You are paying much more in tax than you think you are

What Everyone Needs to Know About Tax takes an entertaining and informative look at the UK tax system in all its glory to show you just how much you pay, how the money is collected and how it affects ordinary people every day. Giving context to recent controversies including the Panama Papers, tax avoidance by multinationals, Brexit and more, this book provides a straightforward explanation of tax and the policy behind it for non-specialists — no accounting or legal knowledge is required. The system's underlying logic is illustrated through three 'golden rules' that explain many of the UK tax regime's oddities, and the discussion focuses on the way things are rather than utopian ideas about how they might be. Case studies show how the VAT on a plumber's bill all adds up; why fraudsters made a movie to throw HMRC off their scent; how a wealthy couple can pay so little tax on a six-figure income; and the way tracing the money you paid for your iPad sheds light why the EU is demanding Apple pay billions extra in tax.

Ever the political battlefield, tax is too important for you to rely on media hype for information. It affects everyone, every day, and it pays for voters and taxpayers to know more. This book leaves aside technical detail and the arcana of the tax code to give you a real-world look at how tax works.

Learn about the many ways that the tax system separates us from our money

Discover how Brexit could change the way we pay taxes

Understand how changing tax policy affects people's everyday lives

See through the rhetoric surrounding controversies in the media

With tax, we have to admit that there are no easy answers. No one enjoys paying them, but without them, the Government would shut down. Seeing through politicians' cant and superficial press coverage is critical for your ability to make the decisions that benefit you; What Everyone Needs to Know About Tax gives you the background and foundational knowledge you need to be a well-informed taxpayer.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Income tax: when you think about tax, that's probably the tax you're thinking about. It was introduced by the Prime Minister, William Pitt the Younger, as a temporary measure in 1798 to fund the Napoleonic Wars. Legally, it's still temporary. Every year, Parliament has to vote for income tax to apply for another twelve months. If ever MPs failed to do so, the government would run out of money and have to shut down.

We all know that the basic rate of income tax is 20p in the pound and the higher rate is 40p. These headline figures are the UK's ‘marginal rates of tax’. When tax experts talk about the marginal rate of tax, they mean the rate you pay on each extra pound of income that you earn. Just looking at income tax, the first £11,000 you earn is tax free so the marginal rate up to this amount is nil. Then it increases to 20%, the basic rate. When you earn over £43,000 the marginal income tax rate goes up to the higher rate of 40%. So, if you are paid £20,000 a year, your marginal income tax rate is 20% because if your pay increases to £20,001, you have to pay 20p of income tax on the extra pound you earn.

A 20p marginal rate of income tax doesn't sound so bad compared to all the public services we enjoy, like healthcare and education. But you have to factor in employers' and employees' national insurance as well. These add 26p of tax on each extra pound a basic rate taxpayer earns.

On top of that, any welfare benefits received from the government are reduced as we earn more. Handing back your benefit payments acts like yet another form of taxation on each extra pound you earn. For the lower paid, the way that benefits are phased out as people start working means they can face marginal tax rates of up to 90%. We'll talk some more about that later in the chapter. For the middle classes, child benefit is clawed back if anyone in the family earns over £50,000. Having to pay back child benefit has the same effect on take-home pay as an increase in tax. This means income tax and national insurance, together with benefit payments, can combine to produce very high marginal tax rates.

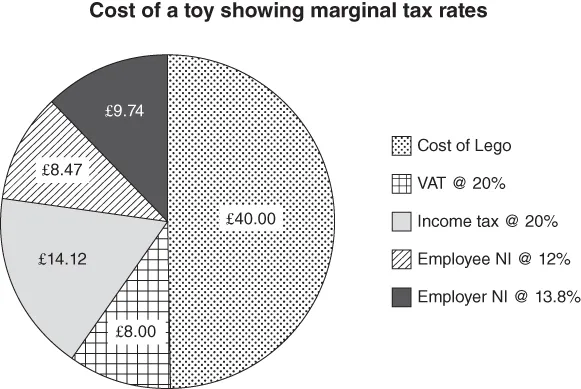

In the Introduction, I showed how you probably need to earn £60 to buy a Lego truck worth £40, once you include income tax, national insurance and VAT. That's £20 in taxes. However, this amount factors in your personal allowance of £11,000 on which you don't have to pay income tax. Now imagine you needed to work some overtime before you could afford to buy the toy. You've already used up your personal allowance so you now have to look at your marginal tax rate to work out how long you need to work. As a basic rate income taxpayer, you would need to earn £70.60 in overtime to buy that £40 truck. Thanks to high marginal rates of tax, over £30 of the £70.60 that your employer pays you to work the overtime goes to the government. That's an overall tax rate of 43%. Add employers' national insurance and it’s 50% (see Figure 1.1). If you are a higher rate income taxpayer, your combined tax rate for ordinary purchases is 58%.

Figure 1.1 The taxes on a £40 Lego set for a basic rate taxpayer showing taxes coming to as much as the toy.

