore a point: even situations which apparently look stable – and that have been so for a relatively long time – may in fact be extremely risky. The notion of latent variables in statistics effectively illustrates this concept.7 Risk can be thought of as the likelihood of a certain event taking place. What is subsequently observed is, in fact, a binary outcome: either the event does take place or it does not. The idea behind latent variables is that they are generated by an underlying propensity for a particular event (say, a general strike, a revolution or a mere act of expropriation) to occur. The political scenario in a country may look stable because it actually is stable, or, paradoxically, it can look stable in a given moment notwithstanding the fact that the political regime in force is about to collapse. A quite effective example thereof can be provided by recalling that, on December 31, 1977, President Carter famously toasted the Shah of Iran for representing “an island of stability in one of the more troubled areas of the world” (Carter, 1977). In the wake of the subsequent and unforeseen Iranian revolution and of the Soviet invasion of Afghanistan, however, PR analysts and scholars such as Brewers had to acknowledge the fact that “the past stability of an authoritarian regime should not be taken as a predictor of future stability” (Brewers, 1981, p. 8). This lesson has proved valid also for the Middle East and North Africa (MENA) countries which experienced drastic political change in the form of revolution in early 2011 (on the Arab Spring as a PR case study, see Chapter 3).

Robock also introduced a distinction that is particularly salient to this inquiry – that is, the distinction between ‘macro’ political risk (when political changes are directed at all foreign enterprises) and ‘micro’ political risk (when changes are selectively directed toward specific fields of business activity). Evidently, micro political risk assessment should be performed at industry – or even at firm – level, while, as can be seen from the present analysis, when writing about political risk in general, most authors are referring to macro political risk.

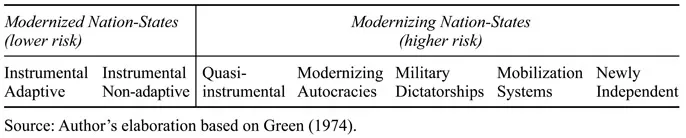

The fifth group of definitions was basically developed by authors who aimed to bridge the gap between political science and business studies, building on the extant scholarship on political change. Green’s contribution is the first to focus on the relationship between the type of political regime and political risk (Green, 1972, 1974). Seven types of regime are individuated, with an increasing level of risk (Table 1.1): Instrumental Adaptive (such as the US and UK) and Instrumental Non-adaptive (such as France and Italy), which are labeled as ‘modernized nation-states’; Quasi-instrumental (such as India and Turkey), Modernizing Autocracies (such as Syria and Jordan), Military Dictatorships (such as Burma and Libya), Mobilization Systems (such as China, Vietnam, Cuba and North Korea) and Newly Independent (such as Indonesia and Ghana), which are defined as ‘modernizing nation-states’. Green’s approach rests on a number of assumptions. The first is that radical political change is intrinsically detrimental to the activity of MNEs. The second is that the younger the political system, the less it is ‘adaptive’ to change, and thus the higher the risk of radical political change. The third is that economic modernization inevitably puts the political system under stress, and that political institutions in modernizing states must either change or be replaced. Although, as already pointed out, this analysis does focus on the origins of political risk in terms of political regime ‘structures’; it is not overly concerned with the empirical foundations of the claims made and does not delve into the specific mechanisms linking different kinds of political regime with political risk.

Table 1.1 Governmental forms and risk of radical political change

Today, more so than in the past, the task of political risk conceptualization and assessment is performed by private or public agencies (Business Environment Risk Intelligence, Control Risks, Eurasia Group, the Multilateral Investment Guarantee Agency in the World Bank Group, Oxford Analytica, Political Risk Services Group, to name but a few). As a matter of fact, most of them do not disclose – except to a very limited extent – their methodology for risk assessment, nor do they seem to agree on a precise definition of what a political risk is to the purposes of their activities. This aspect is particularly relevant because the lack of transparency in definitions and criteria for measurement is one of the reasons why the realm of political risk assessment is often hastily dismissed as a ‘soft’ science.

It is possible to draw some provisional conclusions from what has been said so far. First, despite several decades of scholarly endeavors, political risk in international business and political science seems to be affected by conceptual confusion. Second, in light of the renewed interest of scholars and practitioners of the subject, a reappraisal of political risk from the conceptual point of view seems timely. Third, no auth...

Table of contents

- Cover

- Title

- Copyright

- Dedication

- Contents

- List of tables

- List of figures

- Preface

- Acknowledgments

- Abbreviations

- Introduction

- 1 Political risk as a social science concept

- 2 Thinking about a theoretical framework

- 3 From theory to practice: a case study of the Arab Spring

- 4 Forecasting political events: issues and techniques

- 5 The cross-cutting role of expert judgment

- 6 The impact of the digital revolution on political risk analysis and assessment

- Concluding remarks

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Rethinking Political Risk by Cecilia Emma Sottilotta in PDF and/or ePUB format, as well as other popular books in Politics & International Relations & Politics. We have over 1.5 million books available in our catalogue for you to explore.