Auditing has hit the headlines over recent years, and for all the wrong reasons, and in today's environment, the result of negligent auditing can be serious resulting in sizeable fines and even withdrawal of audit registration which can be costly in terms of fee income.

Frequently Asked Questions in International Standards on Auditing presents the relevant standards in a concise and jargon-free way, enabling auditors to appreciate the reasoning behind the standards and undertake audit work effectively. This book focuses on the main areas of the auditing standards and also addresses some key areas where audit firms are failing and which have been flagged up by audit regulators. The FAQs cover the main parts of each standard, and each question will be answered in a practical context, with worked examples showing how the standards are applied in real situations.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Chapter 1 What is the Role of the International Auditing and Assurance Standards Board?

The International Auditing and Assurance Standards Board (IAASB) is responsible for setting the International Standards on Auditing (ISAs). It is an independent standard-setting body that sets high-quality, international standards on aspects of:

Auditing;

Assurance;

Quality control;

Review; and

Related services.

The IAASB was founded in March 1978 and was previously known as the International Auditing Practices Committee (IAPC) whose work was then focused on three areas, namely:

Objects and scope of audits of financial statements;

Engagement letters; and

General auditing guidelines.

As one can appreciate, the work of the IAASB has significantly evolved and in 1991 the IAPC's guidelines were renamed the International Standards on Auditing.

In 2002, the IAPC changed its name to the IAASB and the International Federation of Accountants (IFAC) approved a series of reforms that were primarily designed (among other things) to strengthen the standard-setting process, which included the processes at the IAASB, in order to best serve the public interest.

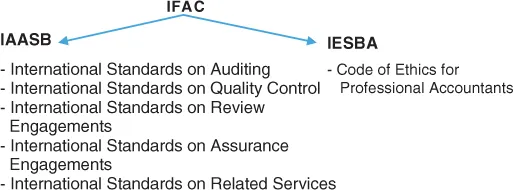

The IAASB is a technical standing committee of IFAC which is also closely linked to the International Ethics Standards Board for Accountants (IESBA) which produces the Code of Ethics for Professional Accountants. An illustration of the hierarchy is as follows:

The standards issued above by the IAASB are authoritative material (as stated in the Preface to International Standards on Quality Control, Auditing, Assurance and Related Services Pronouncements (Revised 2011)). As these standards are authoritative, they must be followed in an audit that is conducted in accordance with the ISAs.

In addition to ‘authoritative’ material published by the IAASB, they also publish ‘non-authoritative’ materials which offer a form of ‘guidance’ rather than mandatory requirements. These are:

International Auditing Practices Notes (IAPNs). These are designed to provide practical assistance to auditors rather than impose mandatory requirements.

Practice Notes Relating to Other International Standards.

Staff Publications: these are designed to raise awareness of new or emerging issues in relation to the standards and to direct attention to the relevant parts of IAASB pronouncements.

Some jurisdictions will have their own standard-setting bodies. For example, the Financial Reporting Council is responsible for standard-setting in the UK. Some countries do adopt ISAs but have to amend them to be country-specific. For example, in the UK, ISAs are adopted but are amended in some areas to be compatible with UK practices and these are then referred to as ISA (UK and Ireland).

Example

ISA 570 Going Concern requires the auditor to consider whether management have made a going concern assessment which covers a period of 12 months from the date of the financial statements. However, in the UK and Ireland, this going concern assessment should cover a period of 12 months from the date of approval (or expected date of approval) of the financial statements.

The UK and Ireland ISA therefore covers a different time span which demonstrates how the standard-setters have amended the mainstream ISA to be specific to the UK and Ireland. In the UK the going concern ISA is known as ISA (UK and Ireland) 570 Going Concern. In the UK and Ireland ISAs are often coined ‘ISA pluses’ because they contain additional or amended requirements to the mainstream ISA issued by the IAASB.

The Clarity Project

In 2004, the IAASB undertook a programme in which the objective was to enhance the clarity of the ISAs. The overall aim of this Clarity Project was to enhance the understandability of the ISAs which would, in turn, enable consistent application of the standards and go to improve overall audit quality on a worldwide level. This was an important exercise following some well-publicised corporate disasters and the decimation of confidence within the auditing profession.

Following the Clarity Project, each standard now has a clear structure with transparent objectives, definitions and requirements, together with application and other explanatory material which drill down further into the requirements of the ISAs. The structure of the new standards makes it easier to understand what is required and what is guidance. In addition, ISQC 1 Q...

Table of contents

Cover

Title Page

Copyright

About the Author

Acknowledgements

Preface

Foreword

Frequently Asked Questions

Introduction

Chapter 1: What is the Role of the International Auditing and Assurance Standards Board?

Chapter 2: Frequently Asked Questions

Chapter 3: Test Your Knowledge

Chapter 4: Answers

Chapter 5: Additional Recommended Reading

Appendix I: Summaries of IFRS and IAS

Appendix II: Illustrative Audit Tests

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Frequently Asked Questions in International Standards on Auditing by Steven Collings in PDF and/or ePUB format, as well as other popular books in Business & Auditing. We have over 1.5 million books available in our catalogue for you to explore.