This joint publication from the Asian Development Bank and the Asian Development Bank Institute features selected papers from the September 2009 conference on the social and environmental impact of the global economic crisis on Asia and the Pacific, especially on the poor and vulnerable. The publication is designed with the needs of policy makers in mind, utilizing field, country, and thematic background studies to cover a large number of countries and cases. This publication suggests that the crisis is an opportunity to rethink the model of development in Asia for growth to become more inclusive and sustainable. Issues that need to be more carefully considered include: closing the gap of dualistic labor markets, building up social protection systems, rationalizing social expenditures, addressing urban poverty through slum upgrading, promoting rural development through food security programs in pro-poor growth potential areas, and concentrating climate change interventions on generating direct benefits for the environments of the poor.

eBook - ePub

Poverty and Sustainable Development in Asia

Impacts and Responses to the Global Economic Crisis

- 542 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Poverty and Sustainable Development in Asia

Impacts and Responses to the Global Economic Crisis

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

The impact of the world recession on Indonesia and an appropriate policy response: Some lessons for Asia

Introduction

This chapter examines the impact of the global recession on Indonesia, the largest country in Southeast Asia. The chapter examines the impact on unemployment and the policies that have been utilized by the government to minimize the impact of the recession. The chapter concludes with a section on lessons for other Asian countries.

1. The recession and Indonesia—A surprisingly small macroeconomic impact

In the early stages of the global recession,3 it was feared that Indonesia would be hard hit. Export earnings were expected to decline by 30% or $30 billion–$40 billion, which would be a loss of 7.5%–10.0% of national income. Add declining remittances and tourist income, and a sharp decline in expected foreign private investment, and the direct cost of the recession was expected to be a more than 10% decline of national income.

Indirect costs, as the impact worked its way through the economy, would nearly double that (a “multiplier” of 1.8–2.0). The direct and indirect costs of the world recession on an initial analysis therefore were estimated to result in a horrific decline of 15% or more in gross domestic product (GDP).

