The overarching goal of South Africa's National Development Plan (NDP) is to eliminate poverty, reduce inequality, lower unemployment and increase the labour participation.This book contributes to academic and policy efforts to achieve these NDP goals. We establish that the coal, metal ores and the platinum group commodity sectors will underpin the mining as a "sunrise" industry. The export-led growth strategy is necessary for intensive employment creation but must be complemented by other micro, macroeconomic and industrial policies. A strategy of minerals beneficiation is important for intensive employment creation. Accelerated land reform is a supply side or structural reform policy intervention tool aimed at increasing potential output, changing ownership patterns in the economy, increasing entrepreneurship, labour absorption, economic inclusion and lowering income inequality. Evidence shows that the balance sheet channel, commodity price booms and busts are intricately linked with the exchange rate dynamics, policy uncertainty, confidence and the effects of droughts (also symptoms of climate change). Productivity and investment growth shocks matter for output, employment and price stability. Evidence indicates that nominal GDP growth above 10 percent and keeping inflation within the target band leads to significant increase in employment and decline in unemployment, without inflationary pressures, especially when inflation is below 4.5 percent. To operationalise the NDP targets, align and co-ordinate policies, the South African Reserve Bank (SARB) mandate can be expanded to include maximum employment. This must be complemented by lowering the inflation target band, adjusting the financial regulatory, macro-prudential and monetary policy frameworks. This will enhance the conduct and credibility of monetary and financial stability policies to achieve the set objectives. These objectives make policy co-ordination pertinent and binding.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

N. Gumata, E. NdouAccelerated Land Reform, Mining, Growth, Unemployment and Inequality in South Africahttps://doi.org/10.1007/978-3-030-30884-1_1

Begin Abstract

1. Introduction

Nombulelo Gumata1 and Eliphas Ndou1, 2, 3

(1)

South African Reserve Bank, Pretoria, South Africa

(2)

Wits Plus, University of the Witwatersrand, Johannesburg, South Africa

(3)

School of Economic and Business Sciences, Johannesburg, South Africa

Nombulelo Gumata (Corresponding author)

Eliphas Ndou

End Abstract

The South African National Development Plan (NDP) targets net 11 million new jobs or an unemployment rate of 6 per cent 2030 to increase the labour participation rate to 65 per cent. In addition, the NDP’s overarching goal is to eliminate poverty, reduce inequality from the current aggregate level of 0.68 to 0.6. What needs to be done? This book contributes to academic and policy efforts to answer this question and forward concrete and implementable policy recommendations. This book is divided into six parts that are dedicated to answer this question:

Part I deals with how the interaction between nominal wage inflation, consumer price inflation and the exchange rate appreciation and depreciation episodes influences output costs associated with disinflation.

Part II evaluates the performance of the inflation targeting framework in South Africa and assesses whether nominal GDP growth targeting is a viable alternative.

Part III estimates the output-employment intensities and the structural change indices. It decomposes overall productivity into changes of productivity within sectors and changes in the allocation of labour between sectors, alternatively structural change.

Part IV deals with policy uncertainty, mining sector charter, exchange rate volatility, commodity price booms and busts, binding minimum wage increases and the mining sector.

Part V addresses the policy of accelerated land reform in the agricultural sector and its implications for food security and affordability, price stability, output growth and employment growth, especially youth employment.

Part VI deals with the interaction between the financial sector regulatory framework, the property rights clause and the South African Reserve Bank mandate.

We apply a variety of econometric techniques to capture the various aspects of the transmission of shocks into the South African economy. We test several hypotheses and the applicability of some theoretical models to determine whether they are agreeable and relevant for the South African economy. In all instances, we use various econometric techniques to assess the robustness of the empirical findings and the policy implications.

1.1 The Interaction Between Nominal Wage Inflation, Consumer Price Inflation and the Exchange Rate Appreciation and Depreciation Episodes Influences Output Costs Associated with Disinflation

