eBook - ePub

Risk Management in the Polish Financial System

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Risk Management in the Polish Financial System

About this book

With globalisation comes an increase in the threat from systemic risk. As national economies become more globally entwined many argue that insufficient attention is being given to systemic risk; a principal contributor to recent economic crises. Focusing on the Polish financial system, this book addresses this critical issue within a global economic context. It advocates that accurate risk management practices and appropriate micro and macroeconomic policies can be created and maintained in order to manage systemic risk at both a national and international level. The book reviews current systemic risk management practices, analysing stability and existing micro- and macroprudential policies, before examining the current risks involved in investing in financial instruments and those associated with investing in stock exchanges. It offers suggestions for the effective implementation of a well-designed public policy, through well managed fiscal and monetary policies, and reflects the roles of households and companies in planning, organizing, and controlling socio-economic activity to control risk. Risk Management in the Polish Financial System aims to redefine the taxonomy of systemic risk, offering practical and regulatory socio-economic processes which can be applied to current risk management practices, as well as provide a risk map for the years to come.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

1

National Systemic Risk Management

Introduction

In order to manage systemic risk in an organization, such as a state, three points of reference must be established, that is a micro- organizational (households, companies), a macro-organizational (the state institutional system, the socioeconomic system of a country), and a mega-organizational one (global relationships). The most important in this case is the macro-organizational point, as looking at the executive of the state institutional system allows to assume a holistic perspective on risk within the framework of shaping the immediate systemic environment and neutralizing the threats posed by a distant systemic environment. In turn, any human activity, especially if related to trade, is connected with taking risks and the possibilities of incurring potential losses, particularly in legal and financial terms. There is also a global perspective on top of that, which should not only be taken into account but perpetually born in mind as it may pose both opportunities and threats. This is because every type of risk, systemic or incidental in nature, assumes its own significance or generates cyclical or stable costs that must be incurred in order to regain the efficiency of operation chiefly in economic terms.

The nature of any risk is always dynamic, irrespective of the fact that it might remain stable at some points in time. As far as management is concerned, it must first be identified, and subsequently its real or estimated weight must be defined, which will make regular control possible and allow the adoption of appropriate security measures. Next, human skills must be used in a broad-minded way and not merely on an individual, sector-, or department-based scale. Therefore, this chapter presents an introduction to the abundance of approaches that one might take to systemic risk, while at the same time showing how to achieve a compromise between exposition to risk and its aversion when it comes to decision-making.

1.1 Managerial grounds for risk and making strategic decisions

Although risk has existed on Earth since any human activity was first documented, regular academic interest in various categories of risk started to be evinced only in the early 20th century. A. Willett saw it as “the objectified uncertainty as to the occurrence of an undesired event. It varies with the uncertainty and not with the degree of probability” (Willet, 1951). In the seventies, risk and its management were directed at incidental and credit risks; in the eighties, market risk was added; and in the nineties, operational, strategic, and financial risks were also being developed (Cican, 2014, 280). If, in turn, we refer to the decision theory in its classical form, the greater the dispersion around the expected values of variance distribution of profit and loss, the higher the risk (Kubińska and Markiewicz, 2012, 45). Whereas risk management is intended to make people conscious of what risk is involved in a given activity so that it can be managed, from the perspective of an individual (household), a state institutional system, and a company, it is supposed to improve financial results and bring about conditions that will allow to keep loss at a level not higher than specified earlier (Dziawgo, 2011, 314). The best principle of risk management in history was written down in the Code of Hammurabi (about 1772 BC). It read, “If a builder build a house for some one, and does not construct it properly, and the house which he built fall in and kill its owner, then that builder shall be put to death” (Taleb, 2015, 244). The death penalty mentioned in this passage might as well be replaced by money damages, if its amount would in fact compensate for the incurred loss (although it is hard to claim that any amount of money could be a substitute for the life of a person).

