![]()

1 Introduction

Organizations

People have organized themselves in various ways through times to survive and prosper. The picture of the lone individual on an island in Robinson Crusoe style appeals to the imagination, but is not a long term viable social construction. Division of labor in organizations has existed from early times on. Organization appears when several people assemble and live by certain rules. States and corporations are cases in point. Family and tribe constitute old organization forms. Membership of these organizations was determined at birth. This differs from organizations that people enter out of free will. People can join firms, clubs and unions and agree to accept their rules. This does not apply to political organizations like nation states and empires whose membership is usually not chosen. Organizations like business firms need permission from political authority to be founded. Human history records several periods wherein business organizations could operate within empires and states. However, periods of freedom of organization were alternated by periods wherein the state increased its economic authority. State enterprise has been the norm in many times and places. A central role of the state fits in with ideas that there is only one best way to organize economic life. However, state organizations possessing monopoly power led to stagnation in many parts of the world.

Human political organization has taken many forms: from tribes to kingdoms and empires; from city states to nation states and international alliances. Many empires and nation states wanted to appropriate surpluses from subjugated people in imperial fashion. The concept of empire is defined as the permanent rule and exploitation of defeated people by a conquering power (Parsons 2010, 4). Empire wherein one group’s military power allows it to exploit others creates an insurmountable gap between conquerors and subjects. Empire means control of (foreign) people. It differs from colonization that refers to the permanent settlement of people in foreign lands. The two concepts merged when empires founded colonies on conquered lands. But Parsons argues that colonies that did not want to exploit indigenous people were not imperial (Parsons 2010, 10). Ancient Greek city states founded colonies along the Mediterranean. The same applies to Italian city states like Venice and Genoa. The colonies of these maritime city states were used as trading posts. They became imperial when they started to exploit inhabitants. Many empires were stagnant organizations that wanted to preserve the past and closed themselves off from the outer world.

Business organizations prosper in political environments that allow them some autonomy to set their own rules. All organizations set rules that regulate human behavior. But freedom of organization allows people to found their own organization or choose an organization of their liking. Market economies that feature freedom of organization allow firms to appropriate surpluses. This differs from surplus appropriation by a state bureaucracy. Markets work well if competition among firms limits profits below monopoly levels. Profits would just suffice to pay ‘normal’ rates of return on investment in market equilibrium.

Long term economic growth

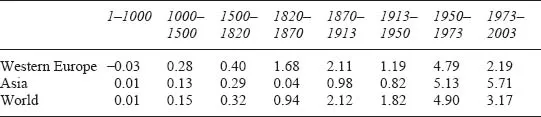

Organization theorists like Max Weber have focused on the importance of organizations and institutions for economic growth (Weber 1978). Economists have focused on quantifiable data relating to production factors and productivity to measure economic growth. Economists assume economic growth to be a natural phenomenon that spreads through the diffusion of knowledge. They have developed economic theories to explain movements of the economy at large. Economic growth models explain long term movements and business cycle models explain short term gyrations around an upward trend. However, real life developments do not fit economic models well. Business cycles do not fit a regular pattern. Macro economic models assume long term economic growth of 2 percent per annum. However, this assumption is not corroborated by economic history. Looking far back in the past makes us conclude that stagnation has been the norm for the larger part of human history. This transpires from Angus Madd-ison’s path breaking work on economic development from year 1 until the present (Maddison 2007b).

We are accustomed to growth of 2 percent or more in the post World War II era. However, the first thousand years AD did not show economic growth at all. Western Europe even declined in the first millennium at an annual rate of 0.03 percent. The world at large was stagnant from AD 1 until 1000. Maddison attributes the decline of Western Europe in the first millennium AD to the breakup of the Roman Empire. A fragmented, fragile and unstable polity emerged out of the ruins of the Roman Empire. Urban civilization disappeared and was replaced by self sufficient, relatively isolated rural communities, where a feudal elite extracted an income from a servile peasantry (Maddison 2007b, 77). Trading links between Western Europe, Africa and Asia disappeared.

The late medieval resurgence of Western Europe came with the rise of organizations like cities, monasteries and universities. The first university was built in Bologna in 1080. Europe counted 70 universities by 1500. Learning got a boost from the invention of the printing press by Gutenberg in 1455. The growth of organizations with some autonomy to set rules of their own increased competition among cities, universities and monastic orders. People were no longer tied to their place of birth, but became mobile. This differed from feudalism that lacked competition and mobility.

