This book examines the uneven economy in Asia, showing how the pace of economic transformation affects prosperity and the emerging middle class. Using the Lewis turning point and the long run cycle of the rise and fall of nations as a framework, it demonstrates how demographic trends, digitizationrates and consumer preferences creates business opportunities in a disruptive and uncertain world. This includes moves toward promoting Eurasian integration, restructuring of state-owned enterprises, green economy, and the digital economies – ecommerce, fintech and sharing economy. Vanity capital, longevity and leisure economies are also discussed. The author explains what drives creative disruption, technical innovation and their effect on manufacturing, consumers, businesses, and sustainability. It is essential reading for students, academics, executives, and business persons wanting in-depth coverage of the economic landscape in Asia.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Pongsak HoontrakulEconomic Transformation and Business Opportunities in Asiahttps://doi.org/10.1007/978-3-319-58928-2_1

Begin Abstract

1. Asia’s Economic Transformation in a Disruptive and Uncertain World

Pongsak Hoontrakul1

(1)

Vimanmak Noi Co., Ltd, Bangkok, Thailand

End Abstract

Introduction

Asia is increasingly becoming the world’s epicenter of economic growth and value creation. As Asians live longer and prosper, the demand and supply of health, well-being, and happiness underlie Asia’s new wealth-generating model, a break from the old export model. In a world still recovering from the 2008 global financial crisis , governments and businesses must understand these dynamics if they are to form impactful public policies and multiple-year growth strategies.

The world economy comprises essentially four components: economic agents (producers, consumers, organizations, government), structure (production, distribution, and consumption ), goods, and services. The old economy system revolves around allocating scarce resources – land , labor , and capital. The entrepreneur exploits comparative advantages across boundaries, producing goods and services cheaply in one place and selling them at higher prices elsewhere until there is no feasible productivity gain. This value creation is a diminishing return to scale.

In the new economy , resources and values are redefined and seemingly abundant. Technological advances like automation , innovations like niche markets , and intellectual property like software applications are the new knowledge-based resources that are more valuable than the traditional resources of land , labor , and capital. Value creation in the new economy is increasing return to scale, where the variable cost of producing another unit approaches zero, as in copying digitalsoftware .

There have been many examples in history of seminal changes disrupting the global economy, such as rail and electricity. Many structural disruptive forces are at work now. With its billion-plus population, China presents threats (and opportunities) to many global industries in the short to medium term. So does India in the long term. Donald Trump’s election as US president in November 2016 has presented disruptive strategic threats (and opportunities) to Asia and the rest of the world, including his stated desires to reverse the globalization and environmental policies of his predecessor, Barack Obama.1 Many technological innovations from the sharing economy to the Internet of Things (IoT) disrupt the status quo by offering new, better, and cheaper products and services. Regulatory changes create big headwinds (and tailwinds) for traditional industries like banking, energy, automobiles , andhealthcare .

Economic transformation will diverge in different Asian countries because of their different starting points, technology gaps, and degrees of institutional rigidities. According to the Lewis Turning Point (LTP) concept, economic development begins with an agriculture-based economy, transits to higher productivity manufacturing , and then high-value service-oriented sectors.

Asia’s economies have undergone tremendous structural transformation from rural agriculture bases to urban industrial bases over the past half century. And Asia’s share of global economic production has doubled. But the benefits have been unevenly distributed. Japan , South Korea , Taiwan , and Singapore have become high-income industrialized nations. China , Thailand , and Malaysia are still trapped in middle-income status with dual economies, a mix of rural agriculture and urban manufacturing . Other countries like India, Indonesia , Vietnam , and Myanmar are still low-income economies in the early stages of industrialization with lopsided agricultural bases. Different degrees of economic transformation present diverse business opportunities. Two-speed economies – pre- versus post-LTP, rural versus urban, low versus higherincome – will be discussed throughout this book.