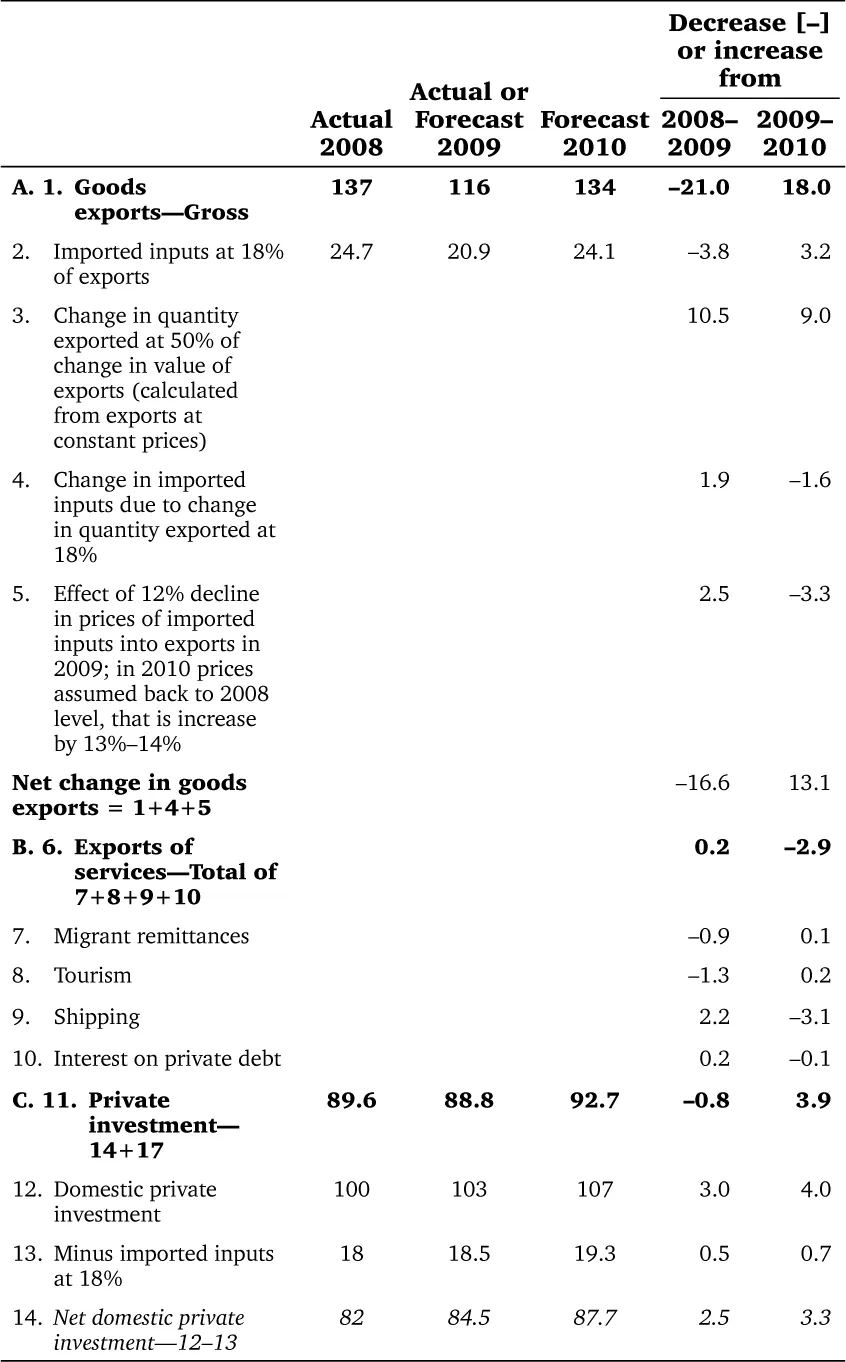

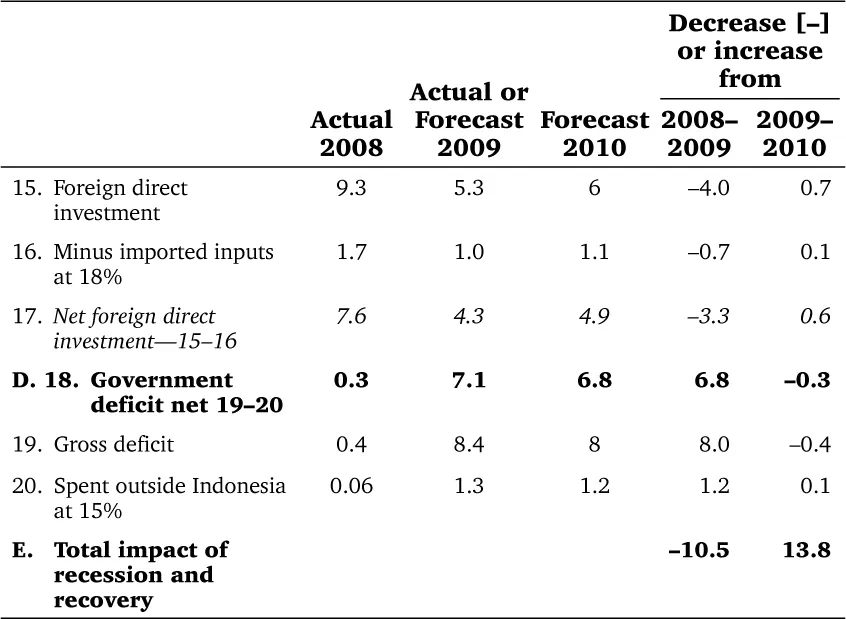

However, these estimates ignore the offsetting benefits of the recession (and the costs of the subsequent recovery). Table 1 indicates all the international variables to be taken into account. It demonstrates the importance of systematically evaluating the impact of the recession (or other changes in the world economy) through all the channels connecting Indonesia to that economy.

Table 1: Direct impact of the world economic recession on Indonesia—Summary ($ billion, rounded)

Note: Annual data for most items under B and C for 2009 are not yet available. Fourth quarter is an estimate.

Sources: Authors’ calculations, using Statistics Indonesia (BPS) data compiled by the World Bank for goods exports and imports; Bank Indonesia data for services and investment; and Ministry of Finance data for government.

The decline in prices in the world market harms Indonesian exports, but it also has benefits of $14 billion due to lower prices for all imports. Other offsets to the cost of recession include:

• a reduction in needed imported inputs into exports, of $2 billion as exports decline;

• lower shipping costs for exports and imports;

• lower interest on the private debt; and

• a government deficit, augmented by a stimulus package, adding a further $7 billion to demand.