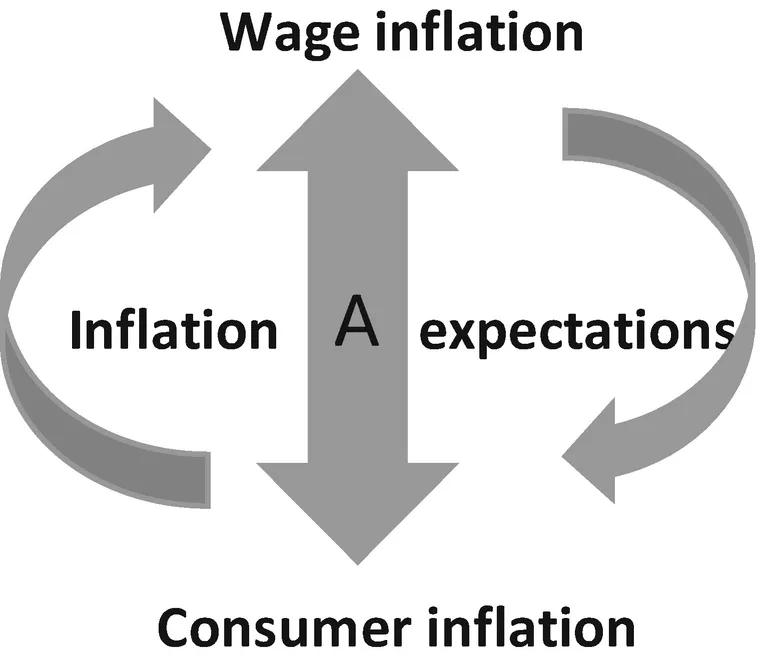

This part of the book is premised on the inflation-wage spiral depicted in Fig. 1.1. The direct and indirect channels of transmission of the exchange rate depreciation affect labour markets, wage setting behaviour and consumer price inflation. The stages of the transmission channels indicate that the exchange rate depreciation shock (i) directly impacts nominal wage and consumer price inflation (first-round stage) via an increase in the import prices of input, production and finished goods and (ii) the inflationary changes are also transmitted into wage inflation via the indirect or second-round effects. Furthermore, inflation expectations play an important role in the link between nominal wage and consumer price inflation, alternatively, the wage-inflation spiral as shown in Fig. 1.1.

Fig. 1.1

Inflation-wage spiral relationship and the role of inflation expectations. (Source: Authors’ drawing)

We find that nominal wage inflation and consumer price inflation display very similar disinflation episodes over time as shown in Fig. 1.2. Furthermore, the trends show that nominal wage inflation and consumer price inflation have trended downwards in a comparable fashion over time. The nominal wage inflation trend has declined significantly post the recession in 2009 and is approaching the upper band of the inflation targeting range.

Fig. 1.2

Consumer and wage price inflationary and disinflation periods. (Note: Shaded areas represent the disinflation periods which are at least 2 percentage points lower than at the peak. The centred nine-quarter moving average inflation is expressed in per cent. Source: Authors’ calculations)

Furthermore, Fig. 1.3 shows that real wage inflation has accordingly declined and has been persistently below the long-term average of 2.52 per cent since 2012Q1. This has narrowed the margin between nominal wage and consumer price inflation.

Fig. 1.3

Real wage inflationary and disinflation periods. (Note: Shaded areas refer to disinflation periods which are at least 2 percentage points lower than at the peak. The centred nine-quarter moving average inflation is expressed in per cent. Source: Authors’ calculations)

We conclude that the consideration of nominal wage growth does not necessarily imply a high level of inflation inertia or persistence compared to consumer price inflation. The policy implication is that this is another appropriate and policy-relevant approach at assessing the role of second-round effects emanating from the labour markets which is an integral part of the monetary policy formulation process.

1.2 An Evaluation of How the Inflation Targeting Framework Has Performed in South Africa

In light of prolonged deviations of real GDP growth and employment levels from linear trends post-2009 shown in Fig. 1.4, there has been a resurgence of arguments against the inflation targeting monetary policy framework. This part of the book chapter evaluates the performance of the inflation targeting regime in South Africa.

Fig. 1.4

Actual and trend real GDP and employment levels post-2009. (Source: South African Reserve Bank and authors’ calculations)

Insight from the relationship between output growth, output-gap and inflation (Phillips curve) shows that the relationship between the output-gap and inflation varies and this has been especially the case post-2009. Figure 1.5 shows that there are times during which both inflation and the output-gap move in the same direction, as well as times in which they diverge. The nature of shocks that drive inflation and the output-gap may at times move these variables in different directions. Pre-2009, the relationship between the output-gap and inflation was positive and steep but it has been rather weak and slightly negative post-2009. These trends mean that the period post-2009 has been characterised by the simultaneous occurrence of a negative and widening output-gap and inflation deviations from the target band.

