Economics

Monetary Policy Strategy

Monetary policy strategy refers to the framework and approach used by central banks to achieve their monetary policy objectives, such as price stability and full employment. It encompasses the tools, rules, and communication methods employed to influence the money supply, interest rates, and overall economic activity. A clear and transparent monetary policy strategy helps guide market expectations and promote economic stability.

Written by Perlego with AI-assistance

Related key terms

1 of 5

10 Key excerpts on "Monetary Policy Strategy"

eBook - ePub

eBook - ePubCentral Banking Systems Compared

The ECB, The Pre-Euro Bundesbank and the Federal Reserve System

- Emmanuel Apel(Author)

- 2003(Publication Date)

- Routledge(Publisher)

3 Monetary Policy Strategy, instruments and actions A central bank is assigned an objective, or objectives, to achieve and maintain. To achieve the objective, or objectives, the central bank’s decisionmaking body usually defines a set of procedures to guide its actions. This set of procedures is called the monetary policy strateg y. The pre-euro Bun-desbankused a Monetary Policy Strategy that is called ‘monetary targeting’. Under such a strategy, the central bank chooses a monetary aggregate and determines its monetary policy actions on the basis of comparisons between the target value of the monetary aggregate and the actual value of the monetary aggregate. The target value of the monetary aggregate must be defined so as to be consistent with the central bank’s definition of the ‘price stability’ objective. Another well-known and widely used (Bank of Canada, Bank of England) Monetary Policy Strategy is the ‘inflation targeting’ strategy. Under such a strategy, the central bank’s decision-making body takes monetary policy actions on the basis of a comparison between the target for inflation and the forecast inflation rate. The monetary authority steers the final target variable (the policy objective of ‘price stability’) directly without the use of a separate intermediate target variable, such as the ‘monetary target’. The inflation targeting strategy requires an inflation forecast since monetary policy actions (i.e. changing short-term interest rates) affect the final objective with a lag. The inflation forecast is usually based on a wide range of economic and financial variables to estimate, for example, the future ‘output gap’, which has an impact on price developments No longer available |Learn more

No longer available |Learn more- (Author)

- 2014(Publication Date)

- College Publishing House(Publisher)

____________________ WORLD TECHNOLOGIES ____________________ Chapter- 4 Monetary Policy Monetary policy is the process by which the monetary authority of a country controls the supply of money, often targeting a rate of interest for the purpose of promoting economic growth and stability. The official goals usually include relatively stable prices and low unemployment. Monetary theory provides insight into how to craft optimal monetary policy. Monetary policy is referred to as either being expansionary or contractionary, where an expansionary policy increases the total supply of money in the economy more rapidly than usual, and contractionary policy expands the money supply more slowly than usual or even shrinks it. Expansionary policy is traditionally used to try to combat unemployment in a recession by lowering interest rates in the hope that easy credit will entice businesses into expanding. Contractionary policy is intended to slow inflation in hopes of avoiding the resulting distortions and deterioration of asset values. Monetary policy differs from fiscal policy, which refers to taxation, government spending, and associated borrowing. Overview Monetary policy rests on the relationship between the rates of interest in an economy, that is, the price at which money can be borrowed, and the total supply of money. Monetary policy uses a variety of tools to control one or both of these, to influence outcomes like economic growth, inflation, exchange rates with other currencies and unemployment. Where currency is under a monopoly of issuance, or where there is a regulated system of issuing currency through banks which are tied to a central bank, the monetary authority has the ability to alter the money supply and thus influence the interest rate (to achieve policy goals). The beginning of monetary policy as such comes from the late 19th century, where it was used to maintain the gold standard. eBook - ePub

eBook - ePub- Sergio Rossi(Author)

- 2007(Publication Date)

- Routledge(Publisher)