But economic growth appeared at a snail’s pace until 1870. Growth in Western Europe from 1000 until 1500 was at 0.28 percent per annum. The rest of the world grew by 0.15 percent per year in that period. Economic growth accelerated somewhat from 1500 to 1820, but only really took off after 1820. The first half of the twentieth century showed a slowdown due to two world wars and the Great Depression of the 1930s. The 1950–1973 era was a period of rapid growth. The 1970s were a period of economic stagnation, but growth reappeared in the 1980s, especially in Asia (see Table 1.1).

Table 1.1 shows that stagnation has been the norm for the larger part of human history. Moreover, periods of high growth did not persist, but were followed by periods of slow growth. The human potential to increase productivity has been left unutilized for large periods of time. Economists talk about production factors: labor, capital and natural resources (including land). Economic growth emanates from increases of production factors and from productivity increases of these factors. Population growth increases labor supply; labor productivity increases, if a worker produces more per hour. The production factor land increases, if more land becomes eligible for cultivation. Land productivity increases, when more is produced per acre.

Table 1.2 shows that population growth has skyrocketed in the last two centuries. The size of the earth has not increased, but our planet is now inhabited by many more people than at the beginning of our era. World population has increased by more than 30 fold from 226 million in year 1 to its present size of seven billion. The larger part of the increase of world population occurred after 1820. Populations in some regions increased faster than in others. Western Europe showed a relative population decline after 1870. The Western European population increased from 188 to 395 million, while world population grew from 1.27 to 6.3 billion from 1870 to 2003. The population of the US grew, by contrast, at a rapid rate from 40 million in 1870 to 290 million in 2003. Latin America also experienced a rapid population increase. Its population grew from 40.4 million in 1820 to 541 million in 2003.

Economic growth and population growth are closely related. An increasing population needs to be fed, clothed and housed. Production needs at least to keep pace with population growth to prevent income per head from dropping, if populations increase in numbers. People are better off if real economic growth exceeds population growth.

Table 1.1 Long term economic growth 1–2003, annual percentages

Source: Maddison (2007, 380).

Table 1.2 Long term population growth (millions)

Source: Maddison (2007, 376).

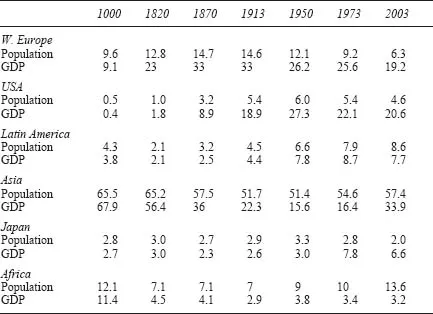

We can compare rates of economic and population growth of regions by comparing changes in their shares of world population and world income (see Table 1.3). Income is measured as real Gross Domestic Product (GDP): the total value of all goods and services produced in a year in a region at constant prices. Regions with relative rapid population growth increase their share of world population. They must increase their share of world income proportionally to keep relative real incomes at the same level.

Table 1.3 shows that per capita incomes did not differ much around the world in AD 1000. However, per capita incomes in Western Europe and the US grew much more rapidly than in the rest of the world. As a consequence, Western Europe and US income levels were almost twice that of world income in 1820. This relative increase occurred at the expense of a relative decline of real incomes in Asia and Africa. Asia had the highest population share and the highest per capita income of the world in AD 1000. However, Asians’ relative income declined and inhabitants of Western Europe became more prosperous than Asians around 1400 (Madison 2007, 309).

We can conclude that the world awoke out of its productivity slumber around AD 1000 and has moved ahead in both numbers and wealth since then. Western Europe took the lead in growth from 1000 until 1820, after which date the US took over. Asia and Japan were the most rapidly developing regions after 1950.

No clear relationship between population and economic growth can be detected from the tables. We can observe a positive relationship between population and GDP share for Western Europe from 1000 until 1870. GDP share grew at a more rapid rate than population share indicating that both population and per capita income grew faster in Western Europe than in the rest of the world in that period. The positive relationship between relative population and income growth disappeared during the twentieth century. Western Europe, the US and Japan saw their population share decline.

Western European population showed a relative decline after 1913 as did its share of world income. The two world wars curbed European population growth and destroyed its productive apparatus. The US overtook in the first half of the twentieth century. The US has maintained its leading position with respect to income per head since 1870. US productivity grew faster than Western European productivity from 1820 until 1950. But Western European productivity caught up after 1950, which closed the productivity gap that had been created between the two regions to some extent. Western Europeans were 2.16 times as affluent as the average world person in 1950 and three times as affluent in 2003. US citizens were 4.5 times as affluent as the average person in both 1950 and 2003. Japan caught up after the World War II period. The average Japanese was 3.3 times as affluent as the average world person in 2003. Asia caught up slowly with the rest of the world after 1950. The average Asian was 0.3 times as affluent as the average person in 1950 and 0.6 times as affluent in 2003. Asian population share increased after 1950.

