This book aims at meeting the growing demand in the field by introducing the basic spatial econometrics methodologies to a wide variety of researchers. It provides a practical guide that illustrates the potential of spatial econometric modelling, discusses problems and solutions and interprets empirical results.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es A Primer for Spatial Econometrics un PDF/ePUB en línea?

Sí, puedes acceder a A Primer for Spatial Econometrics de G. Arbia en formato PDF o ePUB, así como a otros libros populares de Volkswirtschaftslehre y Ökonometrie. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

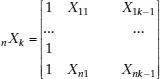

non-stochastic exogenous regressors including a constant term,

a vector of k unknown parameters to be estimated and

a

vector of stochastic disturbances. We will assume throughout the book that the n observations refer to territorial units such as regions or countries.

The classical linear regression model assumes normality, identicity and independence of the stochastic disturbances conditional upon the k regressors. In short

ε | X ≈ i.i.d.N (0, σ2εn In) (1.2)

n In being an n-by-n identity matrix. Equation (1.2) can also be written as:

E(ε | X) = 0(1.3)

E(εεT | X) = σ2εn In (1.4)

Equation (1.3) corresponds to the assumption of exogeneity, Equation (1.4) to the assumption of spherical disturbances (Greene, 2011).

Furthermore it is assumed that the k regressors are not perfectly dependent on one another (full rank of matrix X). Under this set of hypotheses the Ordinary Least Squares fitting criterion (OLS) leads to the best linear unbiased estimators (BLUE) of the vector of parameters β, say

OLS =

. In fact the OLS criterion requires:

S(β) = eT e = min (1.5)

where e = y – X

are the observed errors and eT indicates the transpose of e.

From Equation (1.5) we have:

whence:

OLS = (XT X)-1XT y (1.6)

As said the OLS estimator is unbiased

E(

OLS | X) = β (1.7)

with a variance

Var(

OLS | X) = (XT X)–1σ2ε (1.8)

which achieves the minimum among all possible linear estimators (full efficiency) and tends to zero when n tends to infinity (weak consistency).

From the assumption of normality of the stochastic disturbances, normality of the estimators also follows:

OLS | X ≈ N[β; (XT X)–1σ2ε] (1.9)

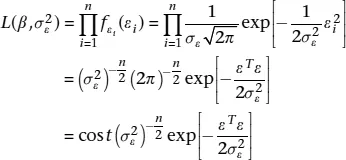

Furthermore, from the assumption of normality of the stochastic disturbances, it also follows that the alternative estimators, based on the Maximum Likelihood criterion (ML), coincide with the OLS solution.

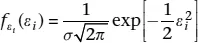

In fact, the single stochastic disturbance is distributed as:

f being a density function, and consequently the likelihood of the observed sample is:

(1.10)

from the assumption of independence of the disturbances. From (1.1) we have that

ε = y – Xβ (1.11)

hence (1.10) can be written as:

(1.12)

and the log-likelihood as:

(1.13)

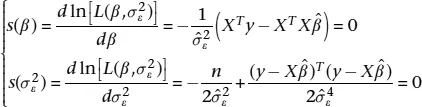

The scores functions are defined as:

(1.14)

and solving the system of k + 1 equations, we have:

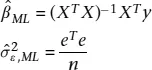

(1.15)

Thus, under the hypothesis of normality of residuals, the ML estimator of β coincides with the OLS estimator. The ML estimator of

on the contrary differs from the unbiased estimator

and it is biased, but asymptotically unbiased.

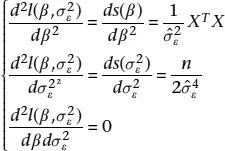

To ensure that the solution obtained is a maximum we consider the second derivatives:

(1.16)

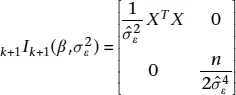

which can be arranged in the Fisher’s Information Matrix:

(1.17)

which is positive definite.

The equivalence between the ML and the OLS estimators ensures that the solution found enjoys all the large sample properties of the ML estimators, that is to say: asymptotic normality, consistency, asymptotic unbiasedness, full efficiency with respect to a larger class of estimators other than the linear...

Índice

Cover

Title

Copyright

Contents

List of Figures

List of Examples

Foreword by William Greene

Preface and Acknowledgements

1 The Classical Linear Regression Model

2 Some Important Spatial Definitions

3 Spatial Linear Regression Models

4 Further Topics in Spatial Econometrics

5 Alternative Model Specifications for Big Datasets

6 Conclusions: What’s Next?

Solutions to the Exercises

Index

Estilos de citas para A Primer for Spatial Econometrics

APA 6 Citation

Arbia, G. (2014). A Primer for Spatial Econometrics ([edition unavailable]). Palgrave Macmillan UK. Retrieved from https://www.perlego.com/book/3486551/a-primer-for-spatial-econometrics-with-applications-in-r-pdf (Original work published 2014)

Chicago Citation

Arbia, G. (2014) 2014. A Primer for Spatial Econometrics. [Edition unavailable]. Palgrave Macmillan UK. https://www.perlego.com/book/3486551/a-primer-for-spatial-econometrics-with-applications-in-r-pdf.

Harvard Citation

Arbia, G. (2014) A Primer for Spatial Econometrics. [edition unavailable]. Palgrave Macmillan UK. Available at: https://www.perlego.com/book/3486551/a-primer-for-spatial-econometrics-with-applications-in-r-pdf (Accessed: 15 October 2022).

MLA 7 Citation

Arbia, G. A Primer for Spatial Econometrics. [edition unavailable]. Palgrave Macmillan UK, 2014. Web. 15 Oct. 2022.