Crucial methods, tactics and tools for successful pension fund management

Achieving Investment Excellence offers trustees and asset managers a comprehensive handbook for improving the quality of their investments. With a stated goal of substantially and sustainably improving annual returns, this book clarifies and demystifies important concepts surrounding trustee duties and responsibilities, investment strategies, analysis, evaluation and much more.

Low interest rates are making the high cost of future pension payouts fraught with tension, even as the time and knowledge required to manage these funds appropriately increases — it is no wonder that pensions are increasingly seen as a financial liability. Now more than ever, it is critical that trustees understand exactly what contributes to investment success — and what detracts from it. This book details the roles, the tools and the strategies that make pension funds pay off.

Understand the role of pension funds and the fiduciary duty of trustees

Learn the tools and kills you need to build profound and lasting investment excellence

Analyse, diagnose and improve investment quality of funds using concrete tools and instruments

Study illustrative examples that demonstrate critical implementation and execution advice

Packed with expert insight, crucial tools and real-life examples, this book is an important resource for those tasked with governing these. Achieving Investment Excellence provides the expert insight, clear guidance and key wisdom you need to manage these funds successfully.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

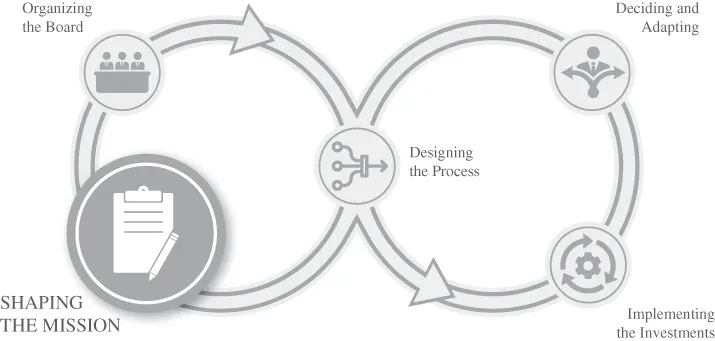

PART One Pension Funds: Understanding the Role, Shaping the Mission

The basic question considered in Part I is the role and purpose of a pension fund, both in a generic and in a specific sense. This will be useful later in the book, as investing is the means for realizing the pension fund's purpose. We will also home in on the role of the board and its members. This is important, because throughout the book we will return time and time again to the critical role of the board in creating investment excellence. Fiduciary duty is important here, but there is also more; steering the fund strategically through a changing societal context, for example. Then we will move on to specific questions: How can you formulate a mission, a vision, and a strategy? How do you move towards your vision?

In this first part of the book we find ourselves firmly in the slow-moving, strategic part of the organizational loop. This is the part where the board sets the scene. Because in daily life, boards tend to spend a lot of time on the immediate issues at hand, it is not always easy to see this strategic layer.

Part I Topics Include:

The role of a pension fund, and the roles of a board and its trustees;

The meaning of fiduciary duty;

How to formulate the mission, vision, and strategy of a pension fund;

The importance of explicitly stating the strategic foundation of a fund in order to avoid confusion later on in the process.

After reading Part I, you should be able to state with confidence: This is the reason for the existence of my fund and this is what it does to realize its objective, given the current context. If this is not totally clear to—and shared by— everybody involved, there is still work to be done!

CONTRIBUTION OF THIS PART TO INVESTMENT EXCELLENCE

Part I gives insight into the role and responsibilities of the board and establishes the idea that the board can make or break investment excellence. By shifting the attention from ad hoc and sometimes reactive decision-making to formulating the mission and the strategy for the fund, it helps the board to look further ahead. This makes it possible to move systematically and in a controlled way towards the achieving the mission, while at the same time taking into account the changing environment in which the fund operates. Operating in the way, decision-making will be more proactive and the fund will be much more in control of its future path.

CHAPTER 1 The Role of Pension Funds, and the Role of Boards

Key Take Aways

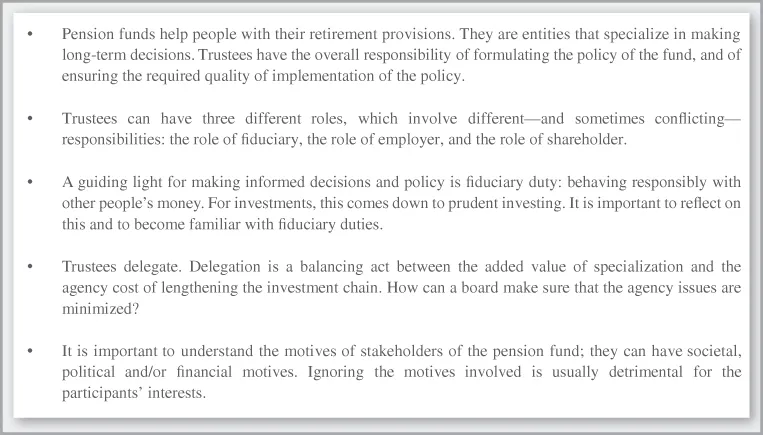

In this chapter, we focus on the pension fund and its board of trustees. The primary role of the board is defining the goals of the pension fund, setting policy, organizing the investment process, and monitoring and adjusting choices in order to adapt to any changing circumstances. Boards can be a complex and diverse combination of lay people in the field of finance, as well as people with a professional background in finance or investing. The board is the key determinant of the success of a pension fund.