The way multiple taxes add up to big bucks is my First Golden Rule of tax: lots of small taxes together combine to make large tax bills. Rather than hit us with a single massive demand that we can't help feeling bad about, the system is organised into lots of smaller levies that accumulate. There are lots of different taxes with lots of different names charged on lots of different things. But, in the end, you and I end up paying them all.

Whether a tax is levied on the companies we work for, or the shops we buy from, it all comes out of our pockets. That's my Second Golden Rule of tax: no matter what name is on the bill, all tax is ultimately suffered by human beings. There is no magic pot of money for governments to dip into. Even when the government borrows, it must tax us in the future to pay back the debt. To understand your personal tax burden, you have to add up all taxes, even the ones that you don't pay directly and may not even know about.

National insurance contributions

We've seen that, as well as income tax, we also pay national insurance contributions on our salaries. It's time to have a closer look at this most misunderstood of taxes.

When you pay national insurance contributions (usually abbreviated to ‘NICs’), what exactly are you contributing to? Many people are vaguely aware of a link between national insurance and their state pension. Indeed, you need to have been paying NICs for 30 years to qualify for the full state pension (if you miss a few years out, you can catch up on them later).

Let's see what that means. Assume you are on average earnings of £26,500 throughout your 35-year working life. That means the combined employees' and employers' national insurance contributions paid on your salary will be about £4,750 a year. Now, suppose you invested that £4,750 a year in a private pension instead of paying it over to the government. With a growth rate of 5% above inflation (the long-run rate of return for shares), your notional pension pot from payments equivalent to your national insurance contributions should be worth over £430,000 when you retire. That would get you an index-linked pension at today's historically low annuity rates of £14,750 a year. A few years ago it would have got you considerably more and, once interest rates return to normal levels with the economic recovery, we can expect pension annuity rates to rise as well. Alternatively, under the new pension freedom rules, you could take that £430,000 as income or reinvest it.

The £14,750 a year pension you would have from saving £4,750 a year in a private pension scheme is a much better deal than the state pension of £8,094 that you really get for making those 35 years of contributions. Worse, if you work for longer (as most of us do) or pay higher NICs because you have higher earnings, you don't get a better state pension. The government does pay our national insurance contributions into a special fund separate from general taxation. But it is not investing the money to pay for your pension when you retire. The national insurance fund only has enough money in it to pay for about two months of benefits for today's claimants. In essence, it is a current account, not a savings account. The government collects money from people currently in work to pay pensions to today's retirees. There is no money set aside to fund pensions in the future. We are entirely reliant on our children being willing to cough up in the same way we have. So, looked at as a contributory pension scheme, national insurance is a very bad deal. However, we should instead regard NICs as another income tax with a different name. It accounts for a fifth of the government's revenues. Although it funds pensions and some other benefits, a large amount of it is used to pay for the NHS. Now, of course, the NHS needs funding and our taxes are the way to do it. But given national insurance contributions have no real contributory element and are really a tax on earnings, why don't we call them a tax?

The answer is one of low politics rather than high principle. At the most basic level, it's a manifestation of the First Golden Rule of tax: lots of small taxes together combine to make large tax bills. It suits the government that we pay multiple taxes with low rates rather than a single transparent and easily understood levy. The complexity of the tax system means no one ever realises how much he or she is paying. This makes it a whole lot easier to extract more tax from us without causing a revolution. Combining income tax with employees’ and employers’ national insurance into a single levy would give us a basic rate of income tax of about 45p in the pound. No government wants to admit that tax rates are that high. So they prefer the sleight of hand of having a 20p income tax rate, 12% employees' national insurance contributions and the essentially invisible 13.8% employers' national insurance contributions.

What, you might ask, is the difference between employers' and employees' national insurance? In all honesty: nothing. They are both taxes on your salary, they are both collected in the same way (through PAYE, which we will discuss further below) and your employer sees them both as amounts they have to pay to keep you turning up to work. The main distinction is that earnings are capped at £43,000 when calculating most of an employee's NICs (and the version paid by the self-employed). This recognises that, by earning more, you don't get better benefits or a bigger pension from the system. In fact, it was not until the 1970s that national insurance stopped being charged at a flat rate so that everyone paid the same. Thanks to Gordon Brown, you now also pay 2% NICs on your earnings over the £43,000 threshold.

Employers' NICs are 13.8% of our entire salary above £8,112 without any upper limit. That means employers' national insurance embodies the Golden Rules of tax: following the First Rule, it is kept separate from income tax, even though it is a tax on income. This disguises just how much we actually pay. It is also in accordance with the Second Golden Rule: no matter what name is on the bill, all tax is ultimately suffered by human beings. Because this element of national insurance is paid by our employers, we don't realise that we are suffering it. But, despite all the subterfuge, ordinary people still end up shelling out.