In sum, the net direct impact of the recession in calendar 2009 is $10 billion after offsetting direct gains against direct losses. However, use of annual data understates the impact of the recession. The Indonesian recession actually lasted from October 2008 to September 2009. During that 12-month period, the value of exports was down a further 6%, or $7 billion, compared to calendar 2009. For 2010, our very preliminary forecast, based on the improvement in the world economy, is for a net rise of $18 billion in export earnings. Other earnings, as from tourism and migrants, also increase. But in a mirror image of the decline during the recession, these increased earnings are partially offset by increased quantities of imports at higher prices, higher shipping costs, and a lower government deficit.

In addition to the direct effects, the indirect effects—the “multiplier”—must not be ignored. The size of the multiplier has not so far been estimated in Indonesia but that is no reason for ignoring it. Indirect losses occur as the direct losses work their way through the economy: as exporters and their workers spend less, sales and production decline throughout the economy. To take account of these second-and third-round effects (and so on), one needs to use an input–output table, plus an estimate of the leakages that eventually stop the effects from cumulating endlessly in the economy. The results for 2010 are in Table 2. (Similar calculations were made for 2009 and are available from the authors.)

Table 2: First attempt at an aggregate open economy income generation model for Indonesia: Forecast for 2010. The recovery from the impact of the world economic crisis 2008–2009

Sources: Prepared by Daniel M. Schydlowsky using the following references: Schydlowsky, D. M. 1980. A Short Macro-Economic Model of the Indonesian Economy. In Gustav F. Papanek, ed. The Indonesian Economy. New York: Praeger; Schydlowsky, D. M. and Martha Rodriguez. 1982. The Vulnerability of Small Semi-Industrialized Economies to Export Shocks: A Simulation Analysis Based on Peruvian Data. In M. Syrquin and S. Teitel, eds. Trade, Stability, Technology, and Equity in Latin America. New York: Academic Press. pp. 125–141.

The multiplier of indirect effects is 1.85, nearly doubling the direct effects. But because of lower world prices in 2009, Indonesia spends less on imports, becoming more self-reliant and less trade-dependent. As a result, the multiplier measuring indirect effects increases to 1.94 during the recession. There are also indirect gains, primarily lower prices for imports of consumer and capital goods.

After systematically taking account of all gains and losses for 2009, we see a reduction of just $6 billion in income, equal to a 1.4% reduction in the GDP growth rate. As growth in 2008 was 6%, after a 1.4% loss, growth is forecast to be roughly 4.5% in 2009, consistent with other growth estimates. This means that the Indonesian economy would still be growing despite the recession—a far cry from the first estimate of a decline of as much as 10% in the economy, made because it failed to take account of offsetting benefits.

By the fourth quarter of 2009, Indonesia was coming out of the recession. It lasted just a year. Just as the decline was moderate, and substantially driven by declining demand for Indonesia’s exports, so will the recovery be, in our forecast: moderate and substantially driven by increased income from exports. And the change in export earnings was primarily commodity driven: 85% of the decline in exports was due to lower prices and, in most cases, lower quantities exported of commodities. The increase in exports in the last quarter is even more dominated by commodities (92%). Under current policies, Indonesia is therefore highly dependent on the vagaries of the world commodity market and the change in prices that prevails there. If prices continue to rise for copper, coal, and palm oil, Indonesia will continue to grow at a good pace; if commodity prices falter, so will the Indonesian economy.

Indonesia has weathered the recession well, largely explained by the following factors:

• It is well known that Indonesia is less trade dependent than many economies in Asia, as well as less remittance and tourism dependent than some. Rather, the primary source of growth of Indonesia’s GDP since 1997 has been domestic consumption.

• Macroeconomic management was good: some effective stimulus was applied and the political environment has been stable.

• The banking system, chastened somewhat by the disaster of 1997–1998, was in fair shape and continued to lend, although there were initial problems with trade finance.

• The government provided a proper response to the recent crisis by focusing on maintaining market confidence through prompt actions including:

2. Aggravation of unemployment and underemployment

Despite macroeconomic success, the problem of unemployment and underemployment, which had plagued Indonesia since the monetary crisis of 1997–1998, worsened as a result of the recession.

