- 272 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Advanced Fixed Income Analysis

About this book

Each new chapter of the Second Edition covers an aspect of the fixed income market that has become relevant to investors but is not covered at an advanced level in existing textbooks. This is material that is pertinent to the investment decisions but is not freely available to those not originating the products. Professor Choudhry's method is to place ideas into contexts in order to keep them from becoming too theoretical. While the level of mathematical sophistication is both high and specialized, he includes a brief introduction to the key mathematical concepts. This is a book on the financial markets, not mathematics, and he provides few derivations and fewer proofs. He draws on both his personal experience as well as his own research to bring together subjects of practical importance to bond market investors and analysts.- Presents practitioner-level theories and applications, never available in textbooks- Focuses on financial markets, not mathematics- Covers relative value investing, returns analysis, and risk estimation

Tools to learn more effectively

Saving Books

Keyword Search

Annotating Text

Listen to it instead

Information

Chapter 1

Asset-Swap Spreads and Relative Value Analysis

Abstract

The Interest-Rate Swap have become an important reference for the bond market. This type of derivate contract typically exchanges a fixed rate interest payment to the floating one, and represents a fundamental tool in terms of hedging, speculation and managing risk. This chapter illustrates the concept of asset-spread analysis for trading issue, including the comparison with the Z-spread measure. Moreover the chapter provides an industry bond analysis using Bloomberg’s screen.

Keywords

Asset-swap spread

Z-spread

Relative value analysis

Industry bond analysis

Credit-default swap

Readers will be familiar with the basics of bond market instruments. We begin this book with a look at the use of asset swaps (ASW) and ASW spreads to determine relative value in a risky bond. Such analysis is a key part of the security selection decision. ASW spreads have been long in use in the market because the interest-rate swap (IRS) is an important reference for the bond market and is used to hedge the IR risk of bonds. This type of derivate contract typically exchanges a fixed rate interest payment to the floating one, and represents a fundamental tool in terms of hedging, speculation and managing risk. The spread between swap and bonds can be used to determine the relative value of the bond, but can be measured in several ways. It is, therefore, important to know which method is being used and quoted. Once known, the spread is taken to indicate the richness or cheapness of bonds with different features.

1.1 Asset-Swap Spread

The asset swap is an agreement that allows investors to exchange or swap future cash flows generated by an asset, usually fixed rates to floating rates. It is essentially a combination of a fixed coupon bond and an IRS. We define it thus:

An asset swap is a synthetically created structure combining a fixed coupon bond with a fixed-floating IRS, which then transforms the bond’s swap fixed rate payments to floating rate. The investor retains the original credit exposure to the fixed rate bond. The pricing of asset swaps is therefore driven by the credit quality of the bond issuer and the size of any potential loss following issuer default.

A bond’s swap spread is a measure of the credit risk of a bond relative to the interest-rate swap market. Because the swap is traded by banks, or interbank market, the credit risk of the bond over the interest-rate swap is given by its spread over the IRS. In essence, then the IRS represents the credit risk of the interbank market. If an issuer has a credit rating superior to that of the interbank market, the spread will be below the IRS level rather than above it.

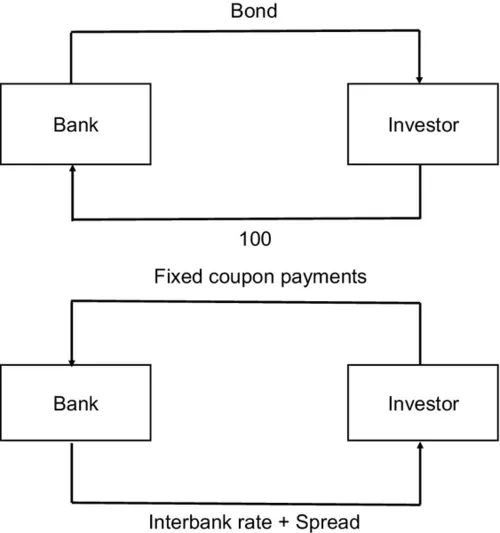

The spread of the floating coupon over the bond’s market price, that is the asset-swap value is the difference between the bond’s market price and par. The package of the asset swap is structured in two phases:

• At issue, the investor pays the asset (cash bond) at par;

• At the same time, the investor enters in the swap contract, paying fixed cash flows equal to the coupon payment and receiving a fixed spread over the interbank rate, that is the asset-swap spread. Figure 1.1 shows the asset-swap mechanism.

Figure 1.1 Asset-swap mechanism.

The zero-coupon curve is used in the asset-swap analysis, in which the curve is derived from the swap curve. Then, the asset-swap spread is the spread that allows us to receive the equivalence between the present value of cash flows and the current market price of the bond.

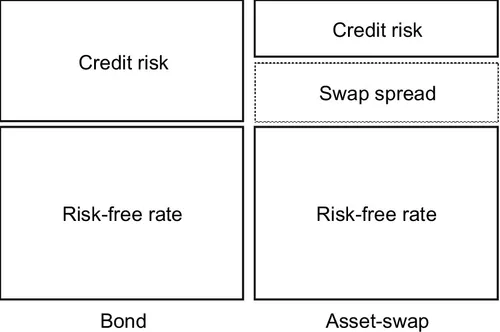

In an asset-swap contract, the investor assumes the credit risk of the bond. In case the bond defaults, the investor will continue to pay the swap, without receiving the coupons and the redemption value at maturity. Therefore, the buyer of the bond takes the default exposure of the bonds. Figure 1.2 illustrates the bond’s yield decomposition.

Figure 1.2 Bond’s yield decomposition and relative ASW spread.

1.2 Swap Spread for Richness and Cheapness Analysis

Making comparison between bonds could be difficult and several aspects must be considered. One of these is the bond’s maturity. For instance, we know that the yield for a bond that matures in 10 years is not the same compared to the one that matures in 30 years. Therefore, it is important to have a reference yield curve and smooth that for comparison purposes. However, there are other features that affect the bond’s comparison such as coupon size and structure, liquidity, embedded options and others. These other features increase the curve fitting and the bond’s comparison analysis. In this case, the swap curve represents an objective tool to understand the richness and c...

Table of contents

- Cover image

- Title page

- Table of Contents

- Copyright

- Dedication

- About the Authors

- Preface

- Preface to the First Edition (published 2004)

- Chapter 1: Asset-Swap Spreads and Relative Value Analysis

- Chapter 2: The Dynamics of Asset Prices

- Chapter 3: Interest-Rate Models I

- Chapter 4: Interest-Rate Models II

- Chapter 5: Fitting the Term Structure

- Chapter 6: Advanced Analytics for Index-Linked Bonds

- Chapter 7: Analysing the Long-Bond Yield

- Chapter 8: The Default Risk of Corporate Bonds

- Chapter 9: Convertible Securities: Analysis and Valuation

- Chapter 10: Floating-Rate Notes

- Chapter 11: Bonds with Embedded Options

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Advanced Fixed Income Analysis by Moorad Choudhry,Michele Lizzio in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over one million books available in our catalogue for you to explore.