Strategic technology strategy for smaller financial institutions

Breaking Digital Gridlock empowers credit unions and community banks to make the shift to digital—even without a seven-figure consulting budget. From leadership, to technology, to security, and more, this book provides effective, real-world strategies for taking the leap without tearing your organization apart. With an emphasis on maintaining the culture, services, and features you have carefully crafted for your customers over the years, these strategies allow you to make your organization more resistant to digital disruption by adopting key technologies at key points in their evolution. Expert advice grounded in practicality shows how FinTech partnerships and strategic technology acquisition can foster new growth with minimal disruption, and how project management can be restructured to most effectively implement any digital solution and how to implement and leverage analytics. Specific implementation advice coupled with expert approaches offer the ability to modernize in an efficient, organized, financially-sound manner.

The companion website features a digital readiness assessment that helps clarify the breadth and scope of the change, and serves as a progress check every step of the way. Access to digital assets helps smooth the path to implementation, and a reader forum facilitates the exchange of ideas, experiences, and advice.

Identify revolutionary versus evolutionary technology opportunities

Empower employee innovation, and stop managing all risk out of good ideas

Understand blockchain, machine learning, cloud computing, and other technologies

Forge strategic partnerships that will drive growth and success amidst technological upheaval

It is widely accepted that digital is the future of banking, but knowing is not the same as doing. If your organization has been riding the fence for too long amidst uncertainty and budget constraints, Breaking Digital Gridlock provides the solutions, strategies, and knowledge you need to begin moving forward.

Continual internal process improvement is often the greatest threat to any organization. It's never more apparent than when an organization commits to changing a computer system. When a new system is chosen, it will result in the need for process improvement. You may wonder why there would be a chapter on processes in a digital transformation book, and the reason is simple. Eventually, every process in your organization will be digitized, and as a result, your digital processes will reflect your analog processes. For instance, if there are 71 steps in your current loan application process, there will likely be 71 steps in your digitized process. However, a digitized process should reduce steps, improve speed, and improve efficacy. For example, solid processes can—and should—transform a 71-step loan application process into a 3- or 4-step process. Unfortunately, our human instinct to avoid change kicks in. Our instincts are to avoid the unknown and resist things that force us to change, and as a result, getting the process down to a few digital steps will prove to be an uphill battle for even the most seasoned executives.

Regulatory Gridlock

The fear of the unknown is normal for everyone. We know that the existing 71-step process works, so why would we change it? There may even be obvious improvements in the process, and the staff may even acknowledge these initially. Eventually, though, they begin to worry that that outcome of the process will slow them down or put their jobs in jeopardy. This is when we encounter another kind of gridlock. I call it regulatory gridlock. Regulatory gridlock is when subject matter experts (SMEs) on a certain process decide that they don't like whatever is being proposed. Because they are the experts in the process, they invoke a regulation or some other rule that forces the organization to abide by their process.

To understand how irrational and unproductive this is, consider this nonbusiness example. I have a friend whose wife is devoutly religious. Whenever they have an argument or there is contention about something, she will say that God has told her that she is right. As you might imagine, it is difficult to counter the rule of God. It's also difficult to counter an SME's subjective interpretation of a regulation. Sadly, I have seen this tactic work many times, usually because the SME is well regarded in the organization or has overseen a process for many years.

The SME usually believes in what he or she is doing because of what I will call the 1 percent rule. Here is how it works: The SME is a tenured staff member, and as such has seen every permutation of a process. Somewhere along the line, there was a trauma during the process and, as a result, a step was added to the process to resolve this issue. The trauma was real, but in the scheme of things, the chances of it happening again are slim. So now the process has a step in it that covers something that rarely happens or may never happen again.

To be fair to the SME, when the problem does happen, it's not fun. But is it necessary to force everyone through an additional step to avoid something that hasn't happened in 10 years? For the SME, it feels like the issue occurred yesterday. I use the analogy of a wound and a vow. The SMEs and their staff were wounded by the fallout of the trauma and they vowed to never let it happen again. Now you are amid an opportunity to rework this process, and they are blocking the effort. No one wants to challenge the SME because of fear of retribution or, worse yet, a regulatory beat down. To counter this, use analytics to determine the likelihood of the issue happening again.

Regulatory Gridlock in Action

Here's an example of gridlock: An organization that once had an issue with its passwords added a PIN. To log in, you had to have an account number or username, password, and PIN. As you are no doubt aware, the standard for logging in has become username and password, and the organization's customers thought it seemed odd to have an extra step. Where it really became an issue is when the company introduced mobile. It was very expensive to add the PIN to an existing product because it was not standard—the mobile systems were set up to use only username and password.

