The financial crisis has been blamed on reckless bankers, irrational exuberance, government support of mortgages for the poor, financial deregulation, and expansionary monetary policy. Specialists in banking, however, tell a story with less emotional resonance but a better correspondence to the evidence: the crisis was sparked by the international regulatory accords on bank capital levels, the Basel Accords.In one of the first studies critically to examine the Basel Accords, Engineering the Financial Crisis reveals the crucial role that bank capital requirements and other government regulations played in the recent financial crisis. Jeffrey Friedman and Wladimir Kraus argue that by encouraging banks to invest in highly rated mortgage-backed bonds, the Basel Accords created an overconcentration of risk in the banking industry. In addition, accounting regulations required banks to reduce lending if the temporary market value of these bonds declined, as they did in 2007 and 2008 during the panic over subprime mortgage defaults.The book begins by assessing leading theories about the crisis—deregulation, bank compensation practices, excessive leverage, "too big to fail, " and Fannie Mae and Freddie Mac—and, through careful evidentiary scrutiny, debunks much of the conventional wisdom about what went wrong. It then discusses the Basel Accords and how they contributed to systemic risk. Finally, it presents an analysis of social-science expertise and the fallibility of economists and regulators. Engagingly written, theoretically inventive, yet empirically grounded, Engineering the Financial Crisis is a timely examination of the unintended—and sometimes disastrous—effects of regulation on complex economies.

eBook - ePub

Engineering the Financial Crisis

Systemic Risk and the Failure of Regulation

- 224 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Engineering the Financial Crisis

Systemic Risk and the Failure of Regulation

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

Publisher

University of Pennsylvania PressYear

2011Print ISBN

9780812243574

9780812243574

eBook ISBN

9780812205077

1

Bonuses, Irrationality, and Too-Bigness: The Conventional Wisdom About the Financial Crisis and Its Theoretical Implications

By the end of 2010, six elements of conventional wisdom about the causes of the financial crisis had taken root:

1. The very low interest rates from 2001 to 2005 fueled a virtually unprecedented nationwide housing bubble in the United States.

2. Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs), helped cause the crisis by loosening their lending standards.

3. Deregulation of finance allowed the “shadow banking sector” to originate subprime loans and securitize them.

4. The compensation systems used by banks, especially the payment of bonuses for revenue-generating transactions, encouraged bankers to bet huge amounts of borrowed money (leverage) on the continuation of the housing boom by buying mortgage-backed bonds. The bankers would be richly rewarded if these bets paid off, but they would not be penalized if the bets went sour.

5. The bankers knew their banks were “too big to fail” (TBTF), and they invested recklessly because they were confident they would be bailed out if disaster struck.

6. Irrational exuberance led investors to buy securities backed by subprime mortgages, oblivious to the fact that when housing prices eventually declined, such mortgages would be likely to default.

In this chapter, we will confront the six items of conventional wisdom with hard evidence and, we hope, sound reasoning in order to clear the ground for our own argument: that, stripped to its essentials, the crisis was a regulatory failure in which the prime culprit was none of the usually targeted factors, but was, instead, the set of regulations governing banks’ capital levels known as the Basel rules.

When we began researching the financial crisis in the early months of 2009, we were driven by our dissatisfaction with the analyses then on offer. At the time, there were (understandably) only hypotheses that lacked evidence, and many of them, while equally plausible, contradicted each other. Additionally, there were more hypotheses than the six we have just listed, and partly as a result of the profusion of theories about the crisis there was also a widespread recognition that nobody had yet explained convincingly what had gone wrong. The extant paradigms of economics were found wanting, and fresh thinking was deemed not only possible but mandatory. This made the financial crisis not only an important topic because of the human tragedy to which it led, but an exciting field of research intellectually.

Very soon, however, politicians and political ideologues began to treat the hypotheses that confirmed their predilections as if they were established facts, and these theories eventually formed the conventional wisdom. Thus, conservatives were eager to blame the crisis on the government by means of hypotheses 1, 2, and 5, while liberals were eager to blame the crisis on capitalism by means of hypotheses 3, 4, and 6.

There were also scholarly forms of special pleading. Most of the academic commentary on the crisis has been written by professional economists, and for all practical purposes, the one weapon in professional economists’ armory is rational-choice theory. This amounts to saying that the one causal variable that economists are able to identify is the “incentive,” known to the rest of us as “the profit motive.” If an economic catastrophe occurs, then to most economists it must have been due to perverse incentives. Items 4 and 5, the bonus hypothesis and the TBTF hypothesis, fit the economists’ template perfectly: each theory posits an incentive for bankers to have engaged in reckless behavior so they could profit from it.

