This book provides a comprehensive overview of the financial integration of emerging economies through an in-depth analysis of the international monetary system, how it impacts capital flows and exchange rates, and its implications for policy making.

The financial integration of emerging economies has been a remarkable development of the past two decades. The growth of cross-border transactions and asset ownership, not least through the accumulation of foreign exchange reserves, has put many of these countries in a more prominent, if still peripheral, position within the global financial system. This has not been a smooth process, as integration has been marked by cyclical waves of capital flows, with financial and currency instability often accompanying the acute phases of these cycles. While conventional economic theory traditionally sees financial integration as a positive development, Post-Keynesian economists, working in the tradition of Keynes, Minsky and Kalecki, have long taken a more sceptical viewpoint. By centring the analysis of financial dynamics on concepts as liquidity, uncertainty, balance-sheet structures and institutions, Post-Keynesian theory highlights the intrinsic character of shocks imposed by financial integration upon emerging economies, and their implications for economic growth and distribution. This book demonstrates that these analyses can be fruitfully used to gain a better understanding of financial (in)stability and economic development in emerging economies as they integrate into the global financial system.

This work provides key reading for students and scholars of economics, political economy and finance that are interested in the financial integration of emerging economies, and how the heterodox tradition of Post-Keynesian economics contributes to its analysis.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Bruno Bonizzi, Annina Kaltenbrunner and Raquel A. Ramos

In March 2020, as the COVID-19 crisis started to ravage Europe, global financial markets went into turmoil. In emerging economies1 (EEs), unprecedent amounts of portfolio investments (García-Herrero and Ribakova, 2020) were pulled out from capital markets and international access to credit was strained. The result were huge adjustments in domestic exchange rates and asset prices. These adjustments came after a decade of EEs, which started to include a growing number of hitherto excluded countries, having reached unprecedented access to global financial markets. As of yet, the full consequences of this sudden stop are not clear but are likely to be severe.

These boom-bust dynamics of foreign financial2 inflows, asset prices and exchange rates, have been a recurring theme for EEs over the past forty years – even if each time the transmission mechanisms and markets affected were different. Latin American and African countries suffered external debt crises in the 1980s as a hike in US interest rates made debts, mainly in the form of syndicated loans from commercial banks and accumulated on the back of recycled petrodollars (United Nations, 2017), unsustainable. A new wave of financial inflows, increasingly dominated by short-term private operators, ended abruptly and resulted in a series of devastating balance of payments crises in Latin America, East Asia, Russia and Turkey in the late 1990s and early 2000s. Many EEs opted for sharp increases in interest rates and abandoned their pegged exchange rate regimes. The 2000s boom in financial flows, again larger and more diversified – thanks to the rise of portfolio and derivative transactions – than anything seen before, ended with a great reversal in 2008–2009 in the context of the Global Financial Crisis (GFC). This time newly financially integrated economies from Eastern Europe were particularly hardly hit.

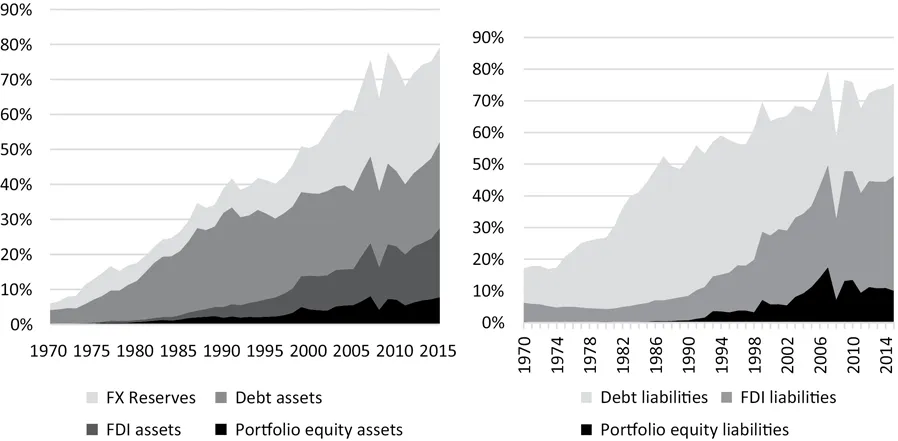

The experience of EEs with foreign financial flows shows therefore a growing and troubled integration. The current financial shock is only the most recent in a long series of ever-increasing cycles of foreign financial flows; each larger and more complex in its vulnerabilities than the previous. This is shown in Figure 1.1 which evidences the secular, but volatile growth in cross-border assets and liabilities, interrupted periodically by financial adjustments and crises.