In a recent review of how boards have developed over time, Ambachtsheer1 states that “while there is some evidence of improvement of pension organizations […], the finding is that the major concerns about how board members are selected and trained, about the effectiveness of board oversight processes, and about the ability to attract and retain key executive and professional skills remain. Much remains to be done to materially raise the effectiveness of the governance function in pension organizations.”

A malfunctioning board can have a considerable negative impact on the pension fund. The malfunction can have many causes, from failing to understand the crucial role of the board to appointees lacking the skills needed to be effective board members. This chapter outlines the very first step a board should undertake in order to be well functioning: understanding its roles and responsibilities, thus forming the framework for all other steps and decisions required in the investment process and governance. Understanding these roles, however, requires background knowledge on what it actually is that a pension fund does. To this end, we start with a short overview of pension funds, why they exist, and what their roles are. Our view is that these roles and responsibilities—give or take a few cultural and regulatory differences—have clear commonalities around the world. Following this, we discuss the characteristics of a pension plan, which defines who pays what (premiums), who receives what (pensions), and, crucially, who holds which risk.

Zooming in on the role of the board, we consider a trustee's responsibilities from three angles: the duties as a fiduciary, the duties as a board member and the duties as a shareholder of an investment organization. An important question is how to balance these roles. Because delegation is an important board task, we discuss delegation and agency issues that arise as a result of delegation. The chapter concludes with a section on understanding and managing different stakeholders.

THE ROLE OF PENSION FUNDS

As the baby boom generation started to retire in the first decade of the twenty-first century, the amount of capital needed to provide for future income increased. In 2017,2 global wealth was $280 trillion. This is about four times the global gross domestic product (GDP), which totaled $75 trillion in 2015. Pension funds in the 22 most important pension countries managed $36.4 trillion at the end of 2016, amounting on average to 62% of their local GDP.3 Thus, pension funds are significant players in the world's economy. A pension fund is an institution set up to accumulate assets in order to pay retirement obligations. It thus provides the means for individuals to accumulate savings over their working life so as to finance their consumption needs in retirement, either by means of a lump sum or by provision of an annuity. To a large extent—often 75% or more—the benefits are paid out of investment returns. This means that pension funds are important investors and sources of potential long-term capital to parties such as corporations, governments and sometimes households.4

In many countries the pension system consists of three pillars: a state pension, the supplementary company pensions, and the private individual pension products that each person can arrange for themselves.

First pillar pensions are a basic pension provided to all citizens by the local government of many countries around the world. This requires (tax) payments throughout the citizen's working life in order to qualify for the benefits upon retirement. A basic state pension is a “contribution-based” benefit, and depends on an individual's contribution history. Examples are National Insurance in the UK, or Social Security in the US.

The second pillar consists of the company pension schemes, as well as pension schemes for occupations and industries. This book focuses on these second pillar pensions, but its insights and lessons are easily applicable for the other types of pension schemes as well. The basis for setting up a second pillar pension fund is the pension plan, i.e. a plan that determines the funding, accrual and payout of benefits; detailing the rights and obligations of members and sponsors.5 Pension funds then administer the pension plan.

The third pillar is formed by individual pension products, such as an annuity insurance or via a tax-efficient blocked savings account. These are mainly used by the self-employed and employees in sectors without a collective pension scheme. However, these products can be serviced or offered by pension organization, where the boards have similar fiduciary duties to second pillar pension plans.

Each pension plan has certain key elements. These include6:

A pension agreement that describes the pension benefit structure and guides day-to-day operations;

A trust fund, foundation or other form of organization, independent from the sponsor, to hold the plan's assets and the administration of pension benefits. The trust is legally and financially independent from the companies;

A record-keeping system to track the flow of money going to and from the retirement plan;

Documents to provide plan information both to the employees participating in the plan, and to the government;

At times, a number of officials with discretion over the plan; these are the plan's fiduciaries.

For a trustee, the main concern is to ensure that the members' retirement obligations will be properly funded and protected. The trustee's role is to make sure that pensions are paid not only now, but also in the future. These obligations stretch out over a long period. Understanding the longevity of the obligations provides a starting point for trustees in getting to know the fund. Taking a brief look back in time, in 1889, German Chancellor Otto von Bismarck introduced the first pension for workers aged over 70, at a time when the average life expectancy of a Prussian civil servant was 45. In 1908, when the British Prime Minister Lloyd George secured a payment of 5 shillings a week for underprivileged workers who had reached 70, Britons, and especially those who were poor, were lucky to survive much beyond 50. By 1935, when the United States set up its Social Security ...

Table of contents

Cover

Table of Contents

About the Authors

Acknowledgments

Foreword

Introduction

PART One: Pension Funds: Understanding the Role, Shaping the Mission

PART Two: Designing the Process

PART Three: Implementing the Investments

PART Four: Organizing the Board

PART Five: Learning, Adapting and Improving

Self-Reflection Questions

Appendix A

Appendix B

References

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Achieving Investment Excellence by Kees Koedijk,Alfred Slager,Jaap van Dam in PDF and/or ePUB format, as well as other popular books in Volkswirtschaftslehre & Banken & Bankwesen. We have over 1.5 million books available in our catalogue for you to explore.