5 Monetary policy strategies

Monetary policy strategies around the world are increasingly centred on attaining some targeted rate of inflation, which several academics and policy makers assimilate to price level stability when the measured inflation rate is around but below 2 per cent (owing to a number of measurement biases, as reviewed by Rossi (2001: 31–41)). As a matter of fact, targeting inflation has become a fashion. Since the Reserve Bank of New Zealand first adopted this Monetary Policy Strategy in 1990, an increasing number of monetary authorities around the world – first in advanced economies only, later also in developing and emerging market economies – have been abandoning their monetary or exchange rate targeting strategy to follow this new fashion. As with several fashions nevertheless, targeting an inflation rate rather than an exchange rate or a growth rate of a monetary aggregate has been adopted without any fully thought-out analytical investigation of a phenomenon as complex and controversial as inflation. The same may be argued with respect to previous monetary policy strategies, as they all stem from a symptom-based perception of inflation.It is indeed both undisputed and undisputable today that ‘[e]conomists’ perceptions of inflation rest on measurements of the “general price level” and on rates of change of price indexes’ (Gale 1981: 2). In fact, as surveys of inflation theories show, neither a satisfactory nor an exact analytical definition of inflation exists as yet in the literature (see Bronfenbrenner and Holzman 1963, Laidler and Parkin 1975, Frisch 1983, Parkin 1987, McCallum 1990). This is so much so that, to date, the phenomenon of inflation has been grasped merely by considering its most evident symptom, namely the increase of the relevant consumer price index (or some core inflation index), with no analytical thought whatsoever as to its underlying cause. eBook - PDF

eBook - PDF- H. Tomann(Author)

- 2016(Publication Date)

- Palgrave Macmillan(Publisher)

In the long run, a stable relationship between the quantity of money and the price level can be expected. However, in the short run, supply shocks or monetary shocks can have an inflationary im- pact. A central bank pursuing a monetary targeting strategy would not take action against these shocks but would keep on the long-term path of monetary expansion. A strategy of monetary targeting follows a very simple rule and rejects discrete policy actions. It rests on a strong believe in the sta- bility of a capitalist market system and refers to the experience that monetary policy interventions had rather destabilising effects in the past. It is based on the assumption, however, of a stable money de- mand (see above). If this assumption is violated, for example when a currency is also used as a reserve currency in international finan- cial markets, there may be a large variance in monetary aggregates which does not indicate monetary disequilibria. On the contrary, in monetary equilibrium, money supply should be adjusted to this vari- ance in money demand. So, although the quantity theory of money can be justified in theoretical terms, its rule of monetary targeting has become obsolete. The simple point is that a high variance in monetary aggregates cannot serve as an indicator of what monetary policy is doing. The strategy of the Deutsche Bundesbank which referred to a money target of M3 has been interpreted as a prag- matic strategy since the Bundesbank accepted frequent and large deviations from its M3 target. This was sensible and the Bundes- bank in such cases painstakingly explained why the deviation from the monetary target did not endanger the final target of price level 4. The Monetary Policy Strategy of EMU 59 stability. It is clear, however, that with this practice a monetary tar- get loses its value as indicator of monetary policy which can create credibility. eBook - PDF

eBook - PDF- Subrata Ghatak, José R. Sánchez-Fung(Authors)

- 2017(Publication Date)

- Red Globe Press(Publisher)

C H A P T E R ........................................................................................................................ 8 Monetary policy transmission, rules and strategies 8.1 Introduction ..................................................................................... Chapter 7 described features of monetary institutions in developing countries and how they affect economic performance. How do a central bank’s actions work their way through an economy? This question leads us to consider monetary policy design issues. Accordingly, the text highlights that choosing a monetary policy framework is a chal-lenging task for policy-makers, and for that reason this chapter examines alternative monetary policy frameworks – including monetary targeting and inflation targeting. Finally, the chapter briefly introduces selected fiscal policy developments: fiscal rules and frameworks for gauging fiscal sustainability. This literature is important, because fostering institutions that help to sustain government fiscal policy is crucial for the success of monetary policy, and for overall economic stability. 8.2 The transmission mechanism of monetary policy ..................................................................................... Understanding how monetary policy actions are transmitted to the rest of the economy is an ongoing subject of study for economists. (The Symposia on the Monetary Trans-mission Mechanism in the Journal of Economic Perspectives , 1995, vol 9, no. 4, pp. 3–96, contains an interesting set of papers on this topic. See also, for example, Lewis and Mizen, 2000.) And even though institutional features may well determine the exact transmis-sion mechanism for an individual economy, several hypotheses have been put forward with the aim of explaining this process. Figure 8.1 sketches three widely held views on the transmission mechanism of monetary policy. eBook - PDF

eBook - PDFMaking a Modern Central Bank

The Bank of England 1979–2003

- Harold James(Author)

- 2020(Publication Date)

- Cambridge University Press(Publisher)