Figure 1.1Emerging and developing economies, cross-border assets and liabilities %GDP.

Source: Dataset by Lane and Milesi-Ferretti (2018). Emerging and developing economies are all countries except for the Eurozone, European Free Trade Association countries, the United Kingdom, the United States, Canada, Japan, Australia and New Zealand. The graph on the left shows cross-border assets, the graph on the right shows cross-border liabilities.

These adjustments have been extremely costly for emerging markets. The debt crises of the early 1980s are widely regarded as the start of a ‘lost decade’ for economic development in Latin America and Africa, as policy responses focussed on fiscal adjustment to face restructured debt commitments. Similarly, the EE crises of the late 1990s have been estimated to cost about 8% of GDP on average (World Bank, 2005). The current COVID-related unprecedented retrenchment of financial flows significantly increases the policy challenges of EEs having to consider their international financial relations and access to global liquidity, in addition to the massive task of addressing a pandemic and a global recession (García-Herrero and Ribakova, 2020). Given the prominence of this process and its potentially detrimental implications, a critical analysis of the causes and effects of financial integrations for exchange rates, asset markets, monetary policies and the domestic economy in general is fundamental to fully understand the current situation and prospects of EEs.

Standard neoclassical models offer unqualified support to free capital movement, which would allow capital to flow to where it is scarcer and therefore higher yielding, i.e. developing countries (Obstfeld, 1998). Over the last decades, most economists have become more careful about their support for financial globalisation, both on the back of the damage originated by financial crises and the elusiveness of its benefits: integration is no longer seen as a boon for growth directly, but rather affects a number of ‘collateral benefits’ (Kose et al., 2006) and requires a number of good policies as preconditions to be ‘done right’ (Mishkin, 2007). Most recent contributions have clearly highlighted the potential negative consequences of liberalisation. Nevertheless, they still effectively keep liberalisation as a policy objective, though qualified in terms of timing and scope and complemented with additional policy measures to mitigate its harmful consequences (Furceri et al., 2019; Broner and Ventura, 2016).

Outside the mainstream of the profession, other economists and political economists have historically been more critical about financial globalisation. In particular, basing their analyses on John Maynard Keynes and Hyman Minsky, among others, Post Keynesian economists have long provided alternative analyses and perspectives, which do not start from the premise that financial integration is fundamentally positive for economic growth and stability. Instead, these authors have highlighted the endogenous and inherent instability created by short-term financial markets, studied their implications and offered policy alternatives. The purpose of this book is to collect contributions on this topic of scholars working broadly within the school of thought of Post Keynesian economics, which have not yet been grouped together, as we review in the next section.

The Post Keynesian contribution: A historical overview

Post Keynesian economics is an approach to economic analysis with some distinctive characters, such as the focus on monetary theory, the principle of effective demand, and income distribution. As the authoritative book by Lavoie (2014) shows, open economy issues are however not as well established as other core Post Keynesian themes. Historic exceptions to this observation are works based on Keynes’ plan for reforming the international monetary system, and the so-called balance of payments constrained growth theory. The former are policy-oriented contributions, discussing Keynes’ idea of a system based international clearing agency to account for imbalances between debtor and creditor countries. This literature however mostly ignores the experience of EEs. The latter, originated by Thirlwall (1979), is based on a version of the Harrordian growth model, where export demand drives long-term growth, constrained by the growth of imports to achieve external current account stability. This theory was frequently applied to the analysis of EEs, especially by authors influenced by Latin American Structuralism, which has a long tradition in analysing long-term growth on the basis of export composition (Missio et al., 2015). By and large, however, these contributions focussed on trade, mostly ignoring the role of finance and financial integration.

