This book analyses the economic and social impact of the Covid-19 crisis with special focus on India. It examines the economic disruption caused by the pandemic, policy responses to it and the prospect of a severe global recession. It also covers how the pandemic has contributed to considerable suffering among the masses and affected socio-cultural relationships, behavioural patterns and psychological attitudes governing human interaction.

A topical and timely collection on the pandemic, the essays in the volume discuss several key themes which include,

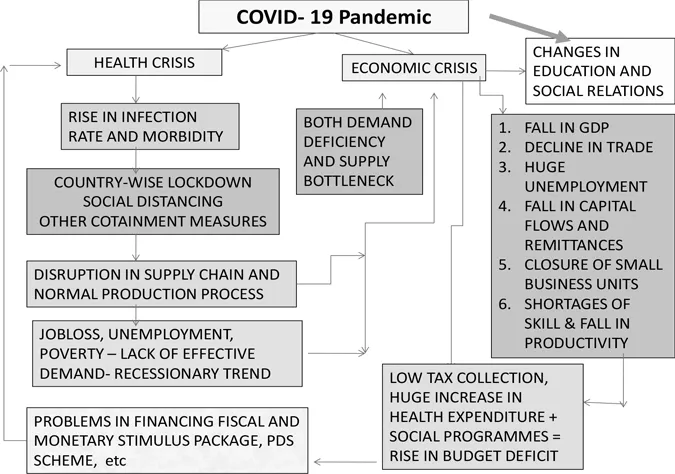

· The Corona pandemic and the changing global economy; growth, trade and macroeconomic recovery;

· Public health and policy failures; appropriate policy response;

· Impact on education; guidelines for the future;

· Idea of economic herd immunity; impact of India's lockdown, crisis of the migrant labourers;

· Impact on agriculture, industry, firms, households and the informal sector;

· Implications of digital technology for production, labour and labour relations;

· Violence amidst the virus; Covid 19 and Hindu- Muslim conflict in India, domestic violence, questions of occupation, identity, gender and vulnerability;

· De-globalisation and environmental challenges in the post-Covid era.

Engagingly written, this comprehensive volume compiles original research by leading economists from India and abroad. It will be useful for scholars and researchers of economics, of the Indian economy, development economics, development studies, labour studies, public policy, public administration, governance, sociology and political economy.