One of the best illustrations of the complex and often contradictory story of Chinese economic development can be found in the automobile sector. Consuming about half the world’s oil, the highly capital- and technology-intensive automobile industry is among the most significant economic sectors at the global level. At national level, this sector often plays a critical role in domestic economies, as it typically comprises long and heavily interdependent supply and production networks, managed through intricate coordination systems. For developing countries, the prevalence of car use for personal transport is a good indicator of development, industrialization , and consumer purchasing power. All of these considerations ring true in the context of China’s economic transition.

The Rise of the Chinese Automobile Industry

China

is getting on wheels. In recent memory, for most Chinese bicycles were the mainstay of personal transport, but by the end of 2003 they were banned on

Shanghai’s main avenues to make way for the rapidly expanding ownership and use of cars. Over the past three decades, with unparalleled speed, China has emerged as the world’s largest producer and consumer of automobiles. During the planned-economy era, from the 1950s to 1980s, China’s total annual automobile output never reached more than half a million vehicles per year. A complete reversal of this trend took place in the 1990s, gathering pace towards the turn of the new millennium. As can be seen in Table

1.1, China’s automobile output increased almost 1400% in 16 years, from about 1.6 million vehicles in 1998 to about 23.7 million in 2014. As output accelerated, so China gradually moved up the rankings of global automakers, from tenth in the world in 1998, reaching the top five after China’s achievement of WTO

membership in 2001, and finally becoming the number one producer by 2009, when China’s output totaled about 14 million, almost equivalent to that of

Japan and the United States combined. By 2014, China’s leading global position was firmly fixed, with a total output of 24 million automobiles, more than double that of

the United States, and 2 million units ahead of the sum of the United States and

Japan .

Table 1.1World top ten automobile producing countries, 1998–2014

1 | USA | 12,006,079 | USA | 11,424,689 | USA | 12,279,582 | Japan | 11,484,233 | China | 13,790,994 | China | 23,731,600 |

2 | Japan | 10,049,792 | Japan | 9,777,191 | Japan | 10,257,315 | USA | 11,263,986 | Japan | 7,934,057 | USA | 11,660,702 |

3 | Germany | 5,726,788 | Germany | 5,691,677 | Germany | 5,469,309 | China | 7,188,708 | USA | 5,709,431 | Japan | 9,774,665 |

4 | France | 2,954,160 | France | 3,628,418 | France | 3,701,870 | Germany | 5,819,614 | Germany | 5,209,857 | Germany | 5,907,548 |

5 | Spain | 2,826,063 | Korea | 2,946,329 | China | 3,286,804 | Korea | 3,840,102 | Korea | 3,512,926 | Korea | 4,524,932 |

6 | Canada | 2,172,662 | Spain | 2,849,888 | Korea | 3,147,584 | France | 3,169,219 | Brazil | 3,182,923 | India | 3,844,857 |

7 | UK | 1,975,656 | Canada | 2,532,742 | Spain | 2,855,239 | Spain | 2,777,435 | India | 2,641,550 | Mexico | 3,368,010 |

8 | Korea | 1,954,494 | China | 2,334,440 | Canada | 2,629,437 | Brazil | 2,611,034 | Spain | 2,170,078 | Brazil | 3,146,386 |

9 | Italy | 1,692,737 | Mexico | 1,841,008 | UK | 1,823,018 | Canada | 2,572,292 | France | 2,047,693 | Spain | 2,402,978 |

10 | China | 1,627,829 | Brazil | 1,817,237 | Mexico | 1,804,670 | Mexico | 2,045,518 | Mexico | 1,561,052 | Canada | 2,394,154 |

Passenger cars, mostly sedan models, hold a unique position in the exponential growth of Chinese automobile production. Prior to the market reform , cars occupied less than 1% of total national output, which was overwhelmingly geared towards functional vehicles such as trucks. The balance began to tip in the late 1990s, as the domestic consumer market started to expand and passenger car output increased to about 30% of total automobile production. Over the next ten years, cars continued to gain prominence. By 2006, about 70% of Chinese automobile output was accounted for by passenger cars, reaching 84% in 2014. This shows the clear role of passenger cars in the recent development trajectory of China’s automobile sector.

The rise of the

Chinese automobile sector , particularly the production of passenger cars, is firmly linked to the integration of China within the globalizing economy and the concurrent transformation of domestic institutions resulting from the market

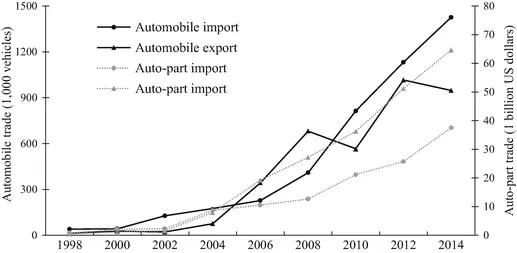

reform . The past three decades have seen China’s automobile sector become ever more closely integrated with the world automobile industry. China’s foreign trade in automobiles and automotive parts has been highly active since the late 1990s (Fig.

1.1). In 1998, auto-parts imports and exports amounted to less than US$ 1 billion in China, but had soared to about US$ 100 billion by 2014. Regarding trade in complete vehicles, in 1998 China imported about 40 thousand automobiles and exported about 14 thousand; by 2012, imports and exports had both increased to around 1 million units.

Behind burgeoning automotive foreign trade were large inflows of FDI

to the

Chinese automobile sector from international automakers (Table

1.2). Since the American Motors Corporation, later taken over by

Daimler Chrysler (DC) , set up China’s first

joint venture to produce jeeps in 1983, and

Volkswagen (VW) set up China’s first

joint venture for sedan cars in 1985, a succession of leading international automakers have swarmed into China. By 2004, major foreign manufacturers had mostly completed establishing their production arrangements in China. VW

and

General Motors (GM), being among the longest established investors in the Chinese auto sector, currently occupy the largest share of the market, though relative latecomers such as

Ford and

Toyota are fast catching up. Accompanying these foreign manufacturers were international suppliers, which followed on the heels of their clients to make inroads into the emerging Chinese market. Incoming international corporations greatly facilitated the integration of China’s automobile sector within global production networks.

Table 1.2Main assembly projects of transnational automobile corporations in China, 1983–2004

DC | ● | | | | | | | | | | ● |

VW | | ● | ● | | | | | | | | |

PSA | | ● | | ● | | | | | | | |

GM | | | | | | ● | | | | | |

Honda | | | | | | | ● | | | ● | |

Ford | | | | | | | | ● | | | |

Toyota | | | | | | | | | ● | | ● |

Hyundai | | | | | | | | | ● | | |

Kia | | | | | | | | | ● | | |

Nissan | | | | | | | | | | ● | |

BMW | | | | | | | | | | ● | |

From a domestic perspective, the development of China’s automobile industry was driven by the sweeping institutional transformations put in place by the market reform . China’s communist leaders had highlighted the importance of automobile production at the outset of the planned economy , considering the expansion of mechanized transport and related manufacturing capabilities indispensable to national industrializat ion. In consequence, the automobile industry was built as a national te...