![]()

STEP 1

HOW LENDERS SEE YOU

Lenders don’t want to treat you like a number or a piece of paper. But lenders are running a business, and they have constraints. They have to work within certain rules, using a series of formulas, before lending you money. It doesn’t matter if you’re nice, if you’ve lost your job, or if a bad relationship has left you in a financial hole. Lenders have to depend on a series of written reports, and a number, to learn everything they need to know about you. What is most influential in making their decision is your credit history.

YOUR CREDIT REPORT

The written report that lenders depend on is called your credit report. A credit report is essentially a history of your entire financial life, from your first credit card to the present time.

There are three major companies that track your credit. They’re called credit bureaus. These companies—Equifax, TransUnion, and Experian—all keep similar records of your credit history. When a lender is considering giving you a loan or a credit card, the lender will contact one of the three credit bureaus for a copy of your credit history. On the basis of the information in your file, the lender will decide whether or not to take a risk with you, how much to lend you, and at what interest rate.

WHAT’S IN YOUR REPORT

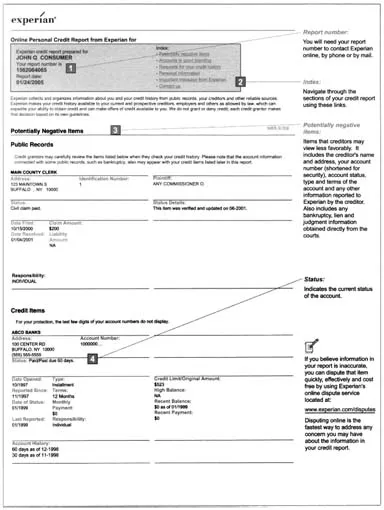

Each credit bureau uses a different format for the information it collects, but all three bureaus have basically the same information. You’ll first find identifying information, such as your name, your Social Security number or Individual Taxpayer Identification Number (ITIN), and your address. Your employment information will also appear here.

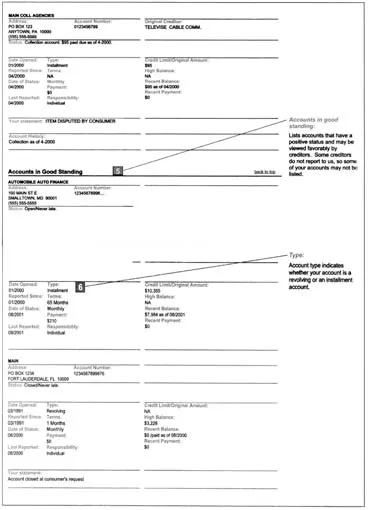

Next, you’ll find a listing of all the credit accounts you’ve ever had. This will show if the account is closed or current; when the account was opened (and closed, if it’s been closed); your credit limit or loan amount; the account balance; and your payment history. This is where lenders will see if you’ve been paying your accounts on time.

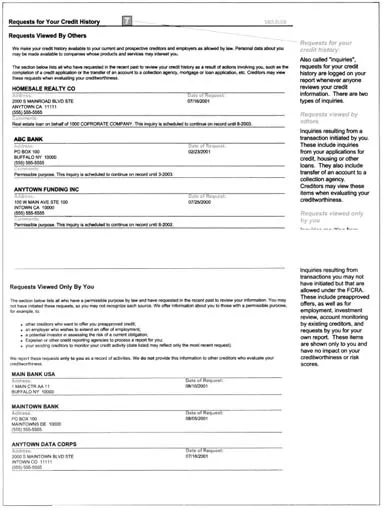

Then comes a section on inquiries. An inquiry takes place when someone asks for a copy of your credit report. Inquiries may come from lenders, from landlords, or from employers. The report lists both voluntary inquiries, which are ones that come when you give lenders permission to check your report when you apply for credit; and involuntary inquiries, which come when lenders order your report on their own—for example, if they want to send you a preapproved credit offer in the mail.

Finally, your credit report will have a section that includes information of public record, usually based on papers filed in a court of law. This can include information on collection agencies seeking funds from you, bankruptcies, foreclosures, overdue alimony or child support payments, lawsuits, liens, wage attachments, and judgments. It may also include arrest records.

GETTING A FREE COPY OF YOUR CREDIT REPORTS

If your credit history shows you’ve made late payments in the past, or if you’ve taken out loans you’ve never repaid, you may have a hard time getting a new lender to lend you any money. And if lenders are willing to lend you money, they’re going to charge a very high interest rate—to the point that you may be paying more in interest than you borrowed in the first place.

That’s why it’s so important to have a good credit history. If you want to buy a car, get a mortgage, get a credit card, or rent an apartment, the people you want to do business with will want to know you’re a good risk. Having a good credit report will save you money and allow you to accomplish many of your financial goals.

It’s very possible that your credit report has some errors. It may show that you’re delinquent on an account, when in reality that account should be clean. This is why it’s essential for you to get a copy of your credit report, read it, understand it, and make sure it’s accurate.

New legislation passed in Congress—the Fair and Accurate Credit Transactions Act (FACT Act)—allows everyone to get free copies of his or her credit reports from the three major credit bureaus once a year. To get your free reports, you must call 877-322-8228, or visit www.AnnualCreditReport.com. This is a centralized service created by the three credit bureaus to help consumers access their reports in one place (while helping the bureaus keep track of which consumers have ordered their reports).

