![]()

1

Introduction and Structure of the Book

Introduction

Environmental management accounting (EMA) is a concept of sustainability management which comprises a set of accounting tools and practices to support managerial decision-making on environmental and economic performance. EMA primarily supports internal decision-making; therefore, it is comparatively difficult to gather reliable information on the actual drivers, practice, state, and quantity of EMA applications in companies and other organisations.

To date, case study research on EMA has focussed mainly on single applications in large companies in industrialised countries. This research book provides new insights into the implementation of EMA through a comparative case study consisting of 12 exploratory case studies conducted in small, medium, and large companies in four emerging economy countries of South-East Asia: Indonesia, the Philippines, Thailand, and Vietnam. The study seeks to explore various decision situations and institutional settings and the way these are linked with types of EMA information, as well as the uses of, and linkages between, a large range of tools which support decision-making at different management levels and company contexts. The book analyses the applicability of EMA and its related tools contingent on the decision-making context within the company.

Motivation for this Collection of Case Studies

In 2003, InWent Capacity Building International (now GIZ Deutsche Gesellschaft für Internationale Zusammenarbeit GmbH), Germany, commissioned the Centre for Sustainability Management of Leuphana University Lüneburg, Germany, to conduct a capacity development programme on Environmental Management Accounting in South-East Asia (EMA-SEA). The programme operated from late 2003 to early 2008 and was financed by the German Federal Ministry for Economic Cooperation and Development and supported by two non-profit organisations: the previously mentioned InWent, as international coordinator, and the Asian Society for Environmental Protection, as the main regional partner for Indonesia, the Philippines, Thailand, and Vietnam. The Centre for Sustainability Management provided the programme content and conducted a series of information workshops, training seminars, internet-based seminars, and ‘training of trainers’ workshops for managers, engineers, consultants, and other business-related persons, as well as representatives from governments, local authorities, and academia in the South-East Asian region. During the project the Centre for Sustainability Management worked closely with the Centre for Accounting, Governance and Sustainability, University of South Australia.

The EMA-SEA programme aimed at developing individual and institutional EMA capacity in the region and continues in a voluntary way now that the supported part of the programme has been completed. An internal survey among the participants of EMA-SEA ‘training of trainers’ seminars revealed that about half were integrating EMA in their daily work as consultants, environmental engineers, managers, lecturers, and researchers. More than 40 cases of EMA implementation leading to substantial financial savings and environmental improvements were reported in 2006 and 2007. In those cases where the interviewees quantified savings and improvements, the average annual financial saving was about €23,100 and the average reduction in annual CO2 equivalents of 1,700 tonnes per company (the survey can be found in the downloads and links page of http://gc21.inwent.org/EMAportal).

The didactic concept of the different types of EMA seminars was based on the project casework training approach (Tharun 1995a,b). The approach combines lectures, group work, and discussion and is based on realistic examples. At the beginning of the EMA-SEA programme, the Centre for Sustainability Management developed several South-East Asian company examples to support the project casework training approach and the development of training materials. This experience strengthened the authors’ desire to conduct comprehensive research beyond the scope and duties of the EMA-SEA programme. The result of this research is manifested in this book, which introduces 12 embedded case studies as part of an overall comparative case study. The structure of the case study book is explained next.

Structure of the Book

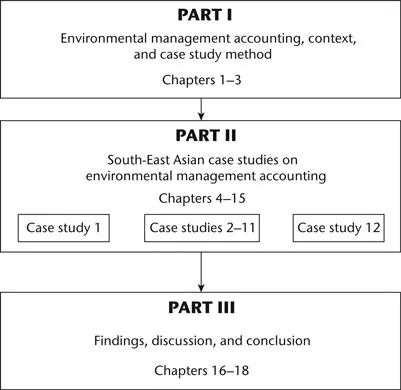

This introductory section precedes Part I of the book. Part I includes an overview of conventional and environmental accounting which constitutes the basis for EMA definition (see Figure 1.1). A framework for the characterization and systematisation of EMA decision settings and tools is then explained, followed by a description of individual EMA tools.

