![]()

Part I

Become an Expert: Master the Five Golden Rules of Negotiation

When you have absorbed and implemented part I, you will be well on your way to being professionally equipped to handle commercial negotiations. It’s a fact that 95% of poorly negotiated deals end up that way because someone fails to abide by one of the five essential rules or his “crucial prerequisites.” The rules are simple, but essential, when you are preparing for and conducting face-to-face negotiations. They will protect you from the major errors that can cost you dearly when handling important business deals.

Look around you. Many people believe that they know these golden rules, but very few people have truly mastered them, even among the most senior managers in major corporations.

Mastering these five golden rules is the hallmark of the successful negotiator.

![]()

Chapter 1

The Crucial Prerequisite

Carl RITCHIE: I’m keen for you to explain your negotiating tactics to me.

Margaret PEAKE: My tactics…why?

Margaret Peake’s Office, 2 Years Earlier

Carl Ritchie is preparing to conduct some tricky negotiations. After discussions with senior management, it seems that the lowest price at which he can settle is $100, whereas the maximum price that he can reasonably quote at the start of the meeting is $110. So Carl Ritchie has quite a restricted “range.”

Margaret Peake does not beat about the bush:

Mr. Ritchie, you cannot be serious. You quote me a fantasy figure of $110, when currently the market price for such products is $98. You have a choice: Either you make me an offer very close to $98 or we are wasting our time.

Carl Ritchie is in trouble. The price quoted is below the minimum price that he agreed to with senior management. Should he give ground and accept $98? Or, despite everything, should he try to seal the deal at $100? But how? He feels that the buyer is dictating the terms and he is meekly following along.

In the Restaurant

Carl RITCHIE: It was awful, but what more could I have done?

Margaret PEAKE: Let us imagine that you are preparing for the same negotiation, but this time you set a specific target price, to take account of the market, your competitors, your production costs, and your sales policy.

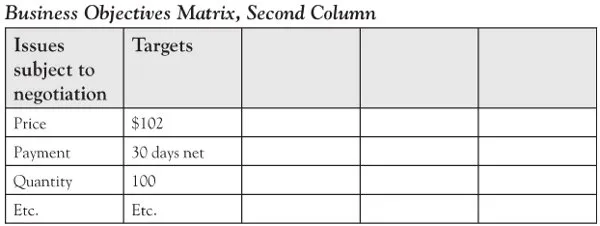

Carl RITCHIE: Let’s say, $102.

Margaret PEAKE: You tell yourself that it will not be easy, but that is your target outcome.

Carl RITCHIE: As usual, I also calculate a minimum price—for example, $100—and a maximum price that I could present at the start of the discussions—$110, for example.

Margaret PEAKE: Then let us imagine that I start the discussions with the same statement as before: “Mr. Ritchie, you cannot be serious. You quote me a fantasy figure of $110, when currently the market price for such products is $98. You have a choice: Either you make me an offer very close to $98 or we are wasting our time.”

Carl RITCHIE: Knowing that I’m aiming for $102 changes everything! It’s light years away from those awful negotiations!

Margaret PEAKE (amused): Really?

Carl RITCHIE: This time I don’t feel like I’ve been undermined. I know that my true target is to clinch a deal at $102. I have quoted $110, which is all part of the game. You have responded with $98—and that’s part of the game, too.

Margaret PEAKE: So what happens now?

Carl RITCHIE: I’ll gradually try to convince you to accept a price of $102 at the end of the negotiations.

Margaret PEAKE: You see, Carl, just by setting a precise target figure, this time you feel that you are in a much stronger position. You are fighting the buyer on equal terms.

Carl RITCHIE: In other words, you need to know what you want.

Margaret PEAKE: That is the crucial prerequisite for all successful negotiations.

The Crucial Prerequisite: Know What You Want

When you are faced with tricky commercial negotiations, you really must know how to establish your priorities and set your objectives. Here are a few practical tips to help you.

Prepare the Ground

This involves identifying all the components of the agreement that you are seeking and that may be negotiated. Generally the agreement will need to specify the following:

- Logistical factors: schedules, deadlines, transport, organization

- Technical factors: product and service specifications (main and secondary products/services)

- Legal factors: the nature of reciprocal undertakings, terms and conditions applicable in the event of subsequent disputes

- Financial factors: price but also method and terms of payment

- Commercial factors

It is important to take a broad view of the agreement in order to properly identify the principal aspects that are at stake as well as to anticipate additional issues that could be involved in the negotiations with your customer.

Rank Your Priorities

As we shall see in detail in a later chapter, you need to understand what the other party “really wants”: her true priorities, her major concerns, and her essential objectives. Likewise, you must analyze what is at stake in the negotiations for your own business: What, above all, are you seeking to achieve?

