- 220 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Advances in Management Accounting

About this book

Advances in Management Accounting (AIMA) is a publication of quality applied research in management accounting. The journal's purpose is to publish thought-provoking articles that advance knowledge in the management accounting discipline and are of interest to both academics and practitioners. The journal seeks thoughtful, well-developed articles on a variety of current topics in management accounting, broadly defined. All research methods including survey research, field tests, corporate case studies, experiments, meta-analyses, and modeling are welcome. Some speculative articles, research notes, critiques, and survey pieces will be included where appropriate.

Articles may range from purely empirical to purely theoretical, from practice-based applications to speculation on the development of new techniques and frameworks. Empirical articles must present sound research designs and well-explained execution. Theoretical arguments must present reasonable assumptions and logical development of ideas. All articles should include well-defined problems, concise presentations, and succinct conclusions that follow logically from the data.

Articles may range from purely empirical to purely theoretical, from practice-based applications to speculation on the development of new techniques and frameworks. Empirical articles must present sound research designs and well-explained execution. Theoretical arguments must present reasonable assumptions and logical development of ideas. All articles should include well-defined problems, concise presentations, and succinct conclusions that follow logically from the data.

Trusted by 375,005 students

Access to over 1 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

CHAPTER 1

CHANGES IN COST SYSTEM DESIGN AND INTENSITY OF USE IN TIMES OF CRISIS: EVIDENCE FROM DUTCH LOCAL GOVERNMENT

ABSTRACT

Purpose: This study examines whether changes in environmental and funding uncertainty during the first three years after the outbreak of the global financial crisis (which we presume to have increased significantly) are associated with changes in cost system design and intensity of use.

Design/methodology/approach: A dataset of survey responses from 56 Dutch municipalities is used for the empirical analyses. In the questionnaire, a senior-level financial manager reflected on the changes that he or she had perceived during the three years prior to the study (which was conducted at the end of 2010).

Findings: The results show that during these years, on average, environmental and funding uncertainty have indeed significantly increased, whereas cost system design and intensity of use have shown little change. The results further indicate that change in environmental uncertainty is positively related to changes in cost system complexity and cost system inclusiveness for activities and/or programs, whereas change in funding uncertainty is positively related to change in cost system intensity of use for product costing purposes. Also, change in cost system complexity is positively related to changes in cost system intensity of use for both operational control and product costing purposes.

Originality/value: Whereas previous large-scale research tends to focus on how the level of cost system design and/or intensity of use characteristics is related to the level of contextual factors, this study focuses on how changes in cost system design and intensity of use characteristics are related to changes in contextual factors. Also distinctive is that this study focuses on local government organizations experiencing a fiscal crisis.

Keywords: Management accounting change; cost system design; cost system intensity of use; uncertainty; local government; fiscal crisis

INTRODUCTION

To date, our knowledge about the design and use of cost systems in public sector organizations operating in “normal” circumstances is limited (e.g., Geiger & Ittner, 1996), and we know even less about this (and many other accounting) topic(s) in times of crisis (Bracci, Humphrey, Moll, & Steccolini, 2015). To extend this knowledge, this study focuses on changes in the design and use of cost systems in Dutch local government, which are the core part of their administrative systems that provide financial information to the municipal managers and decision makers, during the first three years after the outbreak of the global financial crisis. It follows the contingency-based literature on management accounting and control systems (MACSs), in assuming that in order to be effective, an organization’s MACSs have to be aligned with the nature of its internal and external environment. Here we focus in particular on changes in the level of environmental and funding uncertainty because we expect these two factors to be (most) highly affected by the current fiscal crisis that has resulted from the recent global financial and economic crisis (Kickert, 2012; Janke, Mahlendorf, & Weber, 2014), and because contingency-based research, on which we strongly build when developing our hypotheses, has shown that the level of uncertainty that an organization is (perceived to be) confronted with has a large impact on the design and use of MACSs (Chenhall, 2003; Otley, 2016).1 We explicitly focus on both environmental and funding uncertainty, given that, whereas these two types of uncertainty are typically closely related in private sector organizations, this is mostly not (or at least not as much) the case in public sector organizations. In general, contingency-based research suggests that when environmental and funding uncertainty increase, organizations use more sophisticated cost systems and make more intensive use of cost information for managerial decision-making purposes (e.g., Khandwalla, 1972; Gordon & Miller, 1976; Al-Omiri & Drury, 2007). These relationships have mostly been studied and found in studies of private sector organizations operating in “normal” circumstances, however, and may not (fully) apply to public sector organizations and/or times of crisis.

This study thus aims to examine whether changes in environmental and funding uncertainty during the first three years after the outbreak of the global financial crisis are associated with changes in how cost systems are designed, and in how intensively these systems are used for different purposes. Our overall objective is to examine how different types of uncertainty, cost system design, and cost system intensity of use evolve and co-evolve over time, in particular among local government organizations experiencing a fiscal crisis. A dataset of survey responses from 56 Dutch municipalities is used for the empirical analyses. We believe that Dutch local government provides an ideal setting for our study because changes in financial reporting regulations in 2003 have provided more autonomy for Dutch municipalities to design their cost system. Due to this change in autonomy, we are able to assess whether simultaneous changes in cost system design and intensity of use have occurred as a response to (presumably significantly) increased levels of environmental and funding uncertainty during the crisis in a substantial number of organizations. Also, the fact that these organizations share many similarities (e.g., in terms of task characteristics and technology; cf., Johansson & Siverbo, 2014) provides some natural control against omitted variable bias. We follow the approach of Baines and Langfield-Smith (2003) by asking our respondents to reflect on the changes they had perceived during the three years prior to the study (which was conducted at the end of 2010).2 We focus on a three-year time frame because it seems reasonable for the relationships that we focus on and the fact that we have no strong a priori theory or empirical support to predict another particular time frame. Underlying the study is a research model that basically assumes that changes in cost system design are related to changes in the context in which the cost system is being used, and that both are related to changes in how intensively the cost system is used within that context.