Warning: If you go to the Web site, make sure to spell the Web address very carefully. There are imposter sites that have similar spellings, and if you end up at these sites by mistake, they’re going to tell you about other services, which you need to pay for before you get your reports. It’s a scam to try to get you to pay for services you don’t necessarily need. The AnnualCreditReport.com site is perfectly safe. But the Federal Trade Commission (FTC)—the government agency that deals with consumer protection and other economic issues touching the lives of most Americans—warns that consumers must be careful not to be fooled by these other sites. The FTC recently settled a lawsuit against a company that promised “free” reports, but these weren’t really free. If you’re nervous about making a mistake when you type a Web address, you can go to the FTC Web site at www.ftc.gov. There, you’ll find a link to the authentic AnnualCreditReport.com site. Or simply visit the Esperanza USA site (www.esperanza.us) for a direct link.

You can also contact the three credit bureaus directly for copies of your reports, but the copies are free only if you go through the site mentioned above. The three credit reporting agencies—Equifax, Experian, and TransUnion—offer essentially the same information in their credit reports. Only the layout is slightly different. If you order through AnnualCreditReport.com, you can get all three for free. You want to make sure they’re all accurate, because while no one report is more important than the others, you don’t know which one your lender will see.

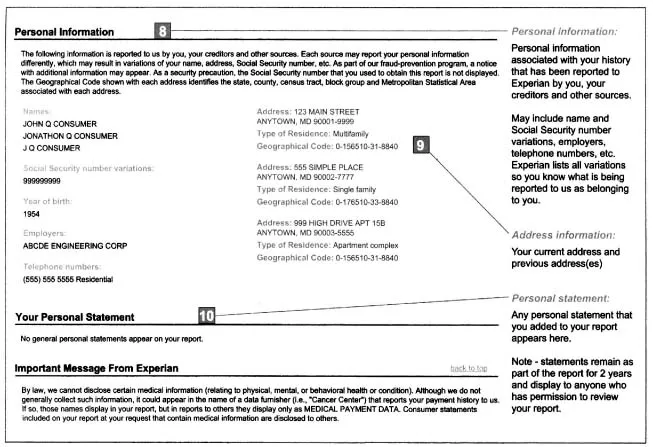

WHAT YOUR CREDIT REPORT LOOKS LIKE

On pages 6-12 you will see an example of what you can find on Experian’s report.

WHAT TO DO WITH YOUR REPORTS

Read, read, read. Carefully go through each entire report and make sure there are no errors. Errors are common. According to a study done in 2004 by the U.S. Public Interest Research Group (U.S. PIRG), as many as 79 percent of credit reports have errors. According to the study, 25 percent of those errors were serious enough that credit could easily have been denied to consumers because of the wrong information. The study is called “Mistakes Do Happen: A Look at Errors in Consumer Credit Reports.”

The Web sites of the three credit bureaus have very explicit directions on how to read their reports, which all look somewhat different. Read the directions to understand how each bureau presents the information. If you see something you don’t understand, call the bureau’s toll-free number. A customer service representative can help you translate the jargon, or explain anything else that doesn’t make sense to you.

IF YOU FIND A MISTAKE

To fix mistakes on your reports, you have to take charge. This process is called “dispute.”

If you want to dispute an item on your report, the first step is to contact the credit bureau by writing a letter, explaining the error you’ve found. The credit bureau will open an investigation, which will probably include contacting the lender who told the bureau that, for example, you missed a few payments. The lender will then review the information and report back to the bureau with its findings. If the credit bureau agrees that the item on your report is an error, the bureau will make the change in your report. By law, the companies have 30 days to investigate and report back to you on their findings.

If you need help writing a dispute letter, the Federal Trade Commission offers a sample letter, available on page 13.

Date

Your Name

Your Address

Your City, State, Zip Code

Complaint Department

Name of Company

Address

City, State, Zip Code

Dear Sir or Madam:

I am writing to dispute the following information in my file. I have circled the items I dispute on the attached copy of the report I received.

This item (identify item(s) disputed by name of source, such as creditors or tax court, and identify type of item, such as credit account, judgment, etc.) is (inaccurate or incomplete) because (describe what is inaccurate or incomplete and why). I am requesting that the item be removed (or request another specific change) to correct the information.

Enclosed are copies of (use this sentence if applicable and describe any enclosed documentation, such as payment records, court documents) supporting my position. Please reinvestigate this (these) matter(s) and (delete or correct) the disputed item(s) as soon as possible.

Sincerely,

Your name

Enclosures: (list what you are enclosing)

You can also visit www.esperanza.us for more sample letters.

If one credit bureau has a mistake in your file, there’s a good chance that the same mistake will appear on your other reports, too. Compare your two other credit reports to make sure they don’t have the same mistake. If they do, notify those bureaus of the errors. Also, be aware that the lender who misreported the information to the first bureau is required to make the correction at all three bureaus. Still, it’s smart to make sure that this happens.

If the investigation into your complaint goes your way, great. The lender is then required to give you the results in writing, and if the investigation leads to a change to your report, the bureau must give you another free report. (This doesn’t count as one of your annual free reports.) If the mistake has been fixed, you can request that the bureau contact all those who received the inaccurate report in the past six months (or the past two years, for employers) to tell them of the correction.

If the investigation doesn’t turn out as you hoped, and the credit bureau and the lender insist that the information is accurate, there’s not much you can do to change it. But what you can do is add a short written statement to your credit file to explain your side of the story. You can do this free. Your written statement will then become part of your credit report, and anyone who wants to see your report will also see your version of events. Here’s a sample letter.

Date

Your Name

Your Address

Your City, State, Zip Code

Name of Credit Bureau

Credit Bureau Address

City, State, Zip Code

Dear Sir or Madam:

I disagree with (identify the item you are disputing here). I took the following action: (explain the action you took to pay the item here, and include dates if you have them). I have disputed the item but the company says (explain what the company’s side is here). I have included here copies of (list here any proof you have of your actions).

Sincerely,

Your name

It’s important to understand that you can’t dispute negative informatio...