However, there has been a tendency to confuse the mere assertion that these incentives existed with a demonstration that they actually caused the crisis. Nobel laureate economist Joseph E. Stiglitz (2010b, 153), who embraces both the TBTF and the bonus hypotheses, writes without irony that “the disaster that grew from these flawed incentives can be, to us economists, somewhat comforting: our models predicted that there would be excessive risk-taking and short-sighted behavior, and what has happened has confirmed these predictions.” Even when Stiglitz wrote those words, however, evidence was already available that, as we shall see, seriously undermines the assumption that the disaster did grow from these flawed incentives.

The crisis has also provided grist for the mill of economists who would like to jettison the orthodox academic focus on the incentives faced by rational agents. These economists (e.g., Akerlof and Shiller 2009) have popularized the notion of irrational exuberance, hypothesis 6. Our objection to this hypothesis is that its misuse of psychologistic terminology has created the impression that there was something peculiarly emotional about the behavior that caused the crisis, even though there is evidence that bankers merely erred—not that they “went crazy.”

Our criticisms of the conventional wisdom may seem unfair. Journalists first popularized many of the dominant claims about the crisis, and under the pressure of deadlines they often have little choice but to repeat the pronouncements of experts and to draw on the analysis of ideologues. For this reason, journalism is usually seen as, at best, the first draft of history: in the long run, journalistic conclusions are supposed to be corrected and superseded by scholarship. The same process of correction and supersession is also, as Max Weber ([1918] 1946) reminded us long ago, the fate of all scholarly endeavors. As the hasty pronouncements about the financial crisis that have been made by many journalists—and scholars—are challenged over time, specialists may come to repudiate what is today the received view.

However, the received view has immediate and important consequences. The informed public’s impressions of the crisis are based in part on journalists’ and scholars’ hasty pronouncements. These impressions have now hardened into convictions. Political movements of the right and the left are already acting upon dogmas about the crisis that have little or no basis in fact, and policy changes have been made on the basis of these dogmas. Moreover, mass attitudes that have been formed in the crucible of an economic catastrophe cannot be expected to change even if, in the future, careful scholars overturn the assumptions that were the basis for these attitudes. Therefore, we think it is crucial to test the various hypotheses against the available evidence immediately, although we are sure that some or all of our evidence is bound to be superseded, as Weber forecast, and that some of our analysis may be flawed. The basic evidence presented in this chapter is already a matter of public record, however, and the analysis of it is relatively straightforward. Once one confronts the conventional wisdom with this evidence, most elements of the received view crumble, and we are left with the questions that initially made the crisis interesting as well as significant.

The conventional wisdom about the causes of the crisis contains kernels of truth, but most of the rest is demonstrably incorrect. In this chapter, we clear away the underbrush of myth so that we can reclaim the topic for scholarly inquiry. In the process, we will explore some of the tacit assumptions that have commonly led very intelligent and knowledgeable scholars, especially economists, to endorse theories about the crisis that have no apparent basis in reality.

The Limited Role of Low Interest Rates

There is empirical evidence for a modified version of the first thesis—that low interest rates fueled the housing bubble, as opposed to the financial crisis. Stanford’s John B. Taylor (2010) has demonstrated rigorously that not only in the United States, but across the European Union, low interest rates correlated with housing booms during the first half of the decade.

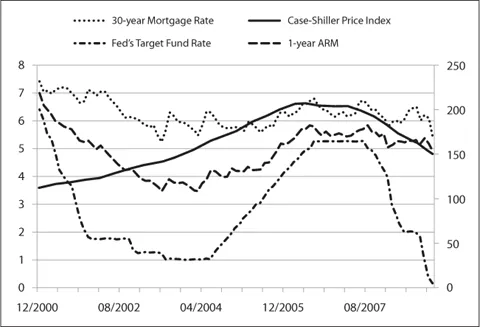

The Federal Reserve Bank (the Fed) and the European Central Bank lowered interest rates from 2001 to 2004, with the Federal Funds Rate falling from 6.5 percent in January 2001 to 1 percent in June 2003, the lowest level in more than four decades (Figure 1.1). It remained at 1 percent for a year before beginning a slow, steady increase to 5.25 percent in 2006. We take no position on whether the central bankers’ actions in lowering interest rates merely reflected a “global savings glut” (e.g., Bernanke 2010; Greenspan 2010) or whether instead it reflected monetary expansion designed to forestall deflation (e.g., Taylor 2010).