Unlike the market-based system , the state-owned economic system produces goods and services according to a centralized hierarchical command. Inefficiencies and shortages are common because resource allocations are not based on supply and demand through the pricing mechanism. Transforming these state-owned enterprises (SOEs) into market-based enterprises will usually increase productivity , transparency, and commercial space for sustainable economic growth.

The Global Macroeconomic Setting

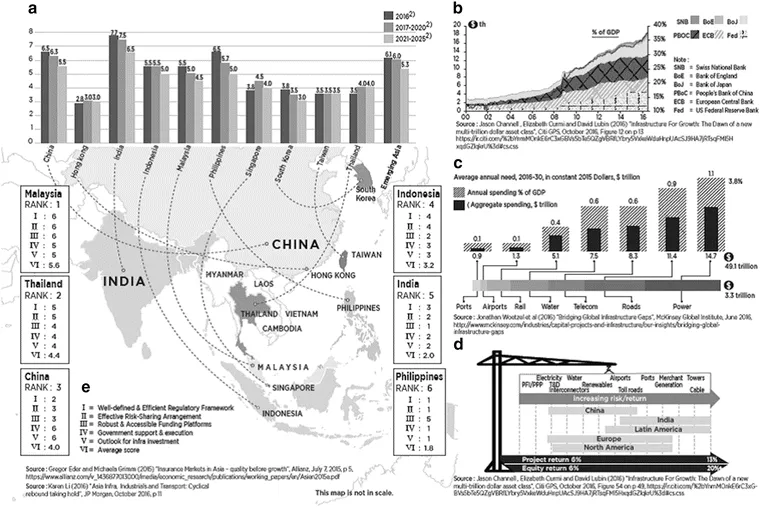

The world economy has been trapped in subpar growth and low inflation since the trough of the global financial crisis a decade ago.2 Current projections for global real GDP are 2.6 percent for 2016 and 2.8 percent for 2017 with moderate prospects of inflation .3 In Asia, strong growth in India and the 10 countries of the Association of Southeast Asian Nations (ASEAN) partially offsets the weakness in China . As shown in Fig. 1.1a, India is projected to lead Asia with over 7.5 percent annual growth from 2016 to 2020 while China and Malaysia will slow down. Asia will lead the world with a projected 6 percent annual GDP growth in 2016–2020. And the gap with the rest of the world is widening.4 Asia’s two closest competitors, Latin America and Eastern Europe , will grow at only half that pace.5

Fig. 1.1

(a) Growth rates in emerging Asia 2016–2025. (b) Aggregate balance sheet of large central banks ($trn and % of GDP). (c) Projected global infrastructure needs from 2016 to 2030. (d) Relative risk and indicative return ranking by industry and region. (e) PPP Scorecard in selected Asian nations

Weak oil and commodities prices, ultra-low interest rates, and increased fiscal spending have not boosted the global economy back to pre-2008 levels.

First, this is partially due to persistent deleveraging in the private sector debt overhang in the advanced economies after years of plentiful liquidity and asset reflation. On aggregate the world is wealthier from asset reflation by massive “quantitative easing” (QE) policies. Worldwide private financial assets...

Table of contents

Cover

Frontmatter

1. Asia’s Economic Transformation in a Disruptive and Uncertain World

2. Life Under the “New Normal”

3. Asia’s Vanity Capital

4. Asia’s Longevity Economy

5. Asia’s Leisure Economy: Creating Economic and Social Value

6. Government Initiative Drive I: Connecting the Region, Building Infrastructure and Cities

7. Government Initiative Drive II: Public DebtDebt

public debt

public assets/public propert/ public wealth

Reform

, Public Wealth, and State Enterprise Reform

8. Asia’s Digital Economy

9. Asia’s Low-Carbon Economy

Backmatter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Economic Transformation and Business Opportunities in Asia by Pongsak Hoontrakul in PDF and/or ePUB format, as well as other popular books in Business & Business General. We have over 1.5 million books available in our catalogue for you to explore.