A growing body of evidence suggests that financial literacy plays an important role in financial well-being, and that differences in financial knowledge acquired early in life can explain a significant part of financial and more general well-being in adult life. Financial technology (FinTech) is revolutionizing the financial services industry at an unrivalled pace. Views differ regarding the impact that FinTech is likely to have on personal financial planning, well-being and societal welfare. In an era of mounting student debt, increased (digital) financial inclusion and threats arising from instances of (online) financial fraud, financial education and enlightened financial advising are appropriate policy interventions that enhance financial and overall well-being.

Financial Literacy and Responsible Finance in the FinTech Era: Capabilities and Challenges engages in this important academic and policy agenda by presenting a set of seven chapters emanating from four parallel streams of literature related to financial literacy and responsible finance.

The chapters in this book were originally published as a special issue of TheEuropean Journal of Finance.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

The effectiveness of smartphone apps in improving financial capability

French DeclanMcKillop DonalStewart Elaine

ABSTRACT

This study is the first to assess whether smartphone apps can be utilised to improve financially capable behaviours. In this study four smartphone apps, packaged together under the title ‘Money Matters’, were provided to working-age members (16–65 years) of the largest credit union in Northern Ireland (Derry Credit Union). The smartphone apps consisted of a loan interest comparison app, an expenditure comparison app, a cash calendar app, and a debt management app. The assessment methodology used was a Randomised Control Trial (RCT) with the U.K. Financial Capability Outcome Frameworks used to set the context for the assessment. For those receiving the apps (the treatment group) statistically significant improvements were found in a number of measures designed to gauge ‘financial knowledge, understanding and basic skills’ and ‘attitudes and motivations’. These improvements translated into better financially capable behaviours; those receiving the apps were more likely to keep track of their income and expenditure and proved to be more resilient when faced with a financial shock.

1.Introduction

Making good financial decisions is important for a person’s economic and financial well-being (Money Advice Service 2013). Whether a person is in a position to make good financial decisions is, however, dependent upon their financial capability. The OECD defines financial capability as ‘a combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial wellbeing’ (OECD INFE 2011). This emphasises that financial capability is about not only having knowledge, understanding and skills but also the ability to apply these attributes in a way that results in positive financial outcomes (Spencer, Nieboer, and Elliott 2015). Financial capability does not necessarily follow from having knowledge, understanding and skills it is shaped also by the psychological motivations and biases that drive our behaviour (Hershfield et al. 2011).1

Increasing levels of financial capability in the U.K. population is a Government priority (Financial Capability Strategy for the UK 2015). Measurement of the financial capability of the U.K. population suggests that at best it is mediocre (Spencer, Nieboer, and Elliott 2015). Approximately 30% of the U.K. population do not make a budget. One in six have problems in identifying the balance on their bank statement. Almost 90% of U.K. adults do not read the full terms and conditions when taking out financial products and nearly half of U.K. adults admit falling into debt as a direct result of their social lives (Money Advice Service 2013). A survey undertaken by the Financial Services Authority (FSA) in 2005 found that those who scored well below average on all aspects of financial capability were young (average age 36), and included roughly equal numbers of single people and couples. Furthermore, their incomes and levels of product holding were lower than average, but not the lowest of all the groups surveyed (FSA 2006).2

The Financial Capability Strategy for the U.K., 2015 highlights the improvement of digital literacy as an important outcome in the advancement of financially capable behaviours ‘ … being able to use online banking services, to use mobile apps, and to compare financial services online is crucial for being able to keep track of your money and make informed decisions’ (Bagwell et al. 2014, 22, Financial Capability Outcome Frameworks). Digital literacy is the ability to effectively and critically locate, evaluate and create information using a range of digital technologies (Spires and Bartlett 2012). There are five basic digital skills: managing information, communicating, problem solving, transacting and creating (Reedy and Goodfellow 2012). Attainment of these digital skills could save the average person in the U.K. £744 per annum (Lloyds Bank 2017). However, 1 in 10 U.K. adults (aged 16+) have never used the internet (ONS 2017), and 4.3 million people are thought to have none of the five basic digital skills (Lloyds Bank 2018).

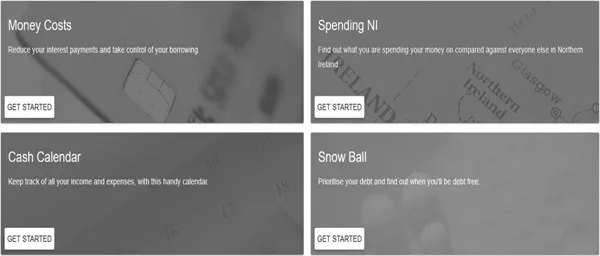

In the U.K., 41 million 16–75-year-olds own a smartphone, with those aged 55–75 the fastest growing adopters (Deloitte 2017). While there is extensive research on the effectiveness of smartphone apps in the improvement of health outcomes and behaviours, there are no studies investigating the efficacy of smartphone apps as a means of improving financial capability.3 Our study addresses this paucity of research by assessing whether four smartphone apps, packaged together under the title Money Matters, could improve financially capable behaviours of working-age members (16–65 years) of the largest credit union in Northern Ireland (Derry Credit Union).4 The smartphone apps consisted of a loan interest comparison app (Money Costs), an expenditure comparison app (Spend NI), a cash calendar app (Cash Calendar), and a debt management app (Snowball). Further details about each app are provided in Figure 1.

Figure 1.‘Money Matters’ mobile app package.

Notes: Developed by the authors and a local web developing company, each app has been specifically designed to target, facilitate and improve different aspects of an individuals’ financial capability. The first app (Money Costs) is a tool to enable participants to easily compare different types of borrowing using different amounts and time periods. The second (Spending NI) provides an indicator of how much a user spends against the Northern Ireland average household spend in various spending categories. The third (Cash Calendar) is a budgeti...

Table of contents

Cover

Half Title

Title Page

Copyright Page

Contents

Citation Information

Notes on Contributors

Introduction: Financial literacy and responsible finance in the FinTech era: capabilities and challenges

1 The effectiveness of smartphone apps in improving financial capability

2 Cross-country variation in financial inclusion: a global perspective

3 Measuring financial well-being over the lifecourse

4 Financial literacy and financial well-being among generation-Z university students: Evidence from Greece

5 Financial literacy and student debt

6 Keep your customer knowledgeable: financial advisors as educators

7 Financial literacy and fraud detection

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Financial Literacy and Responsible Finance in the FinTech Era by John O.S. Wilson, Georgios A. Panos, Chris Adcock, John O.S. Wilson,Georgios A. Panos,Chris Adcock in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.