![]()

1

Philanthropic Endeavors, Saving Behavior, and Bourgeois Virtues

RICHARD SUTCH

Economic change in all periods depends, more than most economists think, on what people believe.

JOEL MOKYR1

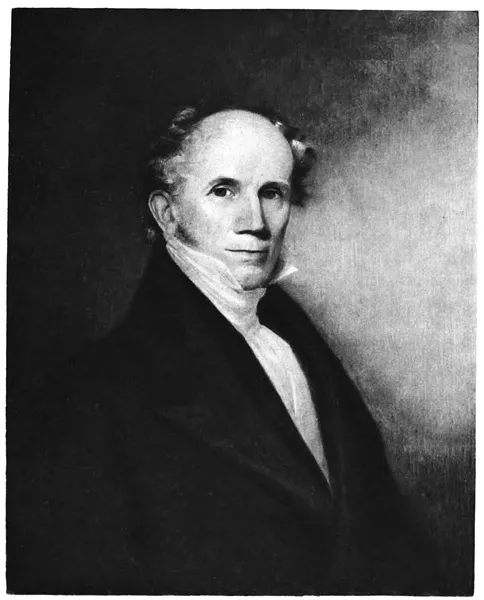

In 1816, near the end of November, Condy Raguet, the president of a fledgling insurance company and a newly elected Pennsylvania state representative, encountered his friend Richard Peters at the southeast corner of Fourth and Chestnut near Philadelphia’s Carpenters’ Hall. Raguet had recently received reports from England on the operation of several savings banks. These newly created Scottish and English banks provided a philanthropic service to the laboring class.2 With the subject fresh on his mind, he “immediately,” by his own account, asked his friend to join with him to establish a similar institution in Philadelphia.

It was probably unseasonably cold. Philadelphia is always cold in late November. But that particular November was “indeed a cold blustering month, and there [were] rain storms and snow storms; cold north-west and north-east winds, . . . froze very hard several nights, and some days were cold enough to sit by a good fire” (Peirce 1847, 220–21).3 In person, Raguet was tall, slender, and according to an acquaintance, “remarkably straight, with much of a military air . . . and was always dignified in his deportment” (quoted in Camurça 1988, 181).

Peters and Raguet walked together eagerly discussing the idea when they met Clement Biddle and Thomas Hale in the financial district. They too joined in support of the proposal. Mr. Raguet was a man of local repute, and it was not difficult for him to recruit eight additional men of prominence as trustees. He was also a man of resolve. Only a few days later, an organizational meeting was held, and soon after, on December 2—less than two weeks since his chance encounter with Peters—the Philadelphia Savings Fund Society opened its doors for business. It was the first savings bank established in the United States.

A local newspaper published the society’s objectives:

To promote economy and the practice of saving amongst the poor and laboring classes of the community—to assist them in the accumulation of property that they may possess the means of support during sickness or old age—and to render them in a great degree independent of the bounty of others—is a duty incumbent upon all, who by their services or advice have it in their power to effect so desirable an end. . . . [Our] design is to afford a secure and profitable mode of investment for small sums (returnable at the will of the depositor on a short notice) to mechanics, tradesmen, laborers, servants and others who have no friends competent or sufficiently interested in their welfare, to advise and assist them, in the care and employment of their earnings.4

The reason for saving presumed by Raguet and his compatriots was to provide “support during sickness or old age.” That same motive has remained the primary objective for saving and wealth accumulation for at least the next two hundred years. From today’s perspective, we might add a few other provisions for the future—saving for children’s education, saving for a down payment on a home, saving to leave an inheritance—but why we save is straightforward. We save today, consuming less than we might, so that we can consume more than we earn at some point in the future.