What is important for our purpose is that, whatever the ultimate cause of the low Federal Funds Rate, mortgage rates followed the rate Fed Funds Rate downward—although, as seen in Figure 1.1, the rates on fixed 30-year prime mortgages stopped going down when they hit the record low of 5.25 percent in 2003. To have gone lower would have caught banks in a trap when the ultralow interest rates at which they were borrowing money (indicated by the Federal Funds Rate) inevitably began to rise. The Federal Funds Rate could not stay at 1 percent forever, and in anticipation of its imminent rise, banks began issuing adjustable-rate mortgages (ARMs) in huge numbers in 2004. The initial ARM rate is shown by the dashed line in Figure 1.1. After the initial period (usually two years), ARMs would reset in accordance with prevailing interest rates. This is generally accepted as a major cause of the trouble experienced by subprime borrowers, strictly defined as those with low credit scores (e.g., Barth 2010).

Figure 1.1. Fed funds rate, mortgage interest rates, and house prices. Fed Target Fund Rate: Federal Reserve Statistical Release, Selected Interest Rates; 30-Year Mortgage Rate and 1-Year ARM: Federal Reserve Monetary Policy Report to the Congress, February 24, 2009; Case-Shiller Price Index: S & P/Case-Shiller Home Price Indices.

By 2006, more than 90 percent of all subprime mortgages were ARMs, as were 80 percent of all Alt-A mortgages, meaning mortgages to borrowers who were shy of the income, credit-score, or income-documentation standards required for a prime loan (Zandi 2008 Table 2.1). Beginning in 2006, as the Federal Funds Rate rose, subprime borrowers’ inability to pay the higher reset rates triggered the deflation of the housing bubble and a widening concern about the actual value of mortgage-backed bonds. By the third quarter of 2007, “43 percent of foreclosures were on subprime ARMs, 19 percent on prime ARMs, 18 percent on prime fixed-rate mortgages, 12 percent on subprime fixed-rate mortgages, and 9 percent on loans with insurance protection from the Federal Housing Administration” (IMF 2008a, 5n7).

All of this is part of the conventional wisdom, and we do not have reason to challenge it here. But it leaves us with two questions: (1) Why did the new money injected into the U.S. economy, as reflected in low interest rates, cause a bubble in housing, rather than, for example, a bubble in the price of cars, food, airplanes, computers, or clothing? And (2) why did this housing bubble cause a financial crisis—which is to say, a banking crisis—when it popped?

In the next section and in Chapter 2, we will first offer an answer to question 1, which the conventional wisdom has largely ignored. Then, for the remainder of this chapter, we will examine the usual answers to question 2, on which the conventional wisdom has justifiably focused.

The Limited Role of Fannie Mae and Freddie Mac

In principle, low interest rates might have caused an upturn in lending across the board, and thus in overall economic activity, instead of an asset bubble in housing. However, as Simon Johnson and James Kwak (2010, 147) note, during the 2000s, “business investment in equipment and software grew more slowly than in the 1990s, despite the lower interest rates. The problem was that the cheap money was misallocated to the housing sector, resulting in anemic growth.” Why did this happen?

Part of the reason, we believe, was stimulation of the housing market by two government-sponsored enterprises (GSEs): Fannie Mae (the Federal National Mortgage Association) and Freddie Mac (the Federal Home Loan Mortgage Corporation). Even though Fannie Mae and Freddie Mac are private corporations, they were sponsored by the federal government,1 and this made a substantial difference: they were not taxed by the states, and they were able to borrow money more cheaply than ordinary private corporations. Investors assumed that the GSEs, having been created by the U.S. government, would be bailed out if they got into trouble. Therefore, investors were willing to lend money to the GSEs (by buying their bonds, including their mortgage-backed bonds) on much easier terms than the money they lent to ordinary corporations. “Agency” MBS (issued by the two housing “agencies,” Fannie and Freddie), therefore typically paid a 0.45 percent lower interest rate than did privately issued mortgage-backed bonds. The low interest rates that investors required in exchange for lending money to Fannie and Freddie (by buying their MBS) reflected investors’ confidence that the GSEs would be bailed out by the federal government if they became insolvent.