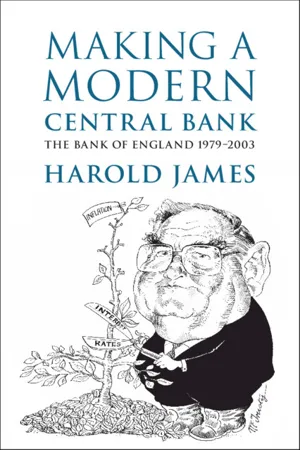

Policy would be directed to a reduction in the growth rate of all the monetary aggregates. The document also investigated what it termed the impact of policy on the ‘Ordinary Man’. This was a critical considera- tion, as ordinary people were thought to be highly sensitive to moves in interest rates, and ordinary people were the voters whose choice was vital every four or five years. The optimistic view was that a fundamental reliance on fiscal policy and interest rates would mean that the ‘proposal Figure 4.1 Sir Geoffrey Howe and Margaret Thatcher in 1984 (on their way to China) (Mirrorpix/Contributor/Getty Images) The Medium-Term Financial Strategy 67 for smoother monetary growth’ would have a lesser impact on general level of interest rates. But within this generally enhanced stability, there might be temporarily greater interest rate fluctuation; and individuals and insti- tutions would have to accommodate to this. 54 Concretely the document set out a series of liberalizations or simplifica- tions: in particular, the ‘corset’ or supplementary special deposits scheme (SSDS) that imposed penalties on banks whose interest-bearing liabilities were growing too quickly would be phased out; 55 the 12½ per cent reserve assets ratio for banks ended; a cash requirement extended to all banks; while the special deposits scheme (where a proportion of bank liabilities had to be placed at the Bank of England at a rate roughly equivalent to Treasury bill rate) was retained. Instead, the growth of money could be limited, above all by controlling public borrowing. The core policy problem lay in the understanding of the drivers of monetary growth. The most important approach in the UK, known as ‘credit counterparts’, was based on an accounting identity derived from the balance sheet of the banking system, and provided a dramatic alternative to the US theory of the money multiplier.

- Thomas F. Cargill(Author)

- 2017(Publication Date)

- Cambridge University Press(Publisher)

Third – control issues: Central banks have less control over the money supply than they did in the past as a result of variation in the money multiplier, which many attribute to the wider range of financial assets available to the public as the result of deregulation and financial liberalization. In contrast, central banks do have significant influence over short-term interest rates. At the same time, this advantage has a caveat. While central banks can influence very short-term interest rates, their influence over medium-and long-term interest rates is much less certain. The longer the term of the interest rate, the more important inflationary expectations. Fourth – relationship to economic activity issues: At various times there has been a close and direct relationship between money and economic activity; however, the relationship between money and economic activity during the past several decades has become unstable for ongoing monetary policy. Central banks have turned to the interest rate channel in the belief it provides a better foundation connecting the tools of monetary policy with the final policy targets. 13.5 The Monetary Policy Instruments 293 Despite arguments in favor of interest rates as the policy instrument, the money supply remains fundamentally important, because, over the longer run, inflation and deflation are inherently related to the growth rate of the money supply. A central bank that puts the money supply on the back burner and focuses only on interest rates is a central bank that will finds its policy to be one of “trouble in River City”. Chapter 14 Step 4: The Central Bank Model of the Economy 14.1 Introduction Step 1 of the sequence of central bank policy focused on the institutional design of the central bank in general and the institutional design of the Federal Reserve in par-ticular. The actual formulation and execution of monetary policy are concentrated in a central committee in most central banks. eBook - PDF

eBook - PDF- Manzur Rashid, Peter Antonioni(Authors)

- 2015(Publication Date)

- For Dummies(Publisher)