It might seem, then, that there is nothing very remarkable about the aims of the Philadelphia Saving Fund Society. Yet what is curious about this story of America’s first savings bank might not be obvious to modern readers. Saving—putting aside some portion of current income for protection against whatever the future might bring—was a novel concept at the time. Saving was not commonly mentioned in letters and diaries originating from the newly independent states of America—that is, “saving” in the sense of saving money. There were plenty of references to saving lives, saving souls, and saving seed.5

“Thrift” would be a word more frequently encountered, but its sense at that time did not suggest the act of saving money. Thrift was a moral virtue: the virtue of frugality. Frugality, moreover, was part of an ethical package, bundled with other bourgeois virtues: honesty, hard work, charity, sobriety, stewardship, and the like (McCloskey 2006). Saving money was not the object of frugality. The frugal person would avoid extravagance, minimize waste, and improve efficiency. The fruit of this parsimony need not be the accumulation of wealth; the practice of thrift was advocated to increase the individual’s capacity for charitable deeds. The English cleric John Wesley, whose ministry was the founding inspiration for the Methodist movement, gave a sermon in 1744 on stewardship titled “On the Use of Money,” which contained the catchphrase “Gain all you can, save all you can, give all you can.” With “save all you can,” Wesley challenged his listeners to live frugally. Avoid “elegant epicurism. . . . Despise delicacy and variety.” Do not waste money on “superfluous or expensive apparel, or by needless ornaments. Waste no part of it in curiously adorning your houses; in superfluous or expensive furniture; in costly pictures, painting, gilding, books; in elegant rather than useful gardens.” Do not “throw away money upon your children. . . . Do not leave it to them to throw away.” If there is a surplus, “give to the poor.” Do “good to them that are of the household of faith” (Wesley 1872). The goal of frugality was to demonstrate the ability to discipline oneself by the use of reason.

When he set out to promote “the practice of saving,” Condy Raguet used the word “saving” in a different, modern sense: setting aside some portion of earnings for future use. In 1816, that was a rather novel definition. Noah Webster’s Compendious Dictionary of 1806, with “the definitions of many words amended and improved,” recorded these definitions:

Saving, a[djective]. frugal, careful, near, excepting.

Save, v[erb]. to preserve from danger or ruin, rescue, lay up, keep frugally, spare, except.

and

Frugal, a[djective]. thrifty, sparing careful, saving of expense without meanness.

Webster’s 1828 edition was more expansive and explicitly a compendium of American English. It recorded five definitions, but not Mr. Raguet’s:

1. Preserving from evil or destruction; hindering from waste or loss; sparing; taking or using in time.

2. Excepting.

3. Frugal; not lavish; avoiding unnecessary expenses; economical; parsimonious. But it implies less rigorous economy than parsimonious; as a saving husbandman or housekeeper.

4. That saves in returns or receipts the principal or sum employed or expended; that incurs no loss, though not gainful; as a saving bargain. The ship has made a saving voyage.

5. That secures everlasting salvation; as saving grace.

Saving was not often mentioned outside of the few cities of the time because it was not a primary concern for early American farmers. Most Americans were not “mechanics, tradesmen, laborers, or servants”—the clients the Philadelphia Saving Fund Society reached out to assist. Around that time, approximately 82 percent of the white (nonslave) population lived in rural areas and were directly engaged in agriculture. More to the point, the great bulk of the farms they resided on were self-sufficient, owner-occupied, family enterprises. Aside from the tobacco plantations operated with slave labor in Virginia and further south, most agricultural production was still small-scale and intended to meet the needs of local consumers and not for export to distant markets. The farmer’s income consisted of the physical product of the family’s labor, and very little if any was sold for coin. Barter was the usual means of exchange, and the goods received in return were more often than not intended for immediate consumption. Apart from saving seed and storing grain, saving for the future was not common among American farmers. Their future was taken care of in another way. Family members, particularly grown children, were obligated by custom and law to provide support in sickness and also to give relief from the infirmities of old age. If that protection failed, neighbors might step forward to help. “Give to the poor,” John Wesley advised the community.

