Interchange fees have been the focal point for debate in the card industry, among competition authorities and policy makers, as well as in the economic literature on two-sided markets and on the regulation of market failures. This book offers insight into the economics of interchange fees. First, it explains the nature of two-sided markets/platforms/networks and elaborates on four-party schemes and on the rationale behind interchange fees according to Baxter's model and its later refinements. It also includes the debate about the optimum level of interchange fees and its determination ("tourist test"), and presents the original framework for assessing the impact of interchange fee regulatory reductions for the market participants: consumers, merchants, acquirers, issuers, and card organisations. The framework addresses three areas of concern in reference to the transmission channels of interchange fee reductions (pass-through) and the card scheme domain (triangle: payment organisation, issuer, acquirer). The book discusses the effects of regulatory interchange fee reductions in Australia, USA, Spain, and, most specifically, Poland. It will be of interest to policy makers, card and payments industry practitioners, academics, and students.

Two-sided marketsNetwork effectFour-party card schemeWelfareConsumerMerchantTourist test

End Abstract

This chapter consists of two parts. Part I describes two-sided markets, thus providing the background knowledge needed to understand the implications of four-party card schemes formed in a two-sided network. Part II deals with interchange fees in card payments . Interchange fees as well as other fees applicable in four-party card schemes are thoroughly discussed.

1.1 Introduction to Two-Sided Markets

This part introduces the concept of two-sided markets, also called two-sided platforms or two-sided networks in the economic and information technology literature. Section 1.1.1 shows the value of platforms connecting specific groups of agents having interrelated interests. Two-sided platforms utilise indirect network effects . Section 1.1.2 gives multiple examples of two-sided platforms from different sectors of economy . It explains the business model and the pricing policy of platforms. This section sets out conditions defining two-sided markets. Section 1.1.3 addresses market imperfections which can arise in two-sided markets and make regulators act in defence of consumers and competition.

1.1.1 Indirect Network Effects in Two-Sided Platforms

The power of competition in a free market economy is based on the scale of interactions between entities . Trade in real economy benefits from the high number of sellers and buyers of goods and services . Similarly, free flow of capital in financial markets depends critically on the number of investors buying and selling securities in a free float. By matching buyers and sellers, platforms improve the market mechanism , because their operations reduce traditional transaction costs as defined by Williamson (2010). Platforms contribute to the ease of interactions, to lower search and bargaining costs and may decrease information asymmetries . A concentration of sellers and buyers can lead to lower prices and a greater overall efficiency of the system for the flow of goods and capital.

Many markets on which network externalities occur are classified as two-sided or even multi-sided markets . On two-sided markets, the interaction between two separate groups of entities takes place on a platform that serves as an intermediary and service provider. Entities of one group benefit from contacts with entities of the other group. The larger both groups and subsequently interactions (transactions) between both groups, the greater so-called indirect network effect , not to be confused with the direct network effect specific for interactions within a group, which is not a determinant of a two-sided market (Katz and Shapiro 1985).

The value of Android operating system has for its users comes from the number of apps offered by the developers on Google Play Store . The latter write apps for Android mobile platform because they hope to see their products reach many users. The larger both groups of entities , the greater the indirect network effect , i.e. the perceived value of Android platform among those writing and using native apps. Android also enables communication between app users, who can rate them, thus informing other people about their experience. Mutual communication and app rating represent a direct network effect , which has a positive impact on its value, but—as mentioned before—is not the essence of the two-sided market. The essence in this particular case is matching developers and users. Apple’s iOS operates exactly the same as Android, even if it forms a more closed ecosystem. Android and iOS are two global competing mobile platforms. They currently operate in duopoly and dominate the smartphone market. Payment apps of banks and non-bank FinTech (Financial Technology) innovative companies are written for those two mobile operating systems . Figure 1 schematically presents the concept of a two-sided market.

Fig. 1

Concept of a two-sided market. Note Agent A, B, …T—group one of agents (e.g. sellers); Agent 1, 2, …N—group two of agents (e.g. buyers)

(Source Own compilation)

In two-sided markets the demands of two groups of agents (entities) are interdependent. There can be usage or membership externalities . Payment card users care about the size of merchant acceptance network , not about how many card transactions merchants accept. In contrast, merchants prefer to join a card network in which cardholders actually use cards. From merchants’ perspective, what matters is card usage , not membership alone (Rysman 2009: 126).

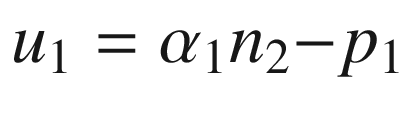

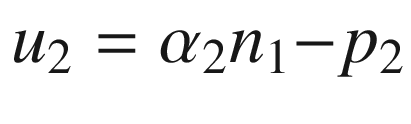

The theory of two-sided markets assumes that a platform’s utility depends on the number of network members on the other side of the market (indirect network effect ). Consequently, if a platform attracts n1entities in the first group and n2 entities in the other one, the utility of group 1 entity (u1) and of group 2 entity (u2) can be expressed as follows (Armstrong 2006: 672):

where p1 and p2 are prices charged by the platforms to both sides of the market, while α1 and α2 are parameters measuring the marginal benefit group 1 entity reaps from the interaction with group 2 entity (or conversely).

1.1.2 Business Model and Pricing Policy

Economists pay special attention to the platforms’ pricing policy . As observed by Rochet and Tirole (2003), and by many other economists who study this topic (e.g. Wright 2004a; Evans and Schmalensee 2005; Armstrong 2006; Hagiu and Hałaburda 2014), a two-sided market is one where the number and value of transactions depend on the structure and level of fees charged to both sides of the market. In a two-sided market, where indirect network effects occur, usually the price elasticity of demand varies between both groups of platform users. Therefore, one of them is charged transaction fees while the other one is provided with service below the marginal costs , and often incurs no transaction fees. In addition, the platform may charge both groups fixed fees for access to its services (membership/access fees). If entities from both groups are capable of internalising the indirect network effects by coordinating mutual activities, the two-sided market becomes a one-sided market . Rochet and Tirole (2006: 11–12) show that the four-party card payment system with an interchange fee can become one-sided when:

charges and benefits are passed through by issuers and acquirers to merchants and consumers ,

merchants charge to consumers two different prices for cash and card payments ,

merchants and consumers incur no transaction costs due to the system of double ...

Table of contents

Cover

Front Matter

1. Two-Sided Markets and Interchange Fees

2. Interchange Fee Reforms in Various Countries

3. Empirical Investigation of the Polish Interchange Fee Reform Effects

4. Final Remarks

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Interchange Fee Economics by Jakub Górka in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over one million books available in our catalogue for you to explore.