UQAM - Universite du Québec à Montréal, Montreal, Québec, Canada

Keywords

Greek crisisDebt crisisMacroeconomicsMonetary union

End Abstract

Introduction

This chapter is about the crisis in Greece. It somewhat resembles the crisis in Italy in that both countries suffer from massive general government debt , well over 100% of GDP. It differs in that the debt in Greece is greater in proportion to GDP, and also in that the debt , consequence of decades of overspending, triggered the crisis. In contrast, the Italian crisis was provoked by the need to bail out several banks , even though Italy has had a high debt -to-GDP ratio for many years. Most treatments of the crisis in Greece recognize a period of enviable growth with the approach and advent of the euro , and then try to explain the crisis in spite of this growth , by recourse to the hostile business environment (scarce credit , byzantine regulations , unreliable juridical process, etc.) created by past governments and the influence of special interest groups over the use of funds. This chapter takes a slightly different approach. The hostile business environment had its most detrimental impact in the years of introduction of free trade with the rest of Europe by impeding business adjustment to the new environment. As a consequence, Greek manufacturers were unprepared for free trade, and could only compete by dropping prices , squeezing profits and their already weak capacity for investment . The reforms of the 1990–1993 government (spending cuts and deregulations) and those required for participation in the euro were too little, too late. The apparent improvement in performance with the onset of the euro is explained mostly by ballooning government expenditure that increased GDP and all measures that are GDP derived, such as productivity.

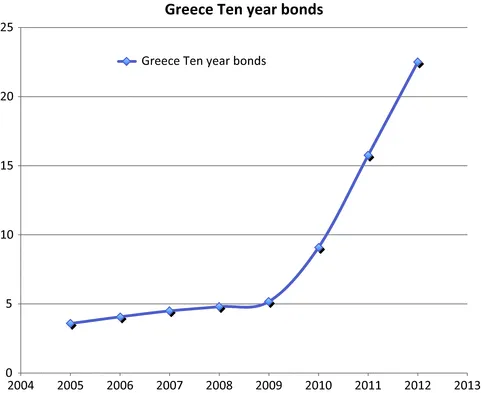

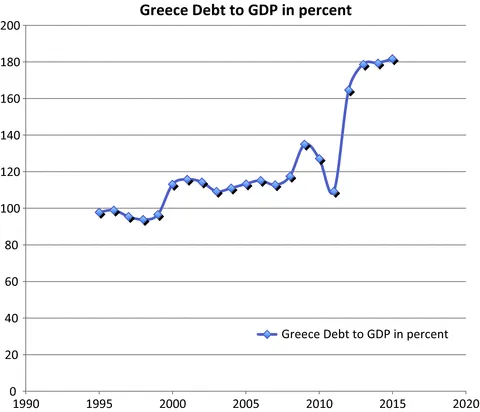

Interest rate variation revealed the financial crisis. The yield on ten-year Greek government bonds had hovered around 5% previous to 2008 and even had sunk as low as 3.2%. That rate began to rise at the start of 2010, reaching 38% in February 2012. Government debt as a ratio of the GDP varied around 100% from 1992 until 2008. Thereafter it soared, reaching 179% in 2016. If we take the maximum of both indicators, Greece would be paying over 80% of its GDP as interest on government borrowing. This is not the case, of course—the interest rate decreased and the debt was composed of bonds issued at different dates with varied interest rates . Nonetheless, it is obvious that Greece has been in financial crisis since at least 2010 (Figs. 1 and 2).

Fig. 1

Greece, long-term interest rates

Fig. 2

Greece, debt as percent of GDP

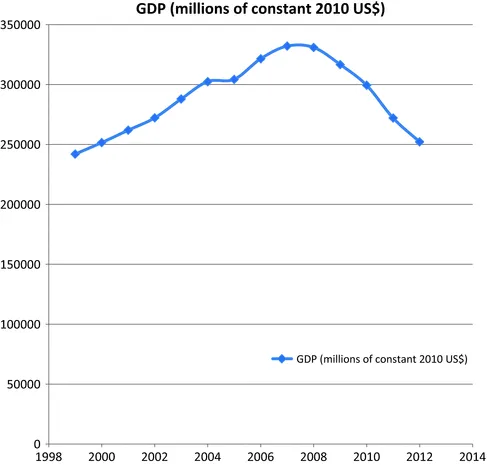

An economic crisis is associated with this financial crisis. This crisis came in part as a consequence of the austerity measures imposed upon Greece. After a near 40% increase in GDP from the year 2000 until 2007, Greece underwent a drop in this GDP from US$332 billion in 2007 to US$244 billion in 2013, a 26.5% drop. In parity purchasing power terms, giving a sense of the way the drop affected individual Greeks, the drop was from US$32,408 per capita in 2007 to US$24,159 in 2013, a drop of 25%. Of course, the impact of this difference was not uniform across the population (Giannitsis and Zografakis 2015), and those who were already tight for money, with less or no cushion to absorb the shock, were the hardest hit (Fig. 3).

Fig. 3

Greece, gross domestic product

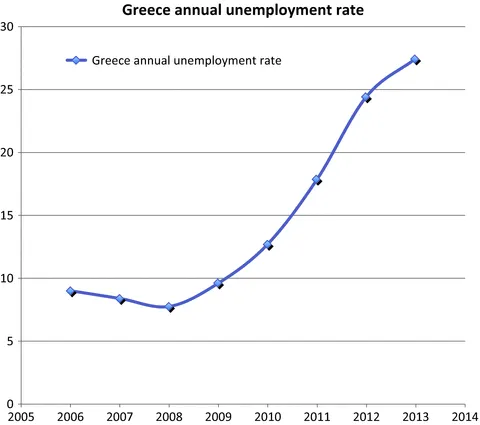

Another way to recognize the economic crisis in Greece is to look at unemployment figures. There was 8.6% unemployment in Greece at the end of 2008. By July 2013, the unemployment figure had reached 27.9%. A drop in the number of job vacancies accompanied this. In January 2009, there were a little over 50,000 job vacancies in all of Greece. By the end of 2012, there were fewer than 10,000 job vacancies. Again, the portion of the population gainfully employed dropped from a high of 63% in 2008 to 52.1% in 2012 (Fig. 4).

Fig. 4

Greece, unemployment rate

The data cited in this chapter should be interpreted even more sceptically than most, as they are somewhat distorted by at least two factors. First, to meet the European Standard of Accounts, revisions of statistics posterior to 1988 and then from 1960 to 1988 attempted to incorporate estimates for the informal economy, resulting in a discontinuity, ambiguity as to version of statistics...

Table of contents

Cover

Front Matter

Introduction: Europe, the Euro and a Crisis

A Financial and Economic Crisis in Greece

Ireland: From Prosperity to Crisis

Spain, the Euro and a Crisis

How Italy Experienced the Euro Crisis

Conclusion: The Crisis and Lessons for the Administration of the Euro

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Eurocritical by Roderick Macdonald in PDF and/or ePUB format, as well as other popular books in Economics & Economic History. We have over 1.5 million books available in our catalogue for you to explore.