Figure 1.1 Structure of the book.

In the remainder of Part I, research method and design are elaborated. First, the economic and environmental importance of the South-East Asian region is described briefly. The authors then explain the usefulness of the EMA concept as well as the state of EMA implementation in the South-East Asian context. Against this background, the purpose and the methodology of the EMA study is defined, followed by a brief general introduction to case study research, reasons for conducting case studies, and types of case studies. Finally, this part of the book outlines the specific case study design for studying companies’ decision situations, institutional settings and implementation of EMA in South-East Asia and concludes with an overview of the 12 South-East Asian company case studies that constitute the comparative case study.

Part II presents each embedded case study in detail. Each of the 12 cases from Indonesia, the Philippines, Thailand, and Vietnam then forms a separate chapter in Part II.

The findings of the comparative case study are discussed in Part III of the book, which concludes with an outlook for future EMA research and implementation.

References

Tharun, G. (1995a) The project casework (PCW) concept in brief: its rationale, structure, function, development and origin in 42 Statements, Bangkok: Carl Duisberg Gesellschaft.

Tharun, G. (1995b) Training für das Management von Umweltprojekten: Fortbildungsmaßnahmen für Führungskräfte aus Wirtschaft und Verwaltung als Lösungsansatz zur Bewältigung von Umweltproblemen in Entwicklungsländern [Training for the management of environmental projects: further education for business and public administration executives on tackling environmental problems in developing countries], Frankfurt: Peter Lang.

![]()

Part I

Introduction to environmental management accounting

![]()

2

Environmental Management Accounting

Introduction to Environmental and Conventional Accounting

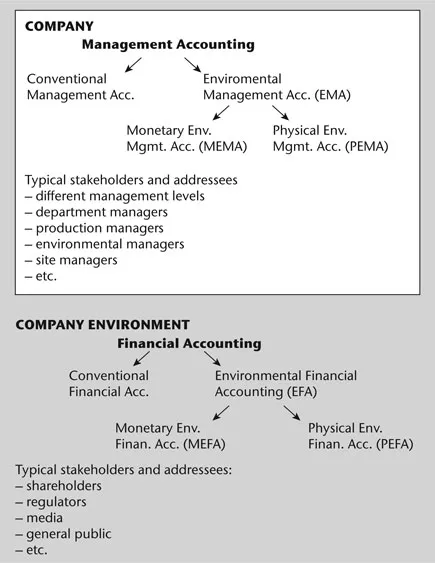

Environmental accounting is a specific type of accounting which brings together monetary and physical information to (i) provide support for decision-making by managers, and (ii) facilitate accountability through feedback from reports made to internal and external stakeholders (Burritt, Hahn, and Schaltegger 2002). Accounting supports decision-making processes. Accounting involves collecting, recording, classifying, and reporting purpose-orientated information, predominantly in monetary units, and is often based on physical information, such as items of semi-manufactured products, production schedules, or kilograms of raw materials (Schaltegger and Burritt 2000). The accounting process can also provide an important foundation for improving the environmental records of businesses, for example in relation to making transparent cost and environmental savings from the reduction of waste. The provision of monetary and physical information to management and external stakeholders about the environmental impacts of business and the financial consequences of environmentally relevant business activities is expressed by the term ‘corporate environmental accounting’ (Schaltegger and Burritt 2000).

Environmental management accounting (EMA) information is available for use by corporate decision-makers to reduce environmental impacts and enhance economic performance (Schaltegger and Müller 1997; Burritt et al. 2002; IFAC 2005; Wagner and Enzler 2006). Management may also decide to use EMA as the foundation for disclosures to external parties.