If you are in work, it's a good rule of thumb to treat NICs and income tax as the same thing, although there are, inevitably, various wrinkles and complications in the rules. For example, savers and pensioners pay income tax but not national insurance. When you factor in employers' NICs, this means there is twice as much tax on wages from work than on money you get from savings or your pension. This might make sense economically, since we do want to encourage saving. And maybe it is fair that pensioners, after being taxed all their lives, don't have to keep paying national insurance after they've retired. But that doesn't explain why wealthy pensioners are taxed a great deal less than low-paid workers.

In most respects, however, NICs and income tax are drawing ever closer together. For example, until 1991, there was no national insurance on many perks such as company cars. Even in the 1990s, it was still possible to exploit gaps between the rules on income tax and NICs. Some city firms were paying bonuses in gold or diamonds to avoid national insurance (which was payable on cash wages only).

More recently, both Labour and Conservative governments have been ironing out the smaller wrinkles to make national insurance and income tax as similar as possible. Nowadays, many benefits in kind, including company cars, are subject to both income tax and employers' national insurance. They go on a special form called a P11D and you pay tax on the monetary value of a benefit as if it were cash. As it happens, one of the most tax-efficient perks available today is not turning up to work. If you take extra holiday as a benefit (and many firms allow their employees a few extra days a year in exchange for sacrificing some of their salary), the cost to you is only the pay you would have received after tax.

Although income tax and NICs are now administratively almost identical, no politician is going to amalgamate them into a single transparent rate of tax. After all, under the First Golden Rule, there is no sense in emphasising how high the combined rates of tax that we pay really are. Tory MP Ben Gummer did suggest in 2014 that NICs should be renamed ‘earnings tax’. That would, at least, be a candid name.

Paying tax

Most people with jobs don't have to worry about paying their taxes as it is all done for them automatically. Payslips show the tax paid, but many of us never really look at any figure except the bottom line, which is our take-home pay. We pay most of our taxes through PAYE, which was invented at the end of the Second World War as a way to improve the efficiency of tax collection. From the point of view of the government, it has three major advantages. The first is the official one. The administration of the tax system for employees was handed to the people they work for. It was no longer necessary for individual workers to figure out how much tax to pay. Instead, our employers calculate the tax we owe and deduct it from our salary. We only ever receive our net wages. The tax component is paid straight over to HMRC. In effect, this privatised a large chunk of tax collection. The primary responsibility for gathering tax was transferred from the tax authority to employers. They bear the cost and suffer the penalty if things go wrong. It is much easier for HMRC to audit employers' tax collection systems than it is to check the tax returns of all the individual employees.

The second advantage of PAYE for the government is that it accelerates when the money arrives in the Treasury's coffers. With PAYE, the government gets paid monthly, just like we do. I receive my net salary and the Exchequer receives both the income tax and national insurance. Given that, between them, NICs and income tax collected through PAYE account for over half the government's total tax-take, the cash flow benefits of regular payment are extremely significant.

The third advantage of PAYE is the subtlest, but perhaps the most important: we never see the tax we are paying. Out of sight, it is kept out of mind. Employers' NICs are also concealed in plain sight. Most of us never think about them or realise that they are a tax on our salary just as much as income tax. Even though employees' national insurance and income tax are supposedly taxes that we pay ourselves, the system requires businesses to pay these taxes on our behalf using the same PAYE machinery with which they account for employers' national insurance. So we never possess our money before the government gets its paws on it.

Ensuring that we hardly ever have to pay any tax directly is a major pillar of the UK's revenue system. In fact, it is a principle that deserves to be enshrined in the Third Golden Rule of tax: taxes are kept as invisible as possible. The government wants to avoid people paying their taxes directly so they are less likely to notice them. I can explain why this is so important from personal experience.

As I noted in the Introduction, I've worked as an accountant for many years. But I'm also occasionally paid for my journalism. This means I have to fill out a tax return each January. Completing the return is a pain, but nothing like as painful as what happens next. Once I've calculated my tax bill for the year, I have to write a cheque for what I owe. This is not usually very large, a few hundred pounds in most years, occasionally a couple of thousand. But I resent writing that cheque far more than I do paying the tax on my regular salary, even though the latter is a much greater amount. I also have to make sure I've saved up enough to cover the bill. Seeing the money leave my bank account and sail off into the grateful arms of the Chancellor of the Exchequer seems far more onerous than the cumulatively much bigger deductions my employer makes from my monthly wages.

Under PAYE, most people don’t have to fill out a tax return, let alone write a cheque to HMRC. We never receive the tax we pay on our salaries. This means we never feel its loss. I...

Table of contents

Cover

Title Page

Copyright

Table of Contents

Dedication

About the author

Introduction

Chapter 1: Taxes on your income and earnings

Chapter 2: Taxes on what you spend

Chapter 3: Taxes on what you own

Chapter 4: Taxes on business

Chapter 5: Taxes evaded, avoided and reformed

Conclusion: the Three Golden Rules of tax

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access What Everyone Needs to Know about Tax by James Hannam in PDF and/or ePUB format, as well as other popular books in Business & Taxation. We have over 1.5 million books available in our catalogue for you to explore.