"A range of naval experts . . . build[s] a diverse and deeply-thought out picture of where maritime warfare is now and where it is likely to go."—

Army Rumour Service

What is the purpose of navies in the modern world, and what types of warship does this require? This book tackles these questions by looking at naval developments, both technological and operational, in the quarter century since the end of the Cold War. It provides the overall political and economic context, assesses significant naval operations from the first Gulf War to Russia's annexation of Crimea, reviews changes in the objectives and composition of the principal fleets, describes major design developments amongst the main warship types, and examines wider technological and operational developments, including naval aviation, shipbuilding and manning.

"A high quality publication with a great many superb photographs. For those wishing to keep fully informed on world naval affairs, it is excellent value and strongly recommended."—Scuttlebutt

"This new book follows the successful approach and format of the very popular naval annual

Seaforth's World Naval Review. Under the same editor, a new team of specialists have been assembled to write authoritative articles in their particular fields of expertise. The absorbing text is fully supported by many outstanding images—Most Recommended."—Firetrench

"Provides a most useful contextual analysis of the post-Cold War period, explaining how technological developments and a range of world events have variously shaped the fleets of today."—

Warship

- 240 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Navies in the 21st Century

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Subtopic

21st Century HistoryIndex

History1.0 |

INTRODUCTION

Navies in the twenty-first century exhibit significant changes from their counterparts at the time of the Cold War’s end, now a quarter of a century ago. Many of the major fleets that dominated the world’s oceans – deprived of longstanding core roles virtually overnight – are now much smaller than they were then. They have, over the same period, been joined by a new cohort of emerging naval powers, many located in Asia. These new fleets have been financed by the shift in world trade towards the broader Asia-Pacific region and justified by rising regional tensions.

However, change extends much further than this. The evolution of the global political order away from a bipolar stand-off between NATO and the Warsaw Pact (and their respective allies) has been accompanied by a period of instability which has brought new and different missions to replace those lost. These often require different types of warship, as well as changed methods of operation. Technology, increasingly derived from civilian applications in a reversal of the historic direction of travel, has also proceeded apace. This is, perhaps, most evidenced by the accelerating use of unmanned and autonomous vehicles. However, it has also had important implications for such wide-ranging areas as command and control, propulsion, stealth and manning. Meanwhile social change has been reflected in a decisive shift away from conscription towards all-volunteer, professional services and in the growing numbers of women serving at sea.

The US Navy Los Angeles class submarine Pasadena (SSN-752) prepares to undock from the floating dock Arco (ARDM-5) as the Arleigh Burke class destroyer Stockdale (DDG-106) departs San Diego harbour in January 2016. Although Asian fleets are of growing importance, the US Navy remains the world’s largest and best-funded fleet by a considerable margin. (US Navy)

Since 2010, Seaforth World Naval Review has chronicled some of these changes on a yearly basis. However, the short timeframe inherent in this approach is not necessarily the best way to identify and assess trends that might take a decade or more to emerge. Navies in the 21st Century therefore attempts to take a longer-term and broader perspective in describing both why and how fleets have evolved in the post-Cold War age. In doing this, the hope is to complement the periodic analysis contained in the Seaforth World Naval Review series with a more comprehensive assessment of why things are the way they are now. At the same time, as relations between Russia and the West cool once more as a result of events in Ukraine and the Crimea, the book aims to explain to a broader readership the current importance, objectives, structures and capabilities of the world’s major fleets.

Navies in the 21st Century follows the methodology established by the annuals in calling on recognised experts to elaborate on these key themes. This introduction aims to set the financial context to post-Cold War naval developments and outline the major areas addressed in subsequent chapters.

THE FINANCIAL BACKGROUND

One of the biggest factors influencing naval force structures across the world is inevitably the amount of money governments allocate to spending on the military. A good starting point from which to analyse global world naval development is, therefore, to understand this financial backdrop.

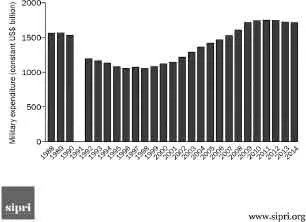

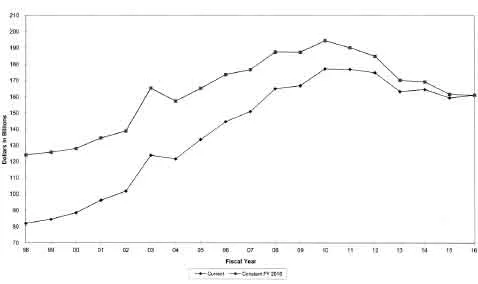

Global Trends in Defence Spending: In spite of considerable discussion about the post-Cold War ‘peace dividend’, it is important to appreciate that the world, at the start of 2015, was actually spending a little more cash on the military than it did at the end of the Cold War. This is graphically illustrated by Diagram 1.1, provided courtesy of SIPRI.1 Arguably, there are three main reasons for this:

The British Royal Navy’s technologically advanced Type 45 air-defence destroyer Diamond escorting the Danish merchant ship Ark Futura in the course of Operation ‘Recsyr’, part of the UN-sponsored mission to destroy Syria’s chemical weapons, in 2014. The post-Cold War era has seen navies acquire new technology and adapt to a broad range of missions. (Crown Copyright 2014)

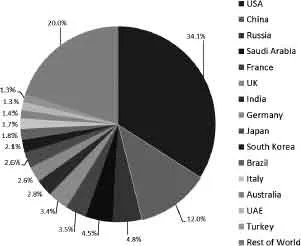

Although the impact of the world financial crisis that started in 2008 and a large government deficit have curtailed United States’ defence spending since the beginning of the current decade, it remains the world’s dominant military power by a considerable margin. The United States spends three times as much on its military as its nearest rival, China, and accounts for around a third of the world’s defence spending overall. It also remains by far the largest economy, being over two-thirds larger than China in nominal terms.2 Moreover, the United States benefits from a network of alliances with many of the other world’s major powers, which share a common interest in a global trading economy that relies on a stable international order. In spite of perceived threats to American dominance in Asia and elsewhere, it is difficult to perceive the basic status quo changing materially in the short to medium term. Equally, the US Navy looks firmly anchored to its position as the world’s dominant naval force.

