- 440 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

Market Practice in Financial Modelling

About this book

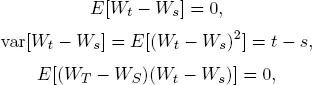

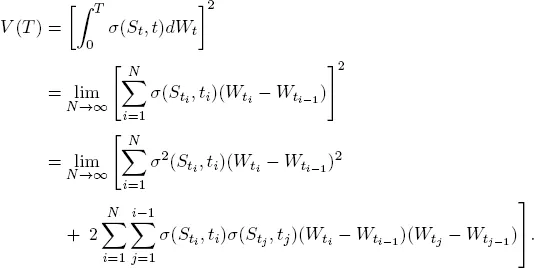

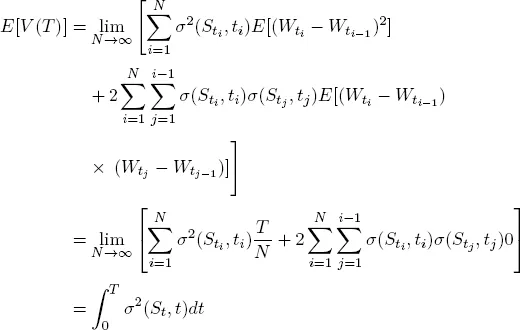

Written to bridge the gap between foundational quantitative finance and market practice, this book goes beyond the basics covered in most textbooks by presenting content concerning actual industry norms, thus resulting in a clearer picture of the field for the readers. These include, for instance, the practitioner's perspective of how local versus stochastic volatility affects forward smile, or the implications of mean reversion on forward volatility.

Key considerations for modelling in rates, equities and foreign exchange are presented from the perspective of common themes across various assets, as well as their individual characteristics.

The discussion on models emphasizes the key aspects that are relevant to the pricing of different types of financial derivatives, so that the reader can observe how an appropriate choice of models is essential in reflecting the risk profile and hedging considerations for different products.

With the knowledge gleaned from this book, readers will attain a more comprehensive understanding of market practice in derivatives modelling.

Foreword

Foreword (246 KB)

Contents:

- Introduction

- Standard Market Instruments

- Replication

- Correlation Between Two Underlyings

- Local Volatility

- Stochastic Volatility

- Local Stochastic Volatility

- Short Rate Models

- The Libor Market Model

- Long-Dated Foreign Exchange

- Forward Volatility and Callability

- Funding and Basis

Readership: Students of financial mathematics (final year undergraduates and postgraduates) as well as new entrants into the derivatives area of investment banking.

Tools to learn more effectively

Saving Books

Keyword Search

Annotating Text

Listen to it instead

Information

Table of contents

- Cover

- Halftitle

- Title

- Publisher

- Dedicated

- Concept

- Preface

- Foreword

- Contents

- Acknowledgements

- 1. Introduction

- 2. Standard Market Instruments

- 3. Replication

- 4. Correlation Between Two Underlyings

- 5. Local Volatility

- 6. Stochastic Volatility

- 7. Local Stochastic Volatility

- 8. Short Rate Models

- 9. The Libor Market Model

- 10. Long-Dated Foreign Exchange

- 11. Forward Volatility and Callability

- 12. Funding and Basis

- Final Thoughts

- Glossary

- Bibliography

- Answers to Selected Questions

- Index

Frequently asked questions

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app