This book aims at meeting the growing demand in the field by introducing the basic spatial econometrics methodologies to a wide variety of researchers. It provides a practical guide that illustrates the potential of spatial econometric modelling, discusses problems and solutions and interprets empirical results.

Foire aux questions

Comment puis-je résilier mon abonnement ?

Il vous suffit de vous rendre dans la section compte dans paramètres et de cliquer sur « Résilier l’abonnement ». C’est aussi simple que cela ! Une fois que vous aurez résilié votre abonnement, il restera actif pour le reste de la période pour laquelle vous avez payé. Découvrez-en plus ici.

Puis-je / comment puis-je télécharger des livres ?

Pour le moment, tous nos livres en format ePub adaptés aux mobiles peuvent être téléchargés via l’application. La plupart de nos PDF sont également disponibles en téléchargement et les autres seront téléchargeables très prochainement. Découvrez-en plus ici.

Quelle est la différence entre les formules tarifaires ?

Les deux abonnements vous donnent un accès complet à la bibliothèque et à toutes les fonctionnalités de Perlego. Les seules différences sont les tarifs ainsi que la période d’abonnement : avec l’abonnement annuel, vous économiserez environ 30 % par rapport à 12 mois d’abonnement mensuel.

Qu’est-ce que Perlego ?

Nous sommes un service d’abonnement à des ouvrages universitaires en ligne, où vous pouvez accéder à toute une bibliothèque pour un prix inférieur à celui d’un seul livre par mois. Avec plus d’un million de livres sur plus de 1 000 sujets, nous avons ce qu’il vous faut ! Découvrez-en plus ici.

Prenez-vous en charge la synthèse vocale ?

Recherchez le symbole Écouter sur votre prochain livre pour voir si vous pouvez l’écouter. L’outil Écouter lit le texte à haute voix pour vous, en surlignant le passage qui est en cours de lecture. Vous pouvez le mettre sur pause, l’accélérer ou le ralentir. Découvrez-en plus ici.

Est-ce que A Primer for Spatial Econometrics est un PDF/ePUB en ligne ?

Oui, vous pouvez accéder à A Primer for Spatial Econometrics par G. Arbia en format PDF et/ou ePUB ainsi qu’à d’autres livres populaires dans Economics et Econometrics. Nous disposons de plus d’un million d’ouvrages à découvrir dans notre catalogue.

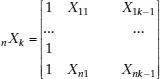

non-stochastic exogenous regressors including a constant term,

a vector of k unknown parameters to be estimated and

a

vector of stochastic disturbances. We will assume throughout the book that the n observations refer to territorial units such as regions or countries.

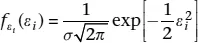

The classical linear regression model assumes normality, identicity and independence of the stochastic disturbances conditional upon the k regressors. In short

ε | X ≈ i.i.d.N (0, σ2εn In) (1.2)

n In being an n-by-n identity matrix. Equation (1.2) can also be written as:

E(ε | X) = 0(1.3)

E(εεT | X) = σ2εn In (1.4)

Equation (1.3) corresponds to the assumption of exogeneity, Equation (1.4) to the assumption of spherical disturbances (Greene, 2011).

Furthermore it is assumed that the k regressors are not perfectly dependent on one another (full rank of matrix X). Under this set of hypotheses the Ordinary Least Squares fitting criterion (OLS) leads to the best linear unbiased estimators (BLUE) of the vector of parameters β, say

OLS =

. In fact the OLS criterion requires:

S(β) = eT e = min (1.5)

where e = y – X

are the observed errors and eT indicates the transpose of e.

From Equation (1.5) we have:

whence:

OLS = (XT X)-1XT y (1.6)

As said the OLS estimator is unbiased

E(

OLS | X) = β (1.7)

with a variance

Var(

OLS | X) = (XT X)–1σ2ε (1.8)

which achieves the minimum among all possible linear estimators (full efficiency) and tends to zero when n tends to infinity (weak consistency).

From the assumption of normality of the stochastic disturbances, normality of the estimators also follows:

OLS | X ≈ N[β; (XT X)–1σ2ε] (1.9)

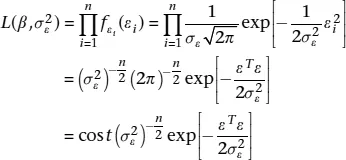

Furthermore, from the assumption of normality of the stochastic disturbances, it also follows that the alternative estimators, based on the Maximum Likelihood criterion (ML), coincide with the OLS solution.

In fact, the single stochastic disturbance is distributed as:

f being a density function, and consequently the likelihood of the observed sample is:

(1.10)

from the assumption of independence of the disturbances. From (1.1) we have that

ε = y – Xβ (1.11)

hence (1.10) can be written as:

(1.12)

and the log-likelihood as:

(1.13)

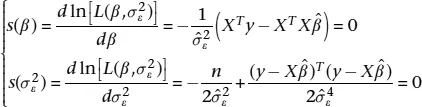

The scores functions are defined as:

(1.14)

and solving the system of k + 1 equations, we have:

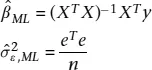

(1.15)

Thus, under the hypothesis of normality of residuals, the ML estimator of β coincides with the OLS estimator. The ML estimator of

on the contrary differs from the unbiased estimator

and it is biased, but asymptotically unbiased.

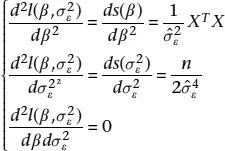

To ensure that the solution obtained is a maximum we consider the second derivatives:

(1.16)

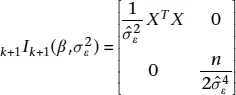

which can be arranged in the Fisher’s Information Matrix:

(1.17)

which is positive definite.

The equivalence between the ML and the OLS estimators ensures that the solution found enjoys all the large sample properties of the ML estimators, that is to say: asymptotic normality, consistency, asymptotic unbiasedness, full efficiency with respect to a larger class of estimators other than the linear...

Table des matières

Cover

Title

Copyright

Contents

List of Figures

List of Examples

Foreword by William Greene

Preface and Acknowledgements

1 The Classical Linear Regression Model

2 Some Important Spatial Definitions

3 Spatial Linear Regression Models

4 Further Topics in Spatial Econometrics

5 Alternative Model Specifications for Big Datasets

6 Conclusions: What’s Next?

Solutions to the Exercises

Index

Normes de citation pour A Primer for Spatial Econometrics

APA 6 Citation

Arbia, G. (2014). A Primer for Spatial Econometrics ([edition unavailable]). Palgrave Macmillan UK. Retrieved from https://www.perlego.com/book/3486551/a-primer-for-spatial-econometrics-with-applications-in-r-pdf (Original work published 2014)

Chicago Citation

Arbia, G. (2014) 2014. A Primer for Spatial Econometrics. [Edition unavailable]. Palgrave Macmillan UK. https://www.perlego.com/book/3486551/a-primer-for-spatial-econometrics-with-applications-in-r-pdf.

Harvard Citation

Arbia, G. (2014) A Primer for Spatial Econometrics. [edition unavailable]. Palgrave Macmillan UK. Available at: https://www.perlego.com/book/3486551/a-primer-for-spatial-econometrics-with-applications-in-r-pdf (Accessed: 15 October 2022).

MLA 7 Citation

Arbia, G. A Primer for Spatial Econometrics. [edition unavailable]. Palgrave Macmillan UK, 2014. Web. 15 Oct. 2022.