Fannie and Freddie’s role is central in conservative narratives of the crisis (e.g., Wallison 2011a). But the GSEs’ implicit government guarantee became explicit when they were, in fact, bailed out by the federal government on September 7, 2008—a week before the peak phase of the banking panic, which began with the bankruptcy of Lehman Brothers on September 15. We initially assumed that the pre-panic bailout of Fannie and Freddie falsified the conservative view that their reckless mortgage lending caused the financial crisis, for like many observers (e.g., Taylor 2011), we equated the crisis with the nerve-wracking weeks following September 15, when interbank lending around the world froze.

During this period, each bank was afraid that sister banks to which it lent money might own so many “toxic” MBS that they would soon be insolvent and thus unable to pay back any loans. We assumed that this interbank lending crisis, in turn, caused a contraction of bank lending into the “real” economy of businesses and consumers (as opposed to other banks). A contraction in bank lending to businesses and consumers would account for the Great Recession, and this, we assumed, started to occur in September 2008, as each commercial bank, unable to obtain loans from other banks—and perhaps fearful for its own solvency—hoarded cash rather than lending it out.

Since Fannie and Freddie were bailed out a week before the interbank panic, it seemed impossible that fears about whether the federal government would honor its implicit guarantee of their debt could have contributed to the panic, and thus to the recession. However, research by Victoria Ivashina and David Scharfstein (2010) changed our minds about the timing of the contraction in bank lending. This research is also essential to our analysis of the recession in Chapter 3.

How the Great Recession Began

Ivashina and Scharfstein showed that bank lending to businesses began to decline sharply in the third quarter of 2007, long before the panic in the autumn of 2008—and long before the bailout of Fannie and Freddie. This chronology is consistent with what was happening in the mortgage markets in 2007 and even earlier. Once house prices stopped rising in mid-2006, subprime ARM mortgage default rates began to rise (Jarsulic 2010, 40). A year later, on July 11, 2007, ratings downgrades were issued for 1,043 subprime nonagency, or “private-label” mortgage-backed securities (PLMBS).

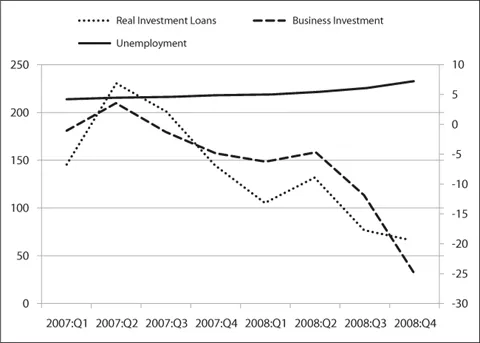

Figure 1.2. U.S. business lending, investment, and unemployment. Left scale: billions of dollars per quarter. Right scale: U.S. unemployment rate/annual change in business investment. Business lending, Ivashina and Scharfstein 2010, Fig. 2; business investment, Federal Reserve, Flow of Funds Accounts, Z.1 Statistical Release.

Figure 1.2 reproduces some of Ivashina and Scharfstein’s data on business lending,2 with the rates of business investment and unemployment superimposed. These data show that business lending and investment started to decline almost precisely when the ratings downgrades occurred—more than a year before the panic of September 2008. These trends are also consistent with the “official” judgment of the National Bureau of Economic Research, which ...

Table of contents

- Cover

- Title

- Copyright

- Contents

- List of Figures and Tables

- Glossary of Abbreviations and Acronyms

- Introduction

- 1 Bonuses, Irrationality, and Too-Bigness: The Conventional Wisdom About the Financial Crisis and Its Theoretical Implications

- 2 Capital Adequacy Regulations and the Financial Crisis: Bankers' and Regulators' Errors

- 3 The Interaction of Regulations and the Great Recession: Fetishizing Market Prices

- 4 Capitalism and Regulation: Ignorance, Heterogeneity, and Systemic Risk

- Conclusion

- Appendix I. Scholarship About the Corporate-Compensation Hypothesis

- Appendix II. The Basel Rules off the Balance Sheet

- Notes

- References

- Index

- Acknowledgments

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Engineering the Financial Crisis by Jeffrey Friedman,Wladimir Kraus in PDF and/or ePUB format, as well as other popular books in Business & Government & Business. We have over 1.5 million books available in our catalogue for you to explore.