1.1: World military expenditure, 1988–2014

1.2: The share of world military expenditure of the 15 states with the highest expenditure in 1989 (SIPRI)

1.3: The share of world military expenditure of the 15 states with the highest expenditure in 2014 (base data courtesy of SIPRI)

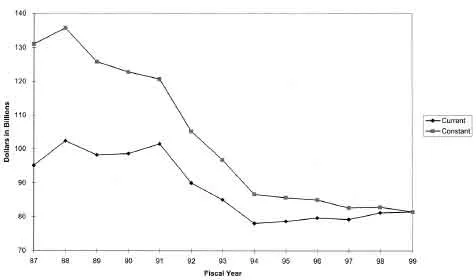

1.4: DoN FY 1999 Budget Estimates Real Program Trends

1.5: DON FY 2016 Budget Estimates Real Program Trends

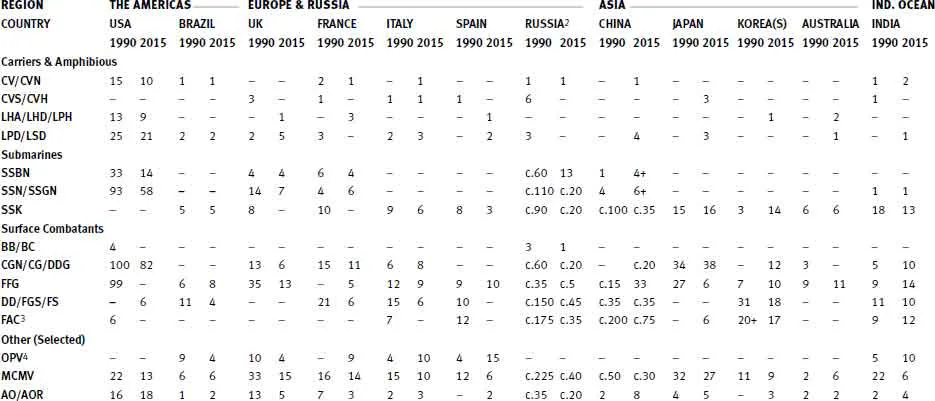

1.6: MAJOR FLEET STRENGTHS – 1990–20151

Notes

1 Numbers are based on official sources, where available, supplemented by news reports, published intelligence data and other ‘open’ as sources as appropriate. Given significant variations in available data, numbers should be regarded as indicative, particularly with respect to Russia, China and minor warship categories. There is also a degree of subjectivity with respect to warship classifications given varying national classifications and this can also lead to inconsistency.

2 1990 data refers to the Soviet Union, dissolved at the end of 1991. The precise status of the Soviet/Russian fleet at the end of 1990 is rather speculative, as many warships held in official reserve status never returned to operation.

3 FAC numbers relate to ships fitted with or for surface-to-surface missiles.

4 The lack of offshore patrol vessels for some countries reflects the existence of a separate coast guard for the performance of territorial constabulary roles. These can be significant forces.

Naval Expenditure & Force Structures: Of course, overall trends in and amounts allocated to military expenditure do not necessarily correlate to naval investment. A good case in point is Saudi Arabia, which currently has the fourth largest defence budget in the world but only a comparatively small navy due to the priority attached to land-based forces. Even when money is directed to the naval budget, this does not inevitably result in a more numerous or powerful fleet. The costs of new technology, ill-judged investment decisions and the need to provide adequate conditions of service and compensation to service personnel with growing expectations are just a few examples of factors that can eat away at naval funding.

Given its status as the world’s most powerful naval force, it is instructive to look at the development of the US Navy’s budget and force structure from the late 1980s with these perspectives in mind. Since then, it has shrunk from the near ‘600-ship fleet’ targeted during the Reagan presidency to somewhat less than 300 ships today. As defence expenditure remains close to 1980s levels, this decline inevitably warrants some explanation. The following factors seem relevant:

The Norwegian Fridtjof Nansen class frigate Thor Heyerdahl in company with other warships off the Nor...

Table of contents

- Cover

- Title Page

- Copyright

- Contents

- Foreword by Geoffrey Till

- Section 1: Navies in the 21st Century

- Section 2: Strategic Overview

- Section 3: Operational Overview

- Section 4: Fleet Analysis

- Section 5: Naval Shipbuilding

- Section 6: 21st Century Warship Designs

- Section 7: Post-Cold War Technical Developments

- Section 8: Aircraft

- Section 9: Personnel

- Glossary

- Contributors

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Navies in the 21st Century by Conrad Waters in PDF and/or ePUB format, as well as other popular books in History & 21st Century History. We have over 1.5 million books available in our catalogue for you to explore.