Since the 1990s, and especially since the currency and financial crises at the end of that decade, new studies emerged that sought to extend and apply some of the theoretical apparatus of Post Keynesian economics to the case of foreign financial flows, exchange rates and EEs. A bibliometric research shows how this literature emerged in 1991 with a seminal article by John T. Harvey, (1991), which puts forward the foundations for a Post Keynesian theory of exchange determination based on the concept of fundamental uncertainty. A search for the main keywords of the area through Scopus shows how this literature has progressively grown over time, with over 200 articles included in our sample search (Figure 1.2 left graph). This does not capture the full extent of the literature, as books and reports for example are excluded and publications in languages other than English only appear if they have keywords or abstracts in English, but serves as an indication of an expanding branch of scholarship.

The increased interest in the subject is also reflected in rising numbers of citations, which, as proxied citations to the articles captured by the search presented in Figure 1.1 shows, have increased significantly in recent years. Indeed, in the last four years the number of citations to Post Keynesian articles on capital flows and exchange rates in EEs has more than tripled (Figure 1.2 right graph). Of these publications about 45% are published in the Journal of Post Keynesian Economics, 20% in the Journal of Economic Issues, the Review of Political Economy and the Cambridge Journal of Economics, and the remaining 35% in other journals and reviews. The literature seems to be geographically concentrated among authors from three countries: 29% of the papers have an author affiliated to a US institution, 19% to a Brazilian one and 13% to a UK institution. Articles included are mainly in English, but a significant minority were in Portuguese or Spanish. While these figures do not capture the entirety of the literature and focus only on peer-reviewed articles, they nonetheless show its clear expansion over the past two decades and a sharp increase in interest more recently.

Figure 1.2Publications and citations per year.

Source: Scopus. We searched for ‘exchange rate’, ‘capital flows’, ‘financial integration’, ‘financial globalisation’ and ‘open economy’ in the Abstract, Title or Keywords, in the Journal of Post Keynesian Economics, the Journal of Economic Issues and the Review of Political Economy, as well as in all journals when combined with the words ‘Minsky’ and ‘Post Keynesian’. The graph on the left shows total publications in the given period. The graph on the right shows the number of citations per year of all papers included in our sample.

The PK literature on open economies builds on a variety of well-established concepts of the wider PK tradition. Table 1.1 seeks to summarise these various strands. The list is likely not exhaustive and might not do full justice to the complex and variegated existing research but aims to give a broad overview of the main topics pursued in Post Keynesian open economics.

Table 1.1 Post Keynesian literature on foreign financial flows, exchange rates and EEs

Area, topics

Theoretical background

Seminal references

Exchange rate determination

Fundamental uncertainty, animal spirits (Keynes, Davidson)

(Alves et al., 1999; Harvey, 1991; Davidson, 2002a)

Interest rate parity and the Forward Rate

Endogenous money (Le Bourva, Lavoie)

(Kregel 1982, Lavoie, 2000; Smithin, 2002)

Financial instability and crisis

Financial instability hypothesis (Minsky)

(Arestis and Glickman, 2002; Dymski, 2000; Kregel, 1998)

Currency hierarchy

Liquidity preference

German Monetary Keynesianism

(Keynes, Minsky)

(Andrade and Prates, 2013; Dow, 1999; Herr and Hübner, 2005; Kaltenbrunner, 2015; Terzi, 2005)

Current account and growth

Balance-of-payment constrained growth

Structuralism

(Kaldor, Thirlwall, Kalecki)

(Blecker, 1989; Thirlwall, 1979; Thirlwall and Hussain, 1982)

Capital controls and international monetary system

(Keynes, 1942; Davidson, 2002b; Grabel, 2003)

The first seminal area was the application of Post Keynesian monetary theory to exchange rate determination itself. A large part of this literature owes a lot to the work of John T. Harvey and Paul Davidson as key references. These authors sought to challenge conventional exchange rate theory by applying the Post Keynesian concepts of fundamental uncertainty and inter-subjective expectations formation, such as conventions ...

Table of contents

Cover

Half Title

Series Information

Title Page

Copyright Page

Contents

List of figures

List of contributors

Part I Introduction and background

Part II Minsky, balance sheets and cycles

Part III Currency hierarchy

Part IV Current account and growth

Part V Policy implications

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Emerging Economies and the Global Financial System by Bruno Bonizzi, Annina Kaltenbrunner, Raquel A. Ramos, Bruno Bonizzi,Annina Kaltenbrunner,Raquel A. Ramos in PDF and/or ePUB format, as well as other popular books in Economics & Economic Theory. We have over 1.5 million books available in our catalogue for you to explore.