For a seller, one set of negotiations may be particularly important for the volumes that the deal will generate, another may be crucial because the deal will help the business develop fresh expertise, while another may help the business gain a foothold in a growth market. Indeed, protecting price levels is not generally a priority per se. When the seller wants to protect her price, she may have several very different priorities.

If her priority is to ensure that the contract is profitable, protecting price levels is not the only potential strategy. Depending on what the customer “really wants,” the seller may prefer to agree to a small price reduction offset by, for example,

- generating a much larger sales volume,

- identifying compensatory measures that generate savings (grouping orders and deliveries, simplification of a product or packaging).

If her priority is to avoid any “slippage” in the market and ensure the protection of a benchmark price levied on all customers, she may refuse to make any concessions on price but may, if necessary, grant her customer nonprice concessions such as cooperation agreements or extra services.

For a buyer, properly defining priorities is even more important, as you usually have a choice from among several suppliers who meet expectations to varying degrees. This can be difficult to achieve because there is a risk that unpleasant and unforeseeable surprises will arise during the purchasing process, and these are, by definition, almost impossible to assess in advance.

Particularly in diplomacy, excellent negotiators are characterized by their seeming flexibility on certain secondary issues as a counterweight to absolute firmness on key issues. It is therefore essential to know what the true priorities are—both the other party’s and your own. If everything is a priority, then you have no true priorities!

Ask yourself these questions:

- What is really important for me in these negotiations?

- What will enable me to say, a year from now, that I negotiated well today?

Do Not Make Do With a Price Range: Specify Precise Objectives

The Roman philosopher Seneca said, “There is no such thing as a favorable wind for those that do not know where they are going.” Thus, for each element of your proposal (price, volume, deadlines, etc.), you need to define precisely the figures you seek.

For the seller, this definition of objectives must be undertaken well before the offer is presented to the customer. This is a crucial point and the source of many errors in practice: Too often, the seller starts by making an offer, and only when faced with pressure from the customer does the seller wonder what he needs to achieve and where he can give ground. You need to reverse this logic and define precise objectives before you do anything else.

In certain sectors there is a tradition of laying out a suitable product or service offer according to the customer’s budget. Here we shall address the most common instance of this, the one where the supplier starts by establishing the product or service offer according to the customer’s needs—and then the price. For businesses selling simple, standardized, or commonplace products, the price may be determined by two criteria: production cost and knowledge of the prices charged by competitors.

Where more complex products or services are being sold, the price may also include the “perceived value” compared with competitors. For this, you need to identify your main competitors and collect and analyze as much objective data as possible to allow you to calculate

- the probable offer price level,

- the main strengths and weaknesses of that offer compared to the one that you are compiling.

It is then a case of quantifying the value of each relative advantage of your offer, as perceived by the customer. For example, during a particular set of negotiations, you might believe that a technical solution that can be implemented 2 months earlier might represent a perceptible advantage for the customer, amounting to some $200,000.

Likewise, you can quantify the perceived cost of each relative disadvantage of your offer compared with that of your main competitor.

Lastly, account needs to be taken of the “value added” that your customer may attach to one or other supplier for reasons of trust, perception, or relationship. The “perceived value” of the offer is therefore

estimated price of the leading competitor + estimated value of our offer’s relative advantages – estimated cost of our offer’s relative disadvantages ± difference in “value added.”

Naturally this “perceived value” plays only an indicative role. It must be compared with recorded market prices and with the business’s average selling price for comparable products or services in order to enable you to define your target price. You also need to study production costs thoroughly and examine the profitability of the transaction if it is completed at the “target” price.

A buyer also needs to define precise objectives. It is true that it is generally up to the seller to “reveal her hand” first. Furthermore, the objectives may also change depending on the information gleaned during negotiations (e.g., the appearance of new offers even more attractive than those anticipated). Yet knowing what you want is one of the keys to negotiating both a purchase and a sale.

Above all, you need to assess the overall consistency of negotiating objectives: Taking account of the other party and his expectations and considering the market, production costs, and your business’s policies, are your targets acceptable? Are they realistic? Do they form a consistent whole?

Do Not Confuse Targets With the Limit Points

Prepare yourself for the worst, including market conditions that are less favorable than anticipated and even stronger pressure than expected from your counterpart for terms lower than your specified targets. It is essential that you are clear about your limit points (commonly known as your bottom line). If you are not, you run the risk of agreeing to concessions in the heat of the moment that you will later regret. Thus, for each element of your offer, you need to determine acceptable limit points ...