Managing the New Bank Technology is a practical action-oriented guide for bank CEOs, executives, business students, and boards. The book is aimed at educating those involved in banking on the key technological issues facing the industry. "Quick reference" guides opening each chapter are a special feature of the book, blueprints that offer bottom line summary suggestions for bank officers and executives. Topics include: Banking as Retailing; The Internet and Financial Services; Strategies for Future Payment Systems; Risk Management Technology; Protecting Technology Investments in an Age of Rapid Change; Negotiating Outsourcing Contracts; Developing an Information System Plan; Organizational Strategies to Manage Technology; Battling Fraud and Security Issues; and Selling Your Bank's Technology Vision.

eBook - ePub

Managing the New Bank Technology

An Executive Blueprint for the Future

- 312 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

CHAPTER 1

Making Banking Technology Spending Pay: Key Success Factors

Kevin J. Merz

Joseph Rosen

Enterprise Technology Corporation

Joseph Rosen

Enterprise Technology Corporation

INTRODUCTION

This chapter presents our view of the key factors for success and failure, gleaned from more than four decades of combined financial technology experience, in exploiting information technology for competitive advantage in the banking industry at large. We address the fundamental question of why some banking institutions consistently "do their systems right" while others time and again fail, often endangering their firms' very existence in the process. The most vital element—on which all else depends—is senior management commitment and support. Management issues addressed also include organizational culture and structure, the "bells and whistles" syndrome, the proper integration of business and IT planning, and the critical importance of having the right people.

The chapter is organized into two major parts, rirst we review the environment: spending, return on investment, and strategic importance. Next we discuss a number of brief case studies to illustrate our key lessons. We conclude with a summary and checklist of the key success factors for exploiting technology in banking.

BANKING TECHNOLOGY ENVIRONMENT

Spending

To say that the banking industry is information-technology intensive is an understatement. Many billions of dollars are spent annually by financial institutions worldwide in support of their IT needs. In addition, quite a few firms already exceed $1 billion each in total spending on IT.

How unfortunate, then, that so many firms have so little to show after spending so much money (and let us not forget time, an equally scarce and valuable resource). Exactly how much effort is wasted is very difficult to estimate, even though we all know of nightmare scenarios of projects that have ended as awful failures.

Black Holes and Blunders

Suffice it to say, for various reasons an unacceptably large percentage of the resources expended on information systems by all manner of banking organizations seems to disappear into a veritable black hole. Fortunately, some ill-conceived systems are canceled in midstream or sooner and never see the light of day.

Worse still are completed systems that are never used, either because they do the wrong thing right or visa versa. Most distressing of all are those defective systems that somehow sneak through testing by the firm's "Quality Assurance" staff and then proceed to show off their pernicious bugs at the most inopportune moments.

At best, these programming and/or design flaws are annoying or embarrassing. In some instances the costs are quite a bit dearer, both in dollars and tenure. Consider the cases of two U.S. investment banks that were prominent in the mortgage-backed securities market. Design flaws in their allocation and deal capture systems, respectively, led to hundreds of millions of dollars in losses and redundancies at both firms.

Why do such annoying and sometimes costly glitches occur so frequently, and so often to the same firms? And conversely, how do others time and again manage to "do their systems right"? What can the unlucky majority do to emulate the fortunate ones?

On a more fundamental level, why do so many IT projects fail, and among financial institutions in particular? The answer may have less to do with technology per se and more to do with management, or a lack thereof. The business press appears to be catching on to this phenomenon. "Management Attitudes Are More Important Than Technology," read the headline of a Financial Times survey on computers in finance. The subtitle of the main article pointed out the major issue even more clearly: "While the fiercely competitive financial services industry is increasing its spending on information technology, it frequently fails to achieve the full benefits."

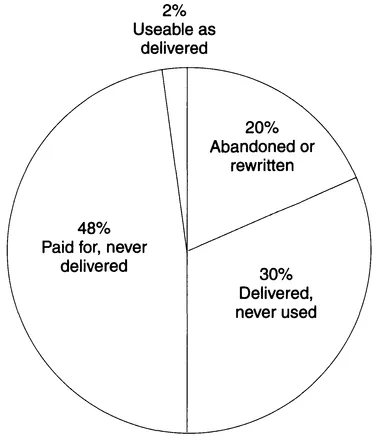

Another article, in the weekly ComputerWorld, noted widespread communication gaps between CEOs and CIOs and suggested a new approach to deployment of IT. The findings of a study on U.S. government software projects conducted several years back by the General Accounting Office (GAO) arm of Congress are especially illuminating and relevant here. The study underscores the need to reexamine how we manage IT. Exhibit 1 illustrates the survey results.

According to the GAO, 48% of government software projects are paid for but never delivered; 30% are delivered but never used; 20% are completely abandoned or rewritten; and all of 2% are usable as delivered.

Sections to follow will address these questions about IT success and failure by example, in primer fashion—a "recipe for success" (but not a cookbook, which would require considerably more space). We will present our view of the key factors for success and failure, based on our financial technology experience with financial organizations of all sizes and shapes: public and private; retail and institutional; American and foreign; and dealing in most types of investment products.

Strategic Importance

EXHIBIT 1. U.S. Government Software Projects: Are We This Bad Too?

Sources: Financial Times, Sloan Management Review.

Let us be clear that this is rio mere academic exercise. On the contrary, IT is growing in strategic importance as well as in costs. Furthermore, one would expect this to continue, if not accelerate, considering increasing global competition and the nascent integration of financial markets worldwide, both electronically and via regulation. Financial institutions are also increasingly dependent on IT because of the growing complexity of investment products and the need to manage their associated risks.