This particular organization wound up implementing the PIN in the mobile application at a great cost. Many years later, the organization wanted to remove the PIN from the process but it was met with many challenges. This is because of organizational trauma that caused a freak-out when it was revealed that management was considering removing the PIN. Some in the organization remembered the earlier password problem and were worried that they might have to experience the same trauma again—even though nearly every other financial institution had implemented a process that was easier and more secure using only a username and password. Now they had a reverse problem: If they were to unwind the change, the organization's current membership, who had become accustomed to the PIN-and-password process, would have to be retrained. As you might imagine, retraining hundreds of thousands of users who have been logging in a certain way for many years would be difficult. In addition, some will see the change as a step down in security and complain.

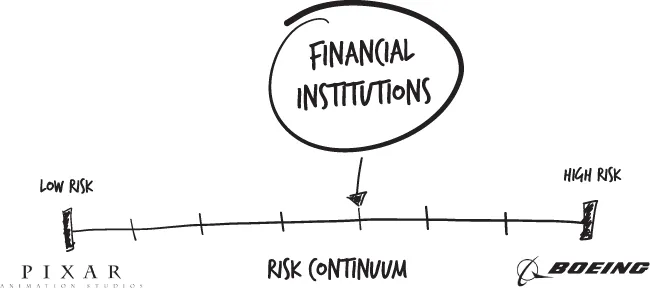

The Risk Spectrum

Inability to reduce or reengineer processes due to organizational muscle memory is a common theme in financial institutions. The main reason is that there is a high price attached to failure, and as a result, processes are often engineered for the 1 percent because in the employee's experience, failure is not an option. In this regard, it is important that the organizational leadership put the right perspective on failure. Failure, when it happens, shouldn't be a taboo subject; it should be talked about and shared. One thing that might help to put failure in perspective is to look at failure by industry.

By evaluating the two extreme ends of the spectrum, one can gain insight into the playing field. At one end is the entertainment company Pixar, where employees are encouraged to fail, and fail fast. The price for failure at Pixar is missing a date on a movie or losing money due to failure. At the other end of the spectrum is an airline company, Boeing. The consequence of failure in this industry could be loss of life (Figure 1.1).

Figure 1.1The risk spectrum

Where does the financial industry fit in this continuum? By using the failure outcome as a litmus test, we can try to put some perspective on where we are on the risk continuum. We can start by saying that no one is going to die from a failure at a financial institution, so we don't belong at the end with Boeing. We can also rule out the other end of the spectrum, as there is the potential for a financial loss and there is a big reputational risk to the organization, particularly with a digital risk that could lead to a security breach. So, on this spectrum we are somewhere in the middle—people won't die, but there is a lot at risk for the organization and for that organization's customers.

The first thing to do is find your place on the risk spectrum and devise a process to evaluate risk for new processes as well as to reevaluate risk in current processes. Here are some things that should be included as part of any process risk review:

How often is this process performed? If the process is rarely performed—such as, for instance, a reverse mortgage, perhaps it is not even worth having the product that the process is attached to. Or conversely, if the process is excessively used by the entire organization, then it needs to be on a list of critical processes that are continuously evaluated for improvement.

How much of the organization is affected by this process? Is the process specific to a department? Processes that are cross-departmental, such as a loan application, need to be evaluated differently than an internal department process like collections.

On the website, you will find a template for evaluating the risk within processes, products, and new features. The risk review should be scored and shared with senior management as well as any process governance groups within the organization. If the process needs to be changed, the risk review should be performed again. For a process, the risk review should cover each of the steps of the process. The process review should provide data definitions and justification for each step of process.

Flawed Bank Processes

It is not necessary to evaluate every process within the average bank to discover the major flaws in our processes. Instead let's take a look at a very common process and point out improvements that can be applied to other similar processes. One simple process with potential complications is an address change. Here is the scenario: A customer calls the call center, goes to the branch in person, emails, or visits the website to change an address. See...

Table of contents

Cover

Title Page

Table of Contents

Foreword

Preface

Acknowledgments

Introduction

PART I: Processes

PART II: Technology

PART III: Security

PART IV: People

PART V: Culture

PART VI: Strategy

Conclusion

About the Companion Website

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Breaking Digital Gridlock by John Best in PDF and/or ePUB format, as well as other popular books in Economics & Banks & Banking. We have over one million books available in our catalogue for you to explore.