Management still has discretion in deciding which environmental issues to recognise, how to measure and what to disclose, but if the accounting system highlights the monetary benefits from certain environmentally helpful activities, no manager would be likely to refuse to take action. Environmental management during the 1990s became an increasingly important issue in financial markets, hitherto a very conservative sector of the world economy as far as environmental issues are concerned. Growth in the socially responsible investment sector adds to this momentum (Kurtz 2008). The importance of environmental accounting for other stakeholders cannot be overestimated either. Management, non-government organisations, shareholders, governments, and other groups are seeking information about the environmental risks and returns from business (Schaltegger, Burritt, and Petersen 2003) – information that environmental accounting systems are designed to capture, track, and report. In the following sections, the functions of conventional accounting and accounting processes are outlined before environmental accounting systems are introduced and differences outlined.

Accounting and Purpose-Orientated Information

To appreciate the significance of EMA it is first necessary to gain an understanding of conventional accounting and why it does not serve managers well in the context of environmental matters. Accounting fulfils a number of functions in an organisation. First, it provides feedback to stakeholders about performance: some stakeholders, such as managers, can be thought of as internal to the business, whereas others, such as shareholders and regulators, are seen as external (see Figure 2.1).

Figure 2.1 Accounting systems and stakeholders.

Accounting provides information to managers at all levels to support the decisions that they need to make. This includes decisions such as determining (i) the short-run price of their products, (ii) the mix of products and services to offer customers, and (iii) the quality of products. The making of long-run decisions is also supported by accounting information such as those about capital investment, whether to enter a market, or to close down a business, or a segment of a business.

Directors and managers are accountable to shareholders for the use of corporate resources; they have a position of stewardship over resources entrusted to them. Accounting information provides feedback to internal (e.g. employees) and external stakeholders (e.g. shareholders) about stewardship of these resources. In practice, the distinction between internal and external stakeholders is blurred as managers may own shares or share options – they have both internal and external perspectives on the business.

Second, accounting also acts as a record of organisational memory. It stores knowledge about the organisation, knowledge that can be lost completely if left to reside in the minds of people employed by the business, and knowledge that can be transferred to others in the business. Such knowledge may relate to past customers, the success or failure of products to generate value for the business, or the development of processes within the business that can help protect the environment while improving the financial bottom line. All of this knowledge can be recorded in a formal accounting system.

Finally, accounting also acts as an instrument for tracking where a business has been, where it is at present, and, through extrapolation, where it plans to be in the future (stewardship). It is, in effect, a classification, recording, and reporting device, the product of which can be used by internal and external stakeholders.

Corporate managers make decisions and act in the present, usually guided by their experience and information available to them about the past and present. The aim of their decisions and actions is to achieve objectives that are established for the future of their organisations. Such objectives are usually complex but, for commercial corporations, the pursuit of monetary gain for shareholders is a high priority, as is satisfying the requirements of other stakeholders, particularly compliance with legal requirements (e.g. health, safety and environment legislation) and economic performance. As the future is uncertain, managers need access to all relevant information obtainable at a reasonable cost about alternative courses of action available to them (Chambers 1957: 3). In this context, information provides purpose-orientated data for users, that is, information about how a desired future state might be achieved. If the desired future state relates to sustainability, then accounting has a part to play.

The Accounting Process

Accounting records data in a logical, rigorous, meticulous way in three stages. In the first stage, the main accounts are identified and classified in a chart of accounts. Second, signs, signals or characteristics of a transaction (e.g. buying raw materials, hiring labour, acquiring a factory), transformation (converting raw materials into a product, etc.), or external events (such as inflation) are recorded in chronological order, generally at the time they occur or shortly afterwards. In the third stage, the balances of each account are determined from period to period. The period may be each year, every six months, each week, day, immediately, or some other time that is useful for those people who are responsible for making decisions and accountable for the stewardship of resources.

Much consideration is given to the books of account in which records are kept, and how these are interrelated through journals and ledgers. However, as computer packages become increasingly affordable, less em...