That’s not because policy makers don’t care about other macroeconomic variables, just that, in the long run, monetary policy is rather useless at influencing, say, economic growth or unemployment. Anyone who tries to use monetary policy to achieve objectives other than controlling inflation is likely to find themselves in hot water pretty quickly. (You can read more about the dan‑ gers of using monetary policy to reduce unemployment in Chapter 12.) The acceptance that monetary policy should be devoted to achieving price stability means that many central banks have adopted an explicit policy of inflation targeting, including the central banks of New Zealand, Chile, Canada, Israel, the UK, Sweden, Australia, Korea, Norway, the EU and the US. The latter was quite late to the party, only adopting an official inflation target in 2012, although unofficially economists understood that it had been targeting inflation for some time before then. Inflation targeting involves announcing a target level (or range) of inflation that the central bank aims for. It then uses monetary policy to achieve (or attempt to achieve) the target level of inflation. The central bank must pub‑ licly announce the target and not keep it to itself, because doing so puts the bank’s reputation on the line and makes it more likely to hit the target. ( You can read more about an important debate related to this point [the rules versus discretion debate] in Chapter 13.) In theory, inflation targeting should be pretty simple to implement: ▶ ✓ Inflation above target: Raise the interest rate to reduce aggregate demand and reduce inflation. ▶ ✓ Inflation below target: Lower the interest rate to boost aggregate demand and increase inflation. As you can guess, however, in reality things aren’t quite so simple. Accounting for policy time lags Interest rate decisions today take around 18–24 months to have their full effect on the economy. eBook - PDF

eBook - PDFReforms in China's Monetary Policy

A Frontbencher's Perspective

- Sun Guofeng(Author)

- 2016(Publication Date)

- Palgrave Macmillan(Publisher)

Later the wording evolved into a dual mandate of “stabilizing currency and facilitating economic growth.” In December 1993, The Decision of the State Council on Reform of the Financial System stated that the goal of China’s monetary policy reform was to maintain currency value to promote economic growth. And this was a major reform of the dual mandate of China’s monetary policy. In 1995, Article 3 of The Law of the People’s Republic of China on the People’s Bank of China stipulated that the aim of monetary policy is to maintain the stability of currency value and thereby promote economic growth, which provided legal basis for the target of “price stability.” The most sig- nificant change was the clear definition of the intended and possible role of monetary policy in the market economy, that is, to build a sound mon- etary environment. Monetary Policy ● 77 Intermediate Targets The intermediate targets of monetary policy evolved constantly over the years, and there were six milestones. Before the mid-1990s and under the pattern of direct control, the PBC used aggregate credit scale and cash issued as intermediate targets. From 1994 onwards, the PBC gradually narrowed the scope of credit control and introduced foreign exchange open market operations. Meanwhile, the PBC strengthened the statistical analysis of and research on money supply and started to publish the monitoring targets for a different measure of money supply in Q3 1994 and also began to observe changes in the monetary base. In 1995, the PBC attempted to incorporate money supply into the intermediate target system of monetary policy. In 1996, the PBC officially adopted money supply as the intermediate target. After that, the amount of cash issued became a supplementary indicator for money and credit scale instead of the key indicator in the money and credit plan. In 1997, the PBC compiled a trial version of monetary base plan.

- Takatoshi Ito, Andrew K. Rose, Takatoshi Ito, Andrew K. Rose(Authors)

- 2007(Publication Date)

- University of Chicago Press(Publisher)

The second element of the monetary-policy framework is a money-supply rule with two parts: when i t 0, M t is determined by money demand, otherwise the central bank targets the money base according to some rule. In implementing policy, the central bank may hold a very gen-eral portfolio of real and nominal assets, and makes transfers to the treas-ury. Fiscal policy consists of a rule for total government debt at a point in time and a very general rule for the composition of debt. The rest of the model is a standard forward-looking macromodel of the type exhaustively detailed in Woodford (2003). With this setup, Eggertsson-Woodford prove the following irrelevance result: the rational-expectations equilibrium for output, prices, interest rates, and so on, is independent of the specification of 1. the money-base targeting rule; 2. the composition of the central banks balance sheet; 3. the composition of the government’s debt. The key implication is that “unconventional” monetary policy has no e ff ect. In interpreting this result it is crucial to keep in mind that “conven-tional” monetary policy includes the expected future path of the overnight interest rate. In other words, the only thing that matters for monetary pol-icy is the expected future path of the overnight interest rate. Eggertsson-Woodford elaborate on this result, in particular the perhaps surprising implication that the maturity structure of the central bank’s open market operations is unimportant: Even if the e ff ects of open-market operations under the conditions de-scribed in the proposition are not exactly zero, it seems unlikely that they should be large. In our view, it is more important to note that our irrele-vance proposition depends on an assumption that interest-rate policy is specified in a way that implies that these [long bond] open market oper-ations have no consequences for [overnight] interest rate policy, either immediately, or at any subsequent date either.

Index pages curate the most relevant extracts from our library of academic textbooks. They’ve been created using an in-house natural language model (NLM), each adding context and meaning to key research topics.