This study aims to contribute to the literature on the design and effectiveness of cost systems in at least two ways. First, whereas previous large-scale research tends to focus on how the level of cost system design and/or intensity of use characteristics is related to the level of contextual factors, our study focuses on how changes in cost system design and intensity of use characteristics are related to changes in contextual factors. We examine both the extent to which there have been, as well as associations among, changes in the design and intensity of use of cost systems, and in the context in which these systems are being used. Moreover, different from related studies, which have mainly focused on rather broad conceptualizations of management accounting change, such as the number of changes (e.g., Libby & Waterhouse, 1996) and/or how these changes can best be classified (e.g., Sulaiman & Mitchell, 2005), our study focuses on changes in specific cost system design and intensity of use characteristics. Second, whereas previous large-scale research in this area tends to focus on private sector organizations operating in “normal” circumstances, our study focuses on local government organizations experiencing a fiscal crisis. As such, our study is conducted in a different setting and during a special time period and provides new insights into how the design and intensity of use of cost systems of governmental organizations change in response to changes in environmental and funding uncertainty. Although some of the relationships examined in this study have been studied before, only a few prior studies have done so in public sector organizations, and none has done so in terms of changes and/or in times of crisis.

The remainder of this chapter is structured as follows. Section 2 discusses background and hypothesis development. Section 3 describes the research methods. Section 4 presents and discusses the results. Finally, Section 5 summarizes and concludes the study.

BACKGROUND AND HYPOTHESIS DEVELOPMENT

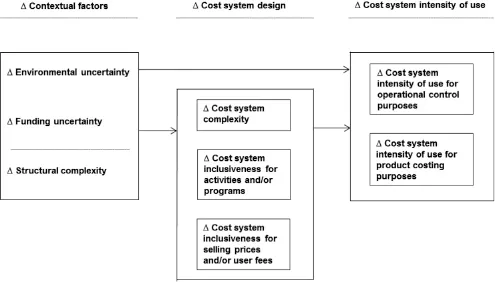

Fig. 1 shows the conceptual research model describing the variables and the relationships examined in this study.3 In the following subsections, we first provide background on Dutch local government, and then review the literature and develop our hypotheses.4

Background on Dutch Local Government

Dutch Local Government and the Fiscal Crisis

In the Netherlands, municipalities are considered the most important and visible level of subnational government in the Dutch decentralized unitary state (Hendriks & Tops, 2003). They are rather autonomous in organizing their business operations, and central government funding is by far their most important source of income. This funding is effectuated via specific and general grants. Specific grants are earmarked revenues meant to finance (most of) local governments’ duties imposed by the central government and are based on the specific cost drivers of the activities performed. General grants are not earmarked and come from the municipal fund, which allocates the available resources among all municipalities. Since the amount of the municipal fund depends upon the central government’s expenditures (this is called the “go upstairs, go downstairs” approach), the exact amount of this fund is unknown until about two years after each budget year. As their income from the municipal fund covers approximately one-third of their expenditures, this delay (always) causes considerable uncertainty for the municipalities. Similar to governmental organizations in many other Organisation for Economic Co-operation and Development (OECD) countries, Dutch municipalities are strongly impacted by the current fiscal crisis. As a result, these organizations have to cut back expenditures, while at the same time the demand for (improved) public services continues (Pollitt, 2010). According to Kickert (2012), the recent/current global financial, economic, and fiscal crisis consisted of three stages: (1) the financial crisis, causing governments (in 2008) to save and support banks; (2) the economic crisis, causing governments (in 2009) to take economic recovery measures; and (3) the fiscal crisis of state debts and budget deficits, causing governments (from 2010 onwards) to take fiscal cutback measures. With hindsight, until the end of 2010, Dutch municipalities have been relatively sheltered from the crisis, in the sense that the central government did not reduce its funding to the municipalities.

Fig. 1. Conceptual Research Model.

In the course of 2010, this situation changed dramatically. In April of that year, a working group of Dutch public officials, appointed to consider possible cutback measures for the central government, proposed to reduce the municipal fund by 1.7 billion euros, about 10% of its amount, after a period in which it had been relatively stable, in terms of level and structure, for a number of consecutive years (Ministry of Finance, 2010). In the coalition agreement of the new cabinet that came into office in October 2010, it was announced that this cabinet intended to lower the municipal fund considerably. This would mainly be done by re-implementation of the “go upstairs, go downstairs” approach. Due to the crisis, this approach was not followed during the years 2009–2011, but the coalition intended to use it again from 2012 onward. The negative financial effect of this measure was first c...

Table of contents

- Cover

- Advances in Management Accounting

- Chapter 1: Changes in Cost System Design and Intensity of Use in Times of Crisis: Evidence from Dutch Local Government

- Chapter 2: Beyond Budgeting: Distinguishing Modes of Adaptive Performance Management

- Chapter 3: Assessing the Main and Interactive Effects of Activity-Based Costing and Internal and External Information Systems Integration on Manufacturing Plant Operational Performance

- Chapter 4: An Exploratory Investigation of Management Accounting Service Quality Dimensions Using Servqual and Servperf

- Chapter 5: Learning from the Experience of Others: Lessons on the Research–Practice Gap in Management Accounting – A Nursing Perspective

- Chapter 6: Performance Changes Over Difficult Times for the Banking Sector: A Branch Level Study

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Advances in Management Accounting by Mary A. Malina in PDF and/or ePUB format, as well as other popular books in Business & Accounting. We have over one million books available in our catalogue for you to explore.