Few “real” jobs added since 1997

Because Indonesian growth was less export-dependent than other countries, it was less vulnerable to the worldwide recession. But the slow growth of manufactured exports and the stagnation of labor-intensive manufactured exports since 1997–1998 meant that there was little demand for additional labor. From 1997 to 2008, roughly 22 million were added to the labor force, but only an estimated 5.6 million workers have found real, productive jobs (Table 3).4

Table 3: Employment, unemployment, and disguised unemployment (millions of workers)

Change (million) | 1985–1997 | 1997–2008 |

Employed in manufacturing and constructiona | 7.5 | 2.5 |

Employed in transport, communication, utilities | 3.3 | 3.1 |

Able to obtain productive work (a) | 10.8 | 5.6 |

Agriculture | 1.7 | 5.5 |

Trade and services | 12.2 | 4.5 |

Added to work- and income-sharing or underemployed (b) | 13.9 | 10.0 |

Unemployed (c) | 2.3 | 3.1 |

Migrants—guesstimate (d) | 1.3 | 3.5 |

Total added to labor force (each period) (a+b+c+d) | 28.2 | 22.2 |

Added to unemployed, underemployed, migrants 1997–2008 (b+c+d) | 16.6 | |

Added to the labor force in 2009 and unlikely to a find job | 2.0 | |

Estimated job losses in labor-intensive exports alone | 0.4 | |

Estimated added to unemployed and underemployed, 1997–2009 | 19.0 |

a Includes mining, banking, and real estate.

Source: Authors’ calculations from Statistics Indonesia (BPS), Sakernas, various years.

Of the remaining 16.5 million, as a rough guess some 3.5 million found jobs abroad. Some 3 million were added to the unemployed, many or most from the middle class whose family could support them while looking for a “good” job.5 Those too poor to survive long without work may be temporarily unemployed but mostly crowded into work-and income-sharing occupations, with close to zero marginal labor productivity, to share in the income without adding much to output.6

Job losses and lack of job creation

The effect of the recession is likely to be that even fewer jobs than in the last decade will be created. Most of the 2 million who are joining the labor force every year will be underemployed. The decline in labor-intensive manufactured exports in four major industries (textiles, garments, footwear, and furniture) means that an estimated additional 0.4 million workers are losing their jobs.7 Other manufactured exports also declined in the first quarter of 2009 and are likely to add to the rolls of the underemployed.

This means that Indonesia is likely to enter 2010 with 15 million workers added since 1997 to those in the country who are not productively employed, with little value added to the country’s output and national income, without steady and decent jobs and reasonable income, many of them likely to be poor, and others vulnerable to falling into poverty at the slightest setback (Table 3).

Failure to create jobs since 1997

The failure of the Indonesian economy to create new productive jobs since 1997 is primarily due to stagnation in the export of labor-intensive manufactures, because Indonesia is no longer competitive in the world market for these goods.

Decline in labor-intensive manufactured exports

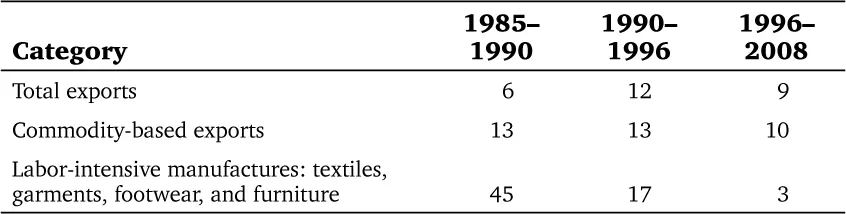

In the decade before the 1997–1998 crisis, Indonesia’s manufactured exports were growing at the strong rate of 30% each year, doubling every 2.5 years (Table 4). In the decade after that crisis, they grew at a slow 8%. What is worse for employment of the unskilled is that labor-intensive exports, which had also grown at 30% before 1997, stagnated at 3% a year since then.

Table 4: Annual growth in categories of exports, 1985–2008 (%)

Source: Authors’ calculations from Statistics Indonesia (BPS) compiled by the World Bank.

Before 1997, the larger firms in these industries had hired 1.4 million workers. Between then and 2008 they actually reduced their labor force slightly. When one adds jobs in larger firms in other industries, producing primarily for exports, and in smaller firms, an estimated two-thirds of the difference in hiring in manufacturing before and after the 1997–1998 crisis is due to manufactured exports.

Indonesia—A high-cost economy

A major reason for the failure to create many jobs is that Indonesia is a high-cost economy, which makes it difficult to compete in the world market. The main reasons are as follows.