Risk has many synonyms, and is interdependently related to many terms, such as chance (the positive aspect of risk), systemic risk (common for a given group), unique risk (specific), shock (negative or positive change that may be either evolutionary or unpredictable), exposure to risk (shocks and vulnerability to risk), susceptibility (to losses generated by negative shocks), resistance to shocks, crisis (emerging under the impact of the negative effects of risk), and uncertainty about the future (World Development Report, 2014, 61).

In general, risks may be categorized as follows:

a) according to the categories of decisions made for the purpose of achieving goals (risk as uncertainty with respect to future events or the outcomes of decisions), and the results brought about by those decisions may either be loss or profit,

b) according to the sources of risk (uncertain information or a decision made on the basis of a not optimal choice),

c) according to the manifestations of risk (deviation from the expected value of the goal that has been set),

d) according to probabilistic or statistical measures as the subjective probability of one-time events (including ones that have never taken place) (Tyszka and Zaleśkiewicz, 2010, 58–60).

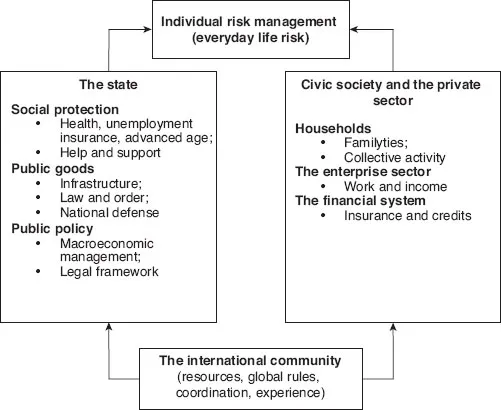

The risk involved in an individual’s actions is always to some extent dependent on the external environment and may be examined from the perspective of numerous overlapping correlations that eventually affect decisions (Figure 1.1).

In this system, an individual (a human being) will always receive the necessary support, starting from a household, which protects its members and has the possibility of making use of the combined total resources, through companies, which ensure income and allow the absorption of shocks, to the state, which, through to an institutional system, is capable of exerting local, national, or international influence and serves as the last resort in ensuring that the fundamental rights are observed (World Development Report, 2014, 19).

The dimensions of risk management, from the broad to the very specific ones, may be presented as follows (Improving the Management ... , 2011, 5):

a) risk management (organizational principles, effective risk prediction):

• placing an emerging strategy of risk management within the framework of organizational strategic decision-making,

• explaining the roles and responsibilities of the particular members of an organization.

b) risk culture (an active culture of risk management oriented at supervision, absorption, and assessment of information):

• developing incentives to exercise supervision and prizes,

• Removing barriers to becoming involved in supervision,

• adopting various points of view.

Figure 1.1 The influence of the socioeconomic system on individual risk management

Source: World Development Report, Risk and Opportunity – Managing Risk for Development, World Bank, Washington 2014, p. 19.

c) training and developing the potential for/capabilities of:

• supervising and scheduling/forecasting,

• informing about the problems that arise and holding a dialogue with the chief interested parties,

• working and cooperating with others for the purpose of understanding the problems and threats that arise.

d) adaptation planning and management (stress placed on communication and identification of risk):

• predicting and preventive preparation in case of adverse effects,

• drawing up of a list of options and priorities in order to ensure flexibility and a possibility to change a decision,

• formulating a strategy for resistance and response to the emerging threats.

As far as the economy is concerned, risk is an inscrutable factor, a random one, which is very often seen through the prism of the possibilities of stabilization and reduction across time by way of dispersion. However, not all such factors may be stabilized or dispersed, and reduction in the level of accompanying uncertainty may also have a merely subjective character, if there are no sufficient grounds for objective appreciation. The unexpected character of certain events is rather a consequence of insufficient knowledge on a given subject. But why is it that having, as we believe, quite extensive knowledge, we are still surprised by the lack of certainty, if we are empirically proven wrong (Hadyniak, 2010, 13–14)?