As industry observers with a sense of history understand very well, firms that fall too far behind in the IT race stand to lose much more than their competitive advantage. One need only recall the demise of many distinguished, old-line investment banking firms during the "Back-Office Crunch" of the 70s, mostly because their trade-processing systems—read IT—were not up to snuff.

The short answer to the question posed above—i.e., how to make the technology spending pay off—is almost too simple. We submit that the proper level of senior management support, adequate planning, and a suitable organizational structure, mixed with a dose of common sense, will together forestall major system mishaps.

The most vital element on which all others depend is senior management, with which we deal below. Following this we discuss key issues in planning, organization, and culture, the "bells and whistles" syndrome, and staffing. We conclude with a summary and checklist of the key success factors for exploiting banking technology.

LESSONS

Management: The Buck Stops Here

There is no substitute for active senior management support and involvement. Throwing money at and abdicating all responsibility to staff to fix the back-office mess just will not do.

Consider the example of a large, U.S. institution—let us call it Bank A—known for its aloof and somewhat erratic senior management. This firm spent some seven calendar years (and who knows how many manyears) attempting without success and with untold millions wasted to automate its Capital Markets Trading area with an integrated deal capture, order processing, and risk management system.

In addition to the uncertainty and turmoil engendered by management vacillation at the top, Bank A also suffered the consequences of violating some cardinal rules of systems "in the trenches." To wit: too many chiefs; little cooperation between business and IT units; and little or no sense of the need to integrate IS developments with corporate business strategies.

As the saying goes, when everyone is in charge nobody is in charge. Rather than having one senior-level businessperson with overall responsibility, in this case there were three different consulting organizations working with and under the nominal authority of Bank A's IT unit. In reality, as one can easily imagine, responsibility was so diffuse as to be virtually nonexistent.

It should come as no great surprise that, a full year after project inception, the team proudly presented its six-volume functional specifications report only to have it unceremoniously and flatly rejected by the Capital Markets management. Oh well: They'd just start all over again.

A stark study in contrasts is presented by IT developments at a privately held dealer with offices in New York and London. Under the strong leadership of the head trader, a director and number two at the firm, the systems development group benefited from active support and participation of senior management at the highest level. No doubt the business side was in firm control of the project; the tail wasn't wagging the doe.

Of equal importance was the fact that the entire community of ultimate users was involved from beginning to end. Neither senior management nor the systems group were interested in IT for the bells and whistles, but rather wanted a system that would support their business plan for achieving a competitive edge over others using technology

The head trader put the lie to the cliche that traders are too busy to be bothered by systems analysts and designers with a fresh and rather democratic approach. IT design meetings were obligatory for all potential users, as were the 'homework' assignments. The rationale, as the head trader put it, was, "You are the ones for whom the system is being built, so you better speak up (with your suggestions and criticisms) now, or shut up later." This was clearly management's prerogative and vision.

The unsurprising result was a state-of-the-art analytic, deal capture, order processing, and risk management system which is an integral part of their business, actually used as intended by those for whom it was developed. Most importantly, it has enabled the firm to more than triple its volume, with negligible cost and staff increases.

Management support and leadership are also crucial for proper planning, both at the strategic/corporate level and at the personal level between business unit and IT staffers. A healthy organizational structure and culture must be fostered, one that encourages communication and understanding; in other words, a common language between the business and technical people.

Planning: It Will Be More Costly Later

As with senior management support, there is no substitute for proper planning. Thorough analysis and design will more than pay for itself by detecting serious flaws when it is still relatively cheap (and easy) to correct them. The costs of correcting IT errors grow increasingly dearer the farther along the project has advanced. Most expensive to fix, of course, are bugs in "live" systems.

Shearsori was one investment bank that epitomized the effectiveness and efficiencies of careful and meticulous planning, particularly during its many acquisitions over some three decades, until Smith Barney ultimately bought it. A case in point was its seemingly effortless conversion of E.F. Hutton's systems, with hundreds of branches, millions of accounts, and billions in assets, to those of Shearson in a few short weeks.

Sadly for Wall Street, this was the exception that underscores the rule. Closer to the norm was the agony endured by Bank A—its takeover of a fellow investment bank proved very costly in both time and money. The problems associated with merging of the two back offices took countless man-hours to solve and kept New York's livery services busy ferrying Bank A staff through all hours of the night.

Examples of inadequate up-front planning are not limited to U.S. banks. Global fiascoes include London Clear, and especially the Taurus back-office system debacle in the City of London.

Fundamentally, planning should ensure that IT is in tune and integrated with the firm's business strategy. In other words, be certain that you have the right system. For some this is easier said than done. Take for example the U.S. investment bank that withdrew from a major line of business soon after bringing a multimillion-dollar trade support system on-line.

The proper meshing of business and technology planning can pay off...

Table of contents

- Cover

- Title Page

- Copyright Page

- Contents

- FOREWORD

- ABOUT THE CONTRIBUTORS

- 1. Making Banking Technology Spending Pay: Key Success Factors

- 2. Developing a Successful Technology Plan

- 3. Designing a Technology Architecture and Strategy

- 4. Understanding Bank Technology—The Customer and the Expectation

- 5. Why the Internet Is Crucial to Bank Executives

- 6. Addressing Fraud and Security in Electronic Commerce

- 7. Risk Management—A Survey of Available Technology

- 8. A Strategic Approach to Outsourcing

- 9. Making Outsourcing Work: 10 Steps to Negotiating the Right Contract

- 10. Managing the Bank's Networks and Personal Computers

- 11. Technology's Impact on the Mortgage Industry

- 12. Technology's Role in Mergers and Acquisitions

- 13. Regulatory Issues and Their Impact

- INDEX

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Managing the New Bank Technology by Marilyn R. Seymann in PDF and/or ePUB format, as well as other popular books in Economics & Business General. We have over 1.5 million books available in our catalogue for you to explore.