Infrastructure is expensive, in part due to the costs imposed by multiple islands. This is one of the most neglected features of economic analysis of Indonesia. Interisland transport is the backbone that links activities in different regions, but transporting goods from production sites in Java to the outer islands, or vice versa, is not cheap. The consequence is limited integration in the domestic market, which slows growth in domestic demand.

High costs are also due to poor infrastructure quality. Infrastructure has long been inade...

Table of contents

- Front Cover

- Title Page

- Copyright Page

- Contents

- List of Boxes

- Preface

- Acknowledgment

- Overview

- The impact of the world recession on Indonesia and an appropriate policy response: Some lessons for Asia

- Impacts of the economic crisis in East Asia: Findings from qualitative monitoring in five countries Carrie Turk and Andrew Mason

- Social impact of commodity price volatility in Papua New Guinea Dominic Patrick Mellor

- Assessing social outcomes through the Millennium Development Goals Shiladitya Chatterjee and Raj Kumar

- The impact of the global economic slowdown on value chain labor markets in Asia Rosey Hurst, Martin Buttle, and Jonathan Sandars

- Global meltdown and informality: An economy-wide analysis for India—Policy research brief Anushree Sinha

- The social impact of the global recession on Cambodia: How the crisis impacts on poverty Kimsun Tong

- Women facing the economic crisis— The garment sector in Cambodia Sukti Dasgupta and David Williams

- No cushion to fall back on: The impact of the global recession on women in the informal economy in four Asian countries Zoe Horn

- Gender and social protection in Asia: What does the crisis change? Nicola Jones and Rebecca Holmes, with Hannah Marsden, Shreya Mitra, and David Walker

- The impact of the global slowdown on the People’s Republic of China’s rural migrants: Empirical evidence from a 12-city survey Xiulan Zhang and Steve Lin

- Urban–rural and rural–urban transmission mechanisms in Indonesia in the crisis Megumi Muto, Shinobu Shimokoshi, Ali Subandoro, and Futoshi Yamauchi

- The global financial crisis and agricultural development: Viet Nam Dang Kim Son, Vu Trong Binh, and Hoang Vu Quang

- Impact of the global recession on international labor migration and remittances: Implications for poverty reduction and development in Nepal, Philippines, Tajikistan, and Uzbekistan Andrea Riester

- Global crisis and fiscal space for social protection Armin Bauer, David E. Bloom, Jocelyn E. Finlay, and Jaypee Sevilla

- Addressing unemployment and poverty through infrastructure development as a crisis-response strategy Chris Donnges

- Fiscal space for social protection policies in Viet Nam Paulette Castel

- The global economic crisis: Can Asia grasp the opportunity to strengthen social protection systems? Mukul G. Asher

- Income support in times of global crisis: An assessment of the role of unemployment insurance and options for coverage extension in Asia Wolfgang Scholz, Florence Bonnet, and Ellen Ehmke

- Financial crisis and social protection reform—Brake or motor? An analysis of reform dynamics in Indonesia and Viet Nam Katja Bender and Matthias Rompel

- Reforming social protection systems when commodity prices collapse: The experience of Mongolia Wendy Walker and David Hall

- The impact of the global recession on the health of the people in Asia Soonman Kwon, Youn Jung, Anwar Islam, Badri Pande, and Lan Yao

- The impact of the global recession on the poor and vulnerable in the Philippines and on the social health insurance system Axel Weber and Helga Piechulek

- Implications of economic recessions on quality, equity, and financing of education Jouko Sarvi

- Impact of the global recession on sustainable development and poverty linkages V. Anbumozhi and Armin Bauer

- Green growth, climate change, and the future of aid: Challenges and opportunities in Asia and the Pacific Paul Steele and Yusuke Taishi

- Measuring the environmental impacts of changing trade patterns on the poor Kaliappa Kalirajan, Venkatachalam Anbumozhi, and Kanhaiya Singh

- Poverty, climate change, and the economic recession Benoit Laplante

- Alternative energy options of Asia in crises Kaoru Yamaguchi and Miki Yanagi

- Back Cover

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Poverty and Sustainable Development in Asia by Armin Bauer, Myo Thant in PDF and/or ePUB format, as well as other popular books in Social Sciences & Poverty in Sociology. We have over 1.5 million books available in our catalogue for you to explore.