Since J. von Neumann and O. Morgenstern elaborated on the D. Bernoulli’s expected utility principle, this rule has governed decisions involving risk, as it offered guidelines on which path to choose. Further development of this theory on the basis of experiments that were conducted has led to the formulation of the so-called conventional theory (Kopańska-Bródka, 2012, 133–134). “These theories study the preference relationships inevitable to explain the sources of inconsistencies with the independence axiom. In such extensions, the axiom system of the theory of expected utility is accepted. However, the functional on a set of risky decisions is not an expected value but a decision-weighted transformation of the utility of possible outcomes. This new principle has not led to such inconsistencies as the principle of expected value maximization” (Kopańska-Bródka, 2012, 134). Nevertheless, even these theories did not prove quite useful, which led to the development of alternative theories known as unconventional ones as well as prospect, dual, or generalization theories. In general, each instance of strategic decision-making should be – from the point of view of the state or the market – dependent on the mutual infiltration and complementation of prescriptive and descriptive approaches (i.e., the so-called conventional and unconventional ones), which would mean taking into account individual reasonableness associated with the subjectivity of the act of making a choice (Kopańska-Bródka, 2012, 134, 146–147).

Therefore, a taxonomy of the threats and risks to macroeconomic growth, which must be taken into consideration when making strategic decisions, especially related to finances, includes the following units that may be examined from the perspective of insurance companies, corporations, financial risk managers, and political decision-makers (Coburn et al., 2013, 20–24, Coburn, 2014, 7–8):

a) financial shocks:

• market crash,

• insolvency and potential bankruptcy of a state,

• speculative (asset) bubbles,

• financial irregularities,

• run on banks, that is, a mass withdrawal of deposits from banks.

b) commercial disputes:

• labor dispute,

• trade sanctions,

• customs war,

• nationalization,

• collusion (e.g., between manufacturers with respect to product prices in a given year).

c) geopolitical conflict:

• conventional warfare,

• asymmetric warfare,

• nuclear warfare (local or global),

• civil war,

• influence of external forces.

d) political violence:

• terrorism,

• separatism,

• riots,

• assassinations,

• organized crime.

e) natural disasters:

• earthquakes,

• hurricanes/storms,

• tsunamis,

• floods,

• volcanic eruptions.

f) climate disasters:

• drought,

• freezing/low temperatures,

• the heat,

• atmospheric discharges (thunderstorms),

• tornado and hail,

g) environmental disasters:

• rise of the sea level,

• oceanic changes,

• atmospheric changes,

• pollution,

• fire.

h) technological disasters:

• nuclear disasters,

• industrial emergencies,

• infrastructural failure,

• technological incidents,

• cyber catastrophes.

i) epidemics:

• epidemics affecting humans,

• epidemics affecting animals,

• epidemics affecting plants,

• zoonoses,

• water epidemics.

j) humanitarian crises:

• famine,

• no access to water,

• refugee crisis,

• failure of or no social protection system,

• child poverty.

k) outer space:

• meteors,

• solar storms,

• satellite systems failures,

• ozone layer depletion,

• threats from the outer space.

l) other threats.

Such a multifaceted and multidimensional list of factors that is taken into account in risk management builds awareness that not only sector-related risks, which are characteristic for a given market segment or a broader socioeconomic structure, are important, but also the risks that seem far away.

A certain mood of the decision-maker can affect their decisions that are made in uncertain conditions. Research conducted by A. Bassi, R. Colacito, and P. Fulghieri demonstrates that even the weather can exert an influence on risk aversion. By affecting people’s moods, good weather encourages the taking of risk, while...

Table of contents

- Cover

- Title Page

- Copyright

- Contents

- List of Figures

- List of Tables

- Preface

- 1 National Systemic Risk Management

- 2 Stability of the Polish Financial System and the Risk Involved

- 3 Management of Financial Stability Risk

- 4 The Risk of Investing in Financial Instruments

- 5 Strategic Risks of Investing in Stock Exchange

- References

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Risk Management in the Polish Financial System by Marian Noga,Konrad Raczkowski,Jarosław Klepacki in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.