Saving seed and storing grain are examples of prudence that require careful frugality. Such activities sustained the agricultural enterprise and preserved the farm from danger or ruin in the following year. Deirdre McCloskey properly describes this behavior as “necessary thrift” (McCloskey and Nash 1984; McCloskey 2011, 64–65). But this “desperate saving,” as she describes it, is not saving as an economist would have it. Saving is technically defined as disposable income minus consumption (Sutch 2006, 287). But if saving and storing seed is compelled by the command of nature, the value of the grain saved must be subtracted from gross income (just like taxes paid are subtracted) to arrive at disposable income. Disposable income is what the income earner has left over (after taxes, fines, and other obligatory dues—including saved seed) to consume or accumulate as he or she wishes.

But the fact of the matter is that most Americans did not accumulate. Most didn’t need to save. The few who did save might have had no easy means beyond hoarding to do so. And hoarding cash—say, in a sock or a hole in the ground—was considered sinful.6 In the Gospel of Matthew, Jesus relates the Parable of the Talents (Matthew 25:14–30). A master berates his servant who had hidden his master’s talent (a unit of money), which was given to him for safekeeping, in a hole: “You wicked and slothful servant. . . . You ought . . . to have deposited my money with the bankers, and at my coming I should have received back my own with interest. . . . Throw out the unprofitable servant into the outer darkness, where there will be weeping and gnashing of teeth” (Matthew 25:24–30, emphasis supplied).

Those of European descent in America before the nineteenth century invested in their economy but rarely invested at a distance or earned interest. Land was cleared, homes and outbuildings were erected, walls and fences and wagon roads were engineered and built with the exercise of a great amount of hard labor. As a consequence, the land was made more productive. To gain that advantage, some consumption was sacrificed as the labor devoted to farm building was diverted from the production of crops, hunting and fishing, and other activities required to provision the farm family. Yet the growth in output that can be attributed to these kinds of intimate investments would be approximately matched by the growth in the population. Virgin land would not need to be cleared; new farms would not need to be built, except to provide for a growing population. If output grows only as fast as population, per capita output remains unchanged.

Just because saving money was rare in this world does not mean that there was no wealth. In agrarian America, most wealth was land and the permanent improvements on the land. And some landowners were wealthier than others. Indeed, if you owned enough land, you could join the landed gentry, rent to others, and live off the rents without the trouble of engaging in hard labor yourself, like the eighteenth-century English aristocrats portrayed in BBC costume dramas. But whether you were a small farmer or an aristocrat, your objective would be to preserve what wealth you owned and ultimately to pass it on to your heirs. In this world, most wealth was inherited (or appropriated from the aboriginal population with or without the color of law). If asked to explain your wealth, your probable answer would be that you were born into a wealthy family.

Raguet was wealthy by the standards of both his time and ours.7 He had inherited from his French-born father, Claudius, who had amassed a fortune first as a privateer during the Revolution and then as a ship owner involved in the lucrative carrying trade across the Atlantic. Condy Raguet established himself as an independent merchant at age twenty-two. Six years later, he built a “mansion” on Chestnut Street. He owned land in rural Pennsylvania and Virginia. He was a successful merchant and private banker (Camurça 1998, 47–56, 308–13).

Even before his inspiration to establish a savings bank, Raguet had become interested in the problem of the insecurity of old age and the power of compound interest. With some experience in underwriting marine insurance, he interested himself in working out the principles of life annuities. It is probable that he was one of the private underwriters who organized the Pennsylvania Company for the Insurances on Lives and Granting Annuities, the first life insurance company in North America (Murphy 2010, 1–2). In any case, he was an early director. The company was granted a charter in March of 1812 just as the tensions that preceded the declaration of war against the United Kingdom made ocean travelers and wealthy Americans reluctant to purchase insurance from English underwriters.

The insurance business got under way in 1814 after a public address was published (Yorke et al. 1814). As a director of the company, Raguet was a signer of t...