Table 1.3 Regional shares of world population and world GDP 1000–2003 (percentages)

Source: Maddison (2007, 378, 381).

However, a negative relationship between relative population and income growth can be detected for Africa after 1950 and for Latin America after 1973. People in these regions became relatively more numerous but poorer in the last decades.

Economic growth and economic theory

The irregular pattern of growth in time and across regions has evoked several theories that want to explain economic growth. We can distinguish between economic growth models and institutional growth theories. Economic growth models explain growth quantitatively by pointing at increased uses of labor, capital and natural resources. Growth generated by an increased use of these production factors is called extensive. The use of production factors increases, but their productivity remains constant. Productivity increase causes intensive growth. Total growth is caused by the sum of extensive and intensive growth. Land is often considered to limit extensive economic growth. Land cannot easily be expanded other than by the cultivation of yet untilled areas. The presence of a limiting factor like land stops population growth in its tracks, if land productivity does not increase. People need to be fed and population can only grow if more food is produced. This can only be achieved by increasing the area of cultivated land, if productivity is constant. This situation is often described as the Malthusian trap: saying that populations will stagnate. A surplus of births above deceases is removed by famines and diseases in the absence of productivity growth.

Intensive economic growth is achieved, if productivity of land, labor and natural resources increases. But economic theory cannot easily explain productivity growth. Economics has obtained its label as the dismal science, because it is the discipline that teaches how (relative) scarcity determines prices of production factors and their share of GDP. Land scarcity was the theme of classical economic theories put forward by Malthus, Ricardo and others. They explained how land rents accrued to land owners. Marx made capital the scarce factor that would appropriate increasing shares of national product. Labor was assumed to be present in abundance in those theories due to the human proclivity to procreate. However, modern economic theory has stressed human capital as a scarce factor.

Relative scarcity of a single production factor can affect the distribution of GDP over owners of natural resources, land, capital and labor. However, productivity growth that elevates the output level of all production factors overcomes scarcity. Shares of GDP accruing from natural resources, capital and labor can remain constant, if productivity of all production factors increases at the same rate. More food is grown on the same piece of land; workers produce more per day and a certain amount of capital generates more profits, if factor productivity increases proportionally.

The next question is where does productivity increase come from? Economic theory says that it comes from technological progress and science. Institutional economists argue that productivity growth emanates from ‘good’ institutions. Protection of (intellectual) property rights, the absence of corruption, an independent judiciary and the rule of law are examples of good institutions that promote investment and growth. I tend to side with those economists that stress the significance of good institutions for productivity growth (Brouwer 2011). Good institutions enable markets to do their work of allocating capital and labor and distributing the proceeds among production factors. Theft would be the norm in the absence of property rights. Corruption would be the norm in non-civil society.

The alleged superiority of market operations has been questioned on a regular basis and even more so after the recent financial crises. The adversaries of market allocation point to the anarchic character of free markets. Textbook models of market competition are the targets of their critique. Workers are assumed to appear at the gate of the farm one at a time to look for a job. Each successive worker is less productive, because he works on a fixed amount of land with a fixed amount of capital at his disposal. Hiring stops when the value of the produce of the last worker equals his wage. Abundant supply reduces price. This applies to labor markets and also to product markets. Good harvests reduce the price of wheat, while bad harvests increase it. Markets and prices are assumed to be ruled by factors like birth rates and weather conditions that are not under the control of business firms, but are regulated by the invisible hand of supply and demand. But markets cannot exist without rules. Employers can exploit workers by paying them below market wages. Products sold on markets and fairs can be of low quality and money coins can be debased. Property can be robbed by force. The idea of an abstract market that exists within an institutional vacuum does not correspond with reality. The merchants of cities like Venice and Amsterdam that prospered on trade lived by rules made by city government and chambers of commerce. A market without rules is a jungle, where the power of the strongest prevails. Organizations have, therefore, established rules to make markets work. The quality of rules, however, varies among places and over time. The institutions established by successful cities and nations were copied by those who caught up with them. Dutch cities dug canals and established exchanges in imitation of Northern Italian maritime cities. But institutional development stopped when government established monopolies of trade and commerce in the seventeenth and eighteenth century (Brouwer 2008, ch. 4). Institutional and organizational freedom was sacrificed to increase state control at several times and places. Freedom of expression was limited to suppress dissent. Freedom of organization was curbed to mute discourse and mobility. Authority was laid in the hands of powerful elites. This differs from commercial city states that had democratic forms of government and systems of discourse. Judicial systems in democracies have rules for a discourse among prosecution and defense. Labor relations determine the character of discourse among unions and management. Company c...