Fig. 1.5

Inflation and output-gap post-2009. (Source: Ndou and Gumata 2017)

The flattening of the Phillips curve post-2009 implies that that inflation has become less responsive to resource slack (the output-gap) and is largely driven by other factors and shocks. Clarida (2019) states that a flatter Phillips curve is a proverbial double-edged sword. This is because it allows policymakers to support employment more aggressively during downturns as a sustained inflation breakout is less likely to occur when the Phillips curve is flatter. Nonetheless, a flatter Phillips curve also increases the cost economic output of reversing the unwelcome increases in longer-run inflation expectations. As a result, a flatter Phillips curve makes it more important that longer-run inflation expectations remain anchored at levels consistent with low and stable inflation. Furthermore, evidence shows that policymakers have considerable scope to engage in short-run demand management policies in the low inflation regime (when inflation is below 4.5) than in high inflation regime (when inflation is above 4.5). This is because there is a substantial degree of policy effectiveness in the low inflation regime and prices become more rigid as consumer price inflation moves below the 4.5 per cent inflation regime. Therefore, nominal demand shocks are unlikely to generate much inflation in the low inflation regime relative to the high inflation regime.

On the appropriateness of the current 3 to 6 per cent inflation target band, we demonstrate the importance of thresholds within the target range. Evidence shows that under different model specifications based on the economic growth theories, by the time the inflation rate hits 5 per cent, the economy has transitioned from a low to a high inflation regime as shown in Fig. 1.6. The transition functions within the current inflation target to capture the manner in which inflation moves from a low to a high inflation regime as it responds to certain shocks.

Fig. 1.6

The shape of the transition function for the inflation threshold. (Note: The vertical line in the shaded area denotes the estimated inflation threshold. Source: Ndou and Gumata 2017)

Furthermore, evidence shows that positive inflation shocks when inflation is between 0 and 3 per cent and below 4.5 per cent exert positive effects on GDP growth. This contrasts with negative effects exerted when inflation is above 6 per cent and 6.5 per cent, as GDP growth declines. These results imply that policymakers can exploit the inflation-output trade-off to their advantage when inflation is within certain thresholds within the current 3 to 6 per cent inflation target range. The transition functions of inflation from the low to the high inflation regime provide further evidence that a lower inflation target range of 2 to 4 per cent is consistent with a lower inflation regime.

On the issue whether nominal GDP (NGDP) growth targeting is a viable alternative to inflation targeting on South Africa, Fig. 1.7 shows that real GDP growth is higher when the gap between the NGDP growth and inflation is wider. During recessions inflation tends to exceed NGDP growth resulting in lower real GDP growth. This suggests that a combination of lower inflation and high NGDP growth is needed to achieve high real GDP growth. When we compare the Taylor rule policy prescriptions of how the conduct of monetary policy would evolve under consumer price inflation and NGDP growth targets, we find that the repo rate would be aggressively tightened to bring NGDP growth to target as shown in Fig. 1.8. Monetary policy tightening and the associated costs of disinflation are heightened under the NGDP growth targets. Thus, we conclude that South Africa would be worse-off under NGDP growth targeting compared to the current flexible inflation targeting framework.

Fig. 1.7

Inflation, nominal and real GDP growth. (Note: The grey shaded areas denote the South African recessions. Source: South African Reserve Bank and authors’ calculations)

Fig. 1.8

Average differences between the actual repo rate and Taylor prescriptions for CPI inflation and NGDP growth under different targets. (Source: Authors’ calculations)

However, a higher target for NGDP growth implies a lower Taylor rule prescription. During the recession in 2009, the repo rate would have been much lower than the actual repo rate at the time. Similarly, towards the end of the sample between 2014Q1 and 2016Q4, the Taylor rule would have been the same as the actual repo rate if the South African Reserve Bank (SARB) was targeting 10 per cent NGDP growth and slightly lower if the target was 12 per cent.

Thus, the results imply a higher NGDP growth driven by for instance positive productivity and investment shocks as opposed to higher CPI inflation is consistent with a low...

Table of contents

Cover

Front Matter

1. Introduction

Part I. The Interaction Between Nominal Wage Inflation, Consumer Price Inflation and the Exchange Rate Appreciation and Depreciation Episodes and their Influence on Output Costs Associated with Disinflation

Part II. An Evaluation of the Performance of the Current Inflation Targeting Framework in South Africa and Whether Nominal GDP Growth Targeting is a Viable Alternative

Part III. The Output-Employment Intensities and the Structural Change Indices

Part IV. Policy Uncertainty, Mining Sector Charter, Exchange Rate Volatility, Commodity Price Booms and Busts, Binding Minimum Wage Increases and the Mining Sector

Part V. The Implications of the Policy of Accelerated Land Reform for Food Security and Affordability, Price Stability and the Agricultural Sector Output and Employment Growth

Part VI. The Interaction Between the Financial Sector Regulatory Framework, Property Rights Clause and the South African Reserve Mandate

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Accelerated Land Reform, Mining, Growth, Unemployment and Inequality in South Africa by Nombulelo Gumata,Eliphas Ndou in PDF and/or ePUB format, as well as other popular books in Business & Agribusiness. We have over 1.5